You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Blades in The Dark - Doskvol Maps PDFDocument3 pagesBlades in The Dark - Doskvol Maps PDFRobert Rome20% (5)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Rich Dad Poor DadDocument26 pagesRich Dad Poor Dadchaand33100% (17)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- April PayslipDocument1 pageApril PayslipDev CharanNo ratings yet

- 2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Document1 page2012 - Communities Cagayan Incorporated Vs Nanol, GR 176791, November 14, 2012Lyka Lim Pascua100% (1)

- Fourmula ONE For HealthDocument2 pagesFourmula ONE For HealthGemma LuaNo ratings yet

- Daimler Chrysler MergerDocument23 pagesDaimler Chrysler MergerAdnan Ad100% (1)

- The Optimum Quantity of Money Milton FriedmanDocument305 pagesThe Optimum Quantity of Money Milton Friedmantrafalgar111100% (4)

- The Feasibility of Merging Naga, Camaligan and GainzaDocument5 pagesThe Feasibility of Merging Naga, Camaligan and Gainzaapi-3709906100% (1)

- EVENT Marketing Generates New BusinessDocument26 pagesEVENT Marketing Generates New Businesssuruchi100% (1)

- Case QDocument1 pageCase QMayuresh SanapNo ratings yet

- Converting Waste Into Organic Manure - FinalDocument21 pagesConverting Waste Into Organic Manure - FinalMayuresh SanapNo ratings yet

- Case QDocument1 pageCase QMayuresh SanapNo ratings yet

- Infosys AR 2010Document96 pagesInfosys AR 2010sh_chandraNo ratings yet

- Credit Cards 101Document26 pagesCredit Cards 101Mayuresh SanapNo ratings yet

- Babcock & WilcoxDocument3 pagesBabcock & WilcoxMayuresh SanapNo ratings yet

- CP 14 Operations MGMTDocument6 pagesCP 14 Operations MGMTSrijith M MenonNo ratings yet

- ScribdDocument1 pageScribdMayuresh SanapNo ratings yet

- SCMDocument1 pageSCMMayuresh SanapNo ratings yet

- ScribdDocument1 pageScribdMayuresh SanapNo ratings yet

- SCMDocument1 pageSCMMayuresh SanapNo ratings yet

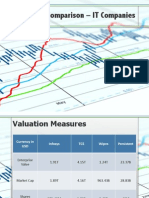

- Indian IT Companies - Financial ComparisonDocument5 pagesIndian IT Companies - Financial ComparisonMayuresh SanapNo ratings yet

- SCMDocument1 pageSCMMayuresh SanapNo ratings yet

- ScribdDocument1 pageScribdMayuresh SanapNo ratings yet

- SCMDocument1 pageSCMMayuresh SanapNo ratings yet

- Technical Interview Summaries of Engineering StudentsDocument25 pagesTechnical Interview Summaries of Engineering StudentsSatendra TiwariNo ratings yet

- A Few Great Indian PersonalitiesDocument65 pagesA Few Great Indian Personalitiesjaggu.goka95% (21)

- Higher Algebra - Hall & KnightDocument593 pagesHigher Algebra - Hall & KnightRam Gollamudi100% (2)

- Seminar TopicsDocument15 pagesSeminar TopicsMayuresh Sanap100% (1)

- ModakDocument9 pagesModakMayuresh SanapNo ratings yet

- CN Question BankDocument1 pageCN Question BankMayuresh SanapNo ratings yet

- PRC Ready ReckonerDocument2 pagesPRC Ready Reckonersparthan300No ratings yet

- Fanshawe College Application FormDocument2 pagesFanshawe College Application Formdaljit8199No ratings yet

- The Value of Money The Value of Labor Power and The Marxian Transformation Problem Foley 1982Document12 pagesThe Value of Money The Value of Labor Power and The Marxian Transformation Problem Foley 1982Espinete1984No ratings yet

- 19th Century Changes: Economic Changes Cultural Changes Political Changes Social ChangesDocument1 page19th Century Changes: Economic Changes Cultural Changes Political Changes Social ChangesShina P ReyesNo ratings yet

- 7 Marketing Strategies of India Automobile CompaniesDocument7 pages7 Marketing Strategies of India Automobile CompaniesamritNo ratings yet

- Schram y Pavlovskaya ED 2017 Rethinking Neoliberalism. Resisiting The Disciplinary Regime LIBRODocument285 pagesSchram y Pavlovskaya ED 2017 Rethinking Neoliberalism. Resisiting The Disciplinary Regime LIBROJessica ArgüelloNo ratings yet

- c6. Test 1. Listening. AnswerDocument5 pagesc6. Test 1. Listening. AnswerLê VinhNo ratings yet

- Solutions: ECO 100Y Introduction To Economics Midterm Test # 2Document15 pagesSolutions: ECO 100Y Introduction To Economics Midterm Test # 2examkillerNo ratings yet

- Ex 6 Duo - 2021 Open-Macroeconomics Basic Concepts: Part 1: Multple ChoicesDocument6 pagesEx 6 Duo - 2021 Open-Macroeconomics Basic Concepts: Part 1: Multple ChoicesTuyền Lý Thị LamNo ratings yet

- Parag Milk & Namaste India Milk Dairy by Manish Kumar Rajpoot (MBA)Document17 pagesParag Milk & Namaste India Milk Dairy by Manish Kumar Rajpoot (MBA)Manish Kumar Rajpoot100% (1)

- The World Trade Organiation and World Trade Patterns: Chapter - 40Document8 pagesThe World Trade Organiation and World Trade Patterns: Chapter - 40Halal BoiNo ratings yet

- US Internal Revenue Service: p1438Document518 pagesUS Internal Revenue Service: p1438IRSNo ratings yet

- Tutorial Letter 201/2/2018: Business Management 1ADocument18 pagesTutorial Letter 201/2/2018: Business Management 1ABen BenNo ratings yet

- FormatDocument2 pagesFormatbasavarajj123No ratings yet

- 20 Recent IELTS Graph Samples With AnswersDocument14 pages20 Recent IELTS Graph Samples With AnswersRizwan BashirNo ratings yet

- 12 Jun 2019 PDFDocument12 pages12 Jun 2019 PDFAnonymous dy7g4jzo7No ratings yet

- Radical Culture Research Collective - Nicolas BourriaudDocument3 pagesRadical Culture Research Collective - Nicolas BourriaudGwyddion FlintNo ratings yet

- Option To PurchaseDocument3 pagesOption To PurchaseAlberta Real EstateNo ratings yet

- TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument7 pagesTXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceEllis DavisNo ratings yet

- Micro-Economic Analysis of Nestle Ma Assignment: Group 2IDocument7 pagesMicro-Economic Analysis of Nestle Ma Assignment: Group 2IShreya GhoshNo ratings yet

- Ud. Wirastri Jurnal Penerimaan Kas Desember 2015Document40 pagesUd. Wirastri Jurnal Penerimaan Kas Desember 2015Raihan FatihaNo ratings yet