You might also like

- ProbabilityDocument22 pagesProbabilityvir1672No ratings yet

- Activity-Based Costing and Activity-Based Management: Tracing, Indirect-Cost Pools, and Cost-Allocation BasesDocument9 pagesActivity-Based Costing and Activity-Based Management: Tracing, Indirect-Cost Pools, and Cost-Allocation Basesvir1672No ratings yet

- Solutions To EPS Examples 1-7 For PostingDocument12 pagesSolutions To EPS Examples 1-7 For Postingvir1672No ratings yet

- Queuing Theory: Dr. T. T. KachwalaDocument9 pagesQueuing Theory: Dr. T. T. Kachwalavir1672No ratings yet

- Wipro Annual Report 2010-11 FinalDocument210 pagesWipro Annual Report 2010-11 FinalyagneshroyalNo ratings yet

- Structuring The Project Finance: Submitted byDocument22 pagesStructuring The Project Finance: Submitted byvir1672No ratings yet

- Chap 014Document24 pagesChap 014vir1672No ratings yet

- Management'S Discussion and Analysis (Md&A)Document8 pagesManagement'S Discussion and Analysis (Md&A)vir1672No ratings yet

- Camelback CommunicationsDocument9 pagesCamelback Communicationsvir1672100% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Bank of BarodaDocument111 pagesBank of BarodaRahul Kr JhaNo ratings yet

- Forex Hunter Part 1Document66 pagesForex Hunter Part 1KARAN DODIYANo ratings yet

- Criteria For Choosing Brand ElementsDocument11 pagesCriteria For Choosing Brand ElementsRakibZWaniNo ratings yet

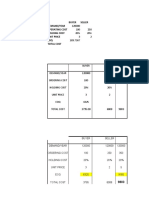

- Buyer Seller Demand/Year Operating Cost Holding Cost Unit Price EOQ Total CostDocument7 pagesBuyer Seller Demand/Year Operating Cost Holding Cost Unit Price EOQ Total CostNeha SmritiNo ratings yet

- Quiz 9 Econ1011 - KEYDocument4 pagesQuiz 9 Econ1011 - KEYMatthewLiuNo ratings yet

- Questionnaire For Understanding Investor BehaviourDocument6 pagesQuestionnaire For Understanding Investor BehaviourNitish Kumar TiwaryNo ratings yet

- Masterlist of Position Category Updated 10.25.2021Document20 pagesMasterlist of Position Category Updated 10.25.2021johnmarcNo ratings yet

- BBM 124 Principles of Marketing Course OutlineDocument3 pagesBBM 124 Principles of Marketing Course OutlineSserwadda Abdul RahmanNo ratings yet

- Five Forces Analysis of NestleDocument3 pagesFive Forces Analysis of NestleAfrinNo ratings yet

- Chapter 8Document35 pagesChapter 8Shahtaj JuttNo ratings yet

- A Comparative Study On Organised Security Market (Document12 pagesA Comparative Study On Organised Security Market (DeepakNo ratings yet

- Case 4 - Alternative Distribution StrategiesDocument8 pagesCase 4 - Alternative Distribution Strategiesmohamed mohamedgalalNo ratings yet

- Three Point SystemDocument2 pagesThree Point SystemtrionjetNo ratings yet

- Chaffey. D., Ellis-Chadwick, F., Johnson, K., & Mayer, R. (2006) - Internet Ed.) Harlow, UK: Prentice Hall FTDocument3 pagesChaffey. D., Ellis-Chadwick, F., Johnson, K., & Mayer, R. (2006) - Internet Ed.) Harlow, UK: Prentice Hall FTOLIVIANo ratings yet

- ECO101 Week10 Monopoly&MarketPowerDocument30 pagesECO101 Week10 Monopoly&MarketPowerShawn MaNo ratings yet

- Mini EssayDocument4 pagesMini Essaynaveeed dcNo ratings yet

- Erp SimDocument17 pagesErp SimGautam D100% (1)

- Problems Stocks ValuationDocument3 pagesProblems Stocks Valuationmimi96No ratings yet

- Chapter 6 Review Questions & AnswersDocument17 pagesChapter 6 Review Questions & Answersalaamabood6No ratings yet

- Chapter 9 PracticeDocument4 pagesChapter 9 Practicexabir54952No ratings yet

- Micro Chap 7Document3 pagesMicro Chap 7Kote GagnidzeNo ratings yet

- M Javed AslamDocument35 pagesM Javed AslammukhtarNo ratings yet

- MGEB02-2019 SyllabusDocument6 pagesMGEB02-2019 SyllabusMick Mendoza100% (1)

- Allen and Gale. 1994. Financial Innovation and Risk SharingDocument411 pagesAllen and Gale. 1994. Financial Innovation and Risk SharingCitio Logos100% (1)

- The Oxford Handbook of China Innovation Oxford Handbooks Series Xiaolan Fu Full ChapterDocument67 pagesThe Oxford Handbook of China Innovation Oxford Handbooks Series Xiaolan Fu Full Chaptercrystal.jackson685100% (9)

- Market Mechanism in Economics: Examples and GraphsDocument11 pagesMarket Mechanism in Economics: Examples and Graphskripasini balajiNo ratings yet

- Retail Mix: Social, Economic, Technological, and Competitive ForcesDocument12 pagesRetail Mix: Social, Economic, Technological, and Competitive ForcesAmit SinghNo ratings yet

- Fast Fasion Brand-Uniqlo: H&M vs. ZaraDocument4 pagesFast Fasion Brand-Uniqlo: H&M vs. ZaraHappyninjaytNo ratings yet

- Chapter 2: Application of Demand and SupplyDocument9 pagesChapter 2: Application of Demand and SupplyAjilNo ratings yet

- Economics Higher Level Paper 3: Instructions To CandidatesDocument6 pagesEconomics Higher Level Paper 3: Instructions To CandidatesAndres Krauss100% (1)