You might also like

- Tools of Industrial EngineeringDocument2 pagesTools of Industrial EngineeringSiddharth GuptaNo ratings yet

- Hula FileDocument2 pagesHula FileSiddharth GuptaNo ratings yet

- AimDocument1 pageAimSiddharth GuptaNo ratings yet

- D.H.U Levels in MeasurementDocument6 pagesD.H.U Levels in MeasurementSiddharth GuptaNo ratings yet

- Hula FileDocument2 pagesHula FileSiddharth GuptaNo ratings yet

- Hula FileDocument2 pagesHula FileSiddharth GuptaNo ratings yet

- Project Proposal: Title: Limitations & AssumptionsDocument1 pageProject Proposal: Title: Limitations & AssumptionsSiddharth GuptaNo ratings yet

- Notes: January February MarchDocument13 pagesNotes: January February Marchrettty15a3494No ratings yet

- 2013 CalendarDocument13 pages2013 CalendarSiddharth GuptaNo ratings yet

- Monthly Calendar 2011Document12 pagesMonthly Calendar 2011Desy HasrithaNo ratings yet

- What Attracts You To The Arrow Store ?Document7 pagesWhat Attracts You To The Arrow Store ?Siddharth GuptaNo ratings yet

- SDFGDocument7 pagesSDFGSiddharth GuptaNo ratings yet

- Notes: January February MarchDocument14 pagesNotes: January February Marchkyogesh07No ratings yet

- QuestionnaireDocument2 pagesQuestionnaireSiddharth GuptaNo ratings yet

- Cutting PlanDocument1 pageCutting PlanSiddharth GuptaNo ratings yet

- BRCS MRP Exit Strategy - Closure Planning Dec07Document18 pagesBRCS MRP Exit Strategy - Closure Planning Dec07Siddharth GuptaNo ratings yet

- Current Account BalanceDocument2 pagesCurrent Account BalanceSiddharth GuptaNo ratings yet

- Food and AlcoholDocument2 pagesFood and AlcoholSiddharth GuptaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Bep NowDocument25 pagesBep NowDenny KurniawanNo ratings yet

- PDF CropDocument1 pagePDF Cropr v subbaraoNo ratings yet

- 10 Activity 1 MRLFJRDDocument1 page10 Activity 1 MRLFJRDMurielle FajardoNo ratings yet

- 3 02.03.2020 NCLT Court No - IiiDocument5 pages3 02.03.2020 NCLT Court No - IiiVbs ReddyNo ratings yet

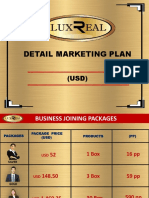

- Luxreal Detail Marketing Plan (2019) UsdDocument32 pagesLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Chaotics KotlerDocument5 pagesChaotics KotlerAlina MarcuNo ratings yet

- Sales and Purchases 2021-22Document15 pagesSales and Purchases 2021-22Vamsi ShettyNo ratings yet

- The Feasibility of Merging Naga, Camaligan and GainzaDocument5 pagesThe Feasibility of Merging Naga, Camaligan and Gainzaapi-3709906100% (1)

- Fanshawe College Application FormDocument2 pagesFanshawe College Application Formdaljit8199No ratings yet

- Future of POL RetailingDocument18 pagesFuture of POL RetailingSuresh MalodiaNo ratings yet

- Hybrid Electric AircraftDocument123 pagesHybrid Electric AircraftSoma Varga100% (1)

- Od 429681727931176100Document5 pagesOd 429681727931176100shubhamsshinde01No ratings yet

- Masura 2Document2,156 pagesMasura 2ClaudiuNo ratings yet

- Rjis 16 04Document14 pagesRjis 16 04geo12345abNo ratings yet

- List of Maharashtra Pharrma CompaniesDocument6 pagesList of Maharashtra Pharrma CompaniesrajnayakpawarNo ratings yet

- IBM - Multiple Choice Questions PDFDocument15 pagesIBM - Multiple Choice Questions PDFsachsanjuNo ratings yet

- Economics of The Printing PressDocument39 pagesEconomics of The Printing PressNancy Xie100% (1)

- Monopolistic CompetitionDocument14 pagesMonopolistic CompetitionRajesh GangulyNo ratings yet

- Lesson 1 Business EthicsDocument21 pagesLesson 1 Business EthicsRiel Marc AliñaboNo ratings yet

- An Introduction To Private Sector Financing of Transportation InfrastructureDocument459 pagesAn Introduction To Private Sector Financing of Transportation InfrastructureBob DiamondNo ratings yet

- Master Coin CodesDocument19 pagesMaster Coin CodesPavlo PietrovichNo ratings yet

- Second Reading of Ordinance State Housing Law 01-05-16Document16 pagesSecond Reading of Ordinance State Housing Law 01-05-16L. A. PatersonNo ratings yet

- LANDON LTDDocument2 pagesLANDON LTDStephanie ChristianNo ratings yet

- 12 Risks With Infinite Impact PDFDocument212 pages12 Risks With Infinite Impact PDFkevin muchungaNo ratings yet

- 2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Document1 page2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Lyka Lim Pascua100% (1)

- Reflections Fall 2010Document84 pagesReflections Fall 2010campbell_harmon6178No ratings yet

- Internal Analysis of Nissan Motors Co - PPDocument1 pageInternal Analysis of Nissan Motors Co - PPvignesh GtrNo ratings yet

- STP DoneDocument3 pagesSTP DoneD Attitude KidNo ratings yet

- IRCTCs e-Ticketing Service DetailsDocument2 pagesIRCTCs e-Ticketing Service DetailsOPrakash RNo ratings yet

- Option To PurchaseDocument3 pagesOption To PurchaseAlberta Real EstateNo ratings yet