You might also like

- 35 Ipcc Accounting Practice ManualDocument218 pages35 Ipcc Accounting Practice ManualDeepal Dhameja100% (6)

- 11 Accountancy Notes Ch08 Financial Statements of Sole Proprietorship 02Document9 pages11 Accountancy Notes Ch08 Financial Statements of Sole Proprietorship 02Anonymous NSNpGa3T93100% (1)

- Armed Struggle in Africa (1969)Document167 pagesArmed Struggle in Africa (1969)Dr.VolandNo ratings yet

- Accounting Decisions Workbook Covers Financials, Costing, AnalysisDocument96 pagesAccounting Decisions Workbook Covers Financials, Costing, AnalysisSatyabrataNayak100% (1)

- Managing Performance with Balanced ScorecardDocument25 pagesManaging Performance with Balanced ScorecardPooja RanaNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Technician Pilot Papers PDFDocument133 pagesTechnician Pilot Papers PDFCasius Mubamba100% (4)

- Contemporary Theories of MotivationDocument17 pagesContemporary Theories of MotivationArsalan SattiNo ratings yet

- Evoked PotentialsDocument49 pagesEvoked PotentialsparuNo ratings yet

- ABE Dip 1 - Financial Accounting JUNE 2005Document19 pagesABE Dip 1 - Financial Accounting JUNE 2005spinster40% (1)

- Talent ManagementDocument33 pagesTalent ManagementPooja Rana100% (3)

- The Future of The Indian Print Media Ind PDFDocument22 pagesThe Future of The Indian Print Media Ind PDFAdarsh KambojNo ratings yet

- Capital Structure TheoriesDocument31 pagesCapital Structure TheoriesShashank100% (1)

- Capital Structure TheoriesDocument31 pagesCapital Structure TheoriesShashank100% (1)

- Xu10j4 PDFDocument80 pagesXu10j4 PDFPaulo Luiz França100% (1)

- MB0041Document3 pagesMB0041Smu DocNo ratings yet

- MB0041 - Summer 2014Document3 pagesMB0041 - Summer 2014Rajesh SinghNo ratings yet

- Get Answers of Following Questions Here: MB0041 - Financial and Management AccountingDocument3 pagesGet Answers of Following Questions Here: MB0041 - Financial and Management AccountingRajesh SinghNo ratings yet

- MBA Semester 1 Spring 2015 Solved Assignments - MB0041Document3 pagesMBA Semester 1 Spring 2015 Solved Assignments - MB0041SolvedSmuAssignmentsNo ratings yet

- MB0041 Financial and Management AccountingDocument12 pagesMB0041 Financial and Management AccountingDivyang Panchasara0% (2)

- SITXFIN003 - Student Assessment v3.1Document11 pagesSITXFIN003 - Student Assessment v3.1Esteban BuitragoNo ratings yet

- MBA Financial Accounting Exercises SolutionsDocument17 pagesMBA Financial Accounting Exercises SolutionsRasanjaliGunasekeraNo ratings yet

- Assignment Front Sheet: BusinessDocument13 pagesAssignment Front Sheet: BusinessHassan AsgharNo ratings yet

- CCE E MBA (Aviation Management) Assignment 1Document6 pagesCCE E MBA (Aviation Management) Assignment 1Sukhi MakkarNo ratings yet

- ISQ EXAMINATION ACCOUNTING FOR FINANCIAL SERVICESDocument6 pagesISQ EXAMINATION ACCOUNTING FOR FINANCIAL SERVICEStysonhishamNo ratings yet

- Multiple Choice Questions: Section-IDocument6 pagesMultiple Choice Questions: Section-Isah108_pk796No ratings yet

- ACT 501 - AssignmentDocument6 pagesACT 501 - AssignmentShariful Islam ShaheenNo ratings yet

- CA IPCC Nov 2010 Accounts Solved AnswersDocument13 pagesCA IPCC Nov 2010 Accounts Solved AnswersprateekfreezerNo ratings yet

- CS Exec - Prog - Paper-2 Company AC Cost & Management AccountingDocument25 pagesCS Exec - Prog - Paper-2 Company AC Cost & Management AccountingGautam SinghNo ratings yet

- Solved SMU AssignmentDocument4 pagesSolved SMU AssignmentArvind KNo ratings yet

- VEC Dept of Mgt Studies BA7106 QBDocument12 pagesVEC Dept of Mgt Studies BA7106 QBSRMBALAANo ratings yet

- BMAC5203 Assignment Jan 2015 (Amended)Document6 pagesBMAC5203 Assignment Jan 2015 (Amended)Robert WilliamsNo ratings yet

- Ac1025 Excza 11Document18 pagesAc1025 Excza 11gurpreet_mNo ratings yet

- Universiti Teknologi Mara Final Examination: Confidential AC/APR 2007/FAR100/FAR110/ FAC100Document11 pagesUniversiti Teknologi Mara Final Examination: Confidential AC/APR 2007/FAR100/FAR110/ FAC100kaitokid77No ratings yet

- Finance Accounting 3 May 2012Document15 pagesFinance Accounting 3 May 2012Prasad C MNo ratings yet

- Goals, Functions of Finance Manager, Working Capital RequirementsDocument3 pagesGoals, Functions of Finance Manager, Working Capital RequirementsISLAMICLECTURESNo ratings yet

- Management Control SystemDocument11 pagesManagement Control SystemomkarsawantNo ratings yet

- BBA203 Financial AccountingDocument3 pagesBBA203 Financial AccountingRajdeep KumarNo ratings yet

- Cash flow statement problemsDocument12 pagesCash flow statement problemsAnjali Mehta100% (1)

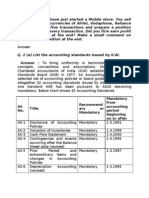

- Recommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterDocument7 pagesRecommend Ary or Mandatory Mandatory From Accounting Period Beginning On or AfterdnbiswasNo ratings yet

- Manage Finances Within The BudgetDocument12 pagesManage Finances Within The BudgetEsteban BuitragoNo ratings yet

- Gujarat Technological University: InstructionsDocument4 pagesGujarat Technological University: InstructionsMuvin KoshtiNo ratings yet

- IMT 57 Financial Accounting M1Document4 pagesIMT 57 Financial Accounting M1solvedcareNo ratings yet

- M Com Part I Accounts Question PDFDocument15 pagesM Com Part I Accounts Question PDFpink_key711No ratings yet

- Accounting For Managers MB003 QuestionDocument34 pagesAccounting For Managers MB003 QuestionAiDLo0% (1)

- Single EntryDocument0 pagesSingle EntrylathadevaraajNo ratings yet

- 29234rtp May13 Ipcc Atc 1Document50 pages29234rtp May13 Ipcc Atc 1rahulkingdonNo ratings yet

- Accounting For Managers GTU Question PaperDocument3 pagesAccounting For Managers GTU Question PaperbhfunNo ratings yet

- Final AccountsDocument5 pagesFinal AccountsGopal KrishnanNo ratings yet

- Review and Evaluate Financial Management Processes: Submission DetailsDocument9 pagesReview and Evaluate Financial Management Processes: Submission Detailsrida zulquarnainNo ratings yet

- Practice MT2 SolutionDocument15 pagesPractice MT2 SolutionKionna TamaraNo ratings yet

- Accountancy EngDocument8 pagesAccountancy EngBettappa Patil100% (1)

- Finance Past PaperDocument6 pagesFinance Past PaperNikki ZhuNo ratings yet

- Unsolved Paper Part IDocument107 pagesUnsolved Paper Part IAdnan KazmiNo ratings yet

- MB41Document5 pagesMB41Prajeesh Kumar KmNo ratings yet

- Examination Paper-2010Document5 pagesExamination Paper-2010api-248768984No ratings yet

- AC100 Exam 2012Document17 pagesAC100 Exam 2012Ruby TangNo ratings yet

- Loyola College (Autonomous), Chennai - 600 034 Loyola College (Autonomous), Chennai - 600 034 Loyola College (Autonomous), Chennai - 600 034Document3 pagesLoyola College (Autonomous), Chennai - 600 034 Loyola College (Autonomous), Chennai - 600 034 Loyola College (Autonomous), Chennai - 600 034Mohan MuthusamyNo ratings yet

- Accountancy and Business Statistics Second Paper: Management AccountingDocument10 pagesAccountancy and Business Statistics Second Paper: Management AccountingGuruKPONo ratings yet

- 05mba14 July 07Document4 pages05mba14 July 07nitte5768No ratings yet

- QBDocument34 pagesQBAadeel NooraniNo ratings yet

- IBF FINAL Exam SP 2020 ONLINE BDocument4 pagesIBF FINAL Exam SP 2020 ONLINE BSYED MANSOOR ALI SHAHNo ratings yet

- Funds Flow AnalysisDocument20 pagesFunds Flow AnalysisRajeevAgrawalNo ratings yet

- Financial Management - I (Practical Problems)Document9 pagesFinancial Management - I (Practical Problems)sameer_kini100% (1)

- Fundamentals of Accounting Problems and SolutionsDocument7 pagesFundamentals of Accounting Problems and SolutionsashwinNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument38 pages© The Institute of Chartered Accountants of IndiaSarah HolmesNo ratings yet

- Commercial Banking Revenues World Summary: Market Values & Financials by CountryFrom EverandCommercial Banking Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Presentation On Capital GainsDocument12 pagesPresentation On Capital GainsSheemaShaheenNo ratings yet

- Project Risk MGMTDocument22 pagesProject Risk MGMTPooja RanaNo ratings yet

- Techniques of BudgetingDocument88 pagesTechniques of BudgetingPooja RanaNo ratings yet

- Chapter 5 - Cost of Capital SML 401 BtechDocument52 pagesChapter 5 - Cost of Capital SML 401 BtechfikeNo ratings yet

- Income From House Property KarthikDocument45 pagesIncome From House Property KarthikPooja RanaNo ratings yet

- ITSM software implementation improves YUBC Internet serviceDocument32 pagesITSM software implementation improves YUBC Internet servicePooja RanaNo ratings yet

- ITSM software implementation improves YUBC Internet serviceDocument32 pagesITSM software implementation improves YUBC Internet servicePooja RanaNo ratings yet

- Event MGTDocument20 pagesEvent MGTPooja RanaNo ratings yet

- Project Risk MGMTDocument22 pagesProject Risk MGMTPooja RanaNo ratings yet

- Bo RDocument15 pagesBo RPooja RanaNo ratings yet

- Political Environment of Business: Presented by Aun AhmedDocument18 pagesPolitical Environment of Business: Presented by Aun AhmedMdheer09No ratings yet

- BR 3Document39 pagesBR 3Akhil VashishthaNo ratings yet

- ITSM software implementation improves YUBC Internet serviceDocument32 pagesITSM software implementation improves YUBC Internet servicePooja RanaNo ratings yet

- Imt CDLDocument56 pagesImt CDLPooja Rana50% (4)

- Global SCM OverviewDocument8 pagesGlobal SCM OverviewPooja RanaNo ratings yet

- Imt LawDocument42 pagesImt LawPooja RanaNo ratings yet

- Application For The Post of - at Media Lab Asia, Delhi Position CodeDocument3 pagesApplication For The Post of - at Media Lab Asia, Delhi Position CodePooja RanaNo ratings yet

- Oltp VS OlapDocument9 pagesOltp VS OlapSikkandar Sha100% (1)

- LawDocument19 pagesLawPooja RanaNo ratings yet

- StatsDocument5 pagesStatsPooja RanaNo ratings yet

- HRM Cross-Border M&A GuideDocument14 pagesHRM Cross-Border M&A GuidePooja RanaNo ratings yet

- Groupware Technology (Sameer)Document15 pagesGroupware Technology (Sameer)DIPAK VINAYAK SHIRBHATENo ratings yet

- ReserchDocument14 pagesReserchPooja RanaNo ratings yet

- Architecture of DSS, GDSS & ESSDocument28 pagesArchitecture of DSS, GDSS & ESSPooja Rana50% (2)

- Akriti Shrivastava CMBA2Y3-1906Document6 pagesAkriti Shrivastava CMBA2Y3-1906Siddharth ChoudheryNo ratings yet

- Guidelines Regarding The Handling of Cable Drums During Transport and StorageDocument5 pagesGuidelines Regarding The Handling of Cable Drums During Transport and StorageJegan SureshNo ratings yet

- Washington State Employee - 4/2010Document8 pagesWashington State Employee - 4/2010WFSEc28No ratings yet

- My Sweet Beer - 23 MaiDocument14 pagesMy Sweet Beer - 23 Maihaytem chakiriNo ratings yet

- Kitchen in The Food Service IndustryDocument37 pagesKitchen in The Food Service IndustryTresha Mae Dimdam ValenzuelaNo ratings yet

- Creating Rapid Prototype Metal CastingsDocument10 pagesCreating Rapid Prototype Metal CastingsShri JalihalNo ratings yet

- 1 s2.0 S0313592622001369 MainDocument14 pages1 s2.0 S0313592622001369 MainNGOC VO LE THANHNo ratings yet

- Pg-586-591 - Annexure 13.1 - AllEmployeesDocument7 pagesPg-586-591 - Annexure 13.1 - AllEmployeesaxomprintNo ratings yet

- Rohini 43569840920Document4 pagesRohini 43569840920SowmyaNo ratings yet

- Section - I: Cover Page Section - II:: IndexDocument21 pagesSection - I: Cover Page Section - II:: Indexamit rajputNo ratings yet

- PC-II Taftan Master PlanDocument15 pagesPC-II Taftan Master PlanMunir HussainNo ratings yet

- B JA RON GAWATDocument17 pagesB JA RON GAWATRon GawatNo ratings yet

- Grate Inlet Skimmer Box ™ (GISB™ ) Suntree Technologies Service ManualDocument4 pagesGrate Inlet Skimmer Box ™ (GISB™ ) Suntree Technologies Service ManualOmar Rodriguez OrtizNo ratings yet

- Wireshark Lab: 802.11: Approach, 6 Ed., J.F. Kurose and K.W. RossDocument5 pagesWireshark Lab: 802.11: Approach, 6 Ed., J.F. Kurose and K.W. RossN Azzati LabibahNo ratings yet

- Management principles and quantitative techniquesDocument7 pagesManagement principles and quantitative techniquesLakshmi Devi LakshmiNo ratings yet

- Brochures Volvo Engines d11 CanadaDocument4 pagesBrochures Volvo Engines d11 CanadaDIONYBLINK100% (2)

- Dhilshahilan Rajaratnam: Work ExperienceDocument5 pagesDhilshahilan Rajaratnam: Work ExperienceShazard ShortyNo ratings yet

- Tdi Hazid TemplateDocument11 pagesTdi Hazid TemplateAnonymous rwojPlYNo ratings yet

- Tds Uniqflow 372s enDocument1 pageTds Uniqflow 372s enm daneshpourNo ratings yet

- Sonydsp v77 SM 479622 PDFDocument41 pagesSonydsp v77 SM 479622 PDFmorvetrNo ratings yet

- Url Profile Results 200128191050Document25 pagesUrl Profile Results 200128191050Wafiboi O. EtanoNo ratings yet

- Shrey's PHP - PracticalDocument46 pagesShrey's PHP - PracticalNahi PataNo ratings yet

- The Mpeg Dash StandardDocument6 pagesThe Mpeg Dash Standard9716755397No ratings yet

- 9643 SoirDocument38 pages9643 SoirpolscreamNo ratings yet

- Dhabli - 1axis Tracker PVSYSTDocument5 pagesDhabli - 1axis Tracker PVSYSTLakshmi NarayananNo ratings yet