You might also like

- Financial Planning Business PlanDocument32 pagesFinancial Planning Business PlanGetto PangandoyonNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Bridge With Buffett A Mathematician On Wall StreetDocument3 pagesBridge With Buffett A Mathematician On Wall StreetgjangNo ratings yet

- Graham and Doddsville - Issue 9 - Spring 2010Document33 pagesGraham and Doddsville - Issue 9 - Spring 2010g4nz0No ratings yet

- Competitive Advantage PeriodDocument6 pagesCompetitive Advantage PeriodAndrija BabićNo ratings yet

- The 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy HimDocument5 pagesThe 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy Himrakeshmoney99No ratings yet

- Decision-Making For Investors: Theory, Practice, and PitfallsDocument20 pagesDecision-Making For Investors: Theory, Practice, and PitfallsGaurav JainNo ratings yet

- 8th Annual New York: Value Investing CongressDocument53 pages8th Annual New York: Value Investing CongressVALUEWALK LLCNo ratings yet

- Moi201102 Super Investors PRINTDocument170 pagesMoi201102 Super Investors PRINTbrl_oakcliffNo ratings yet

- Schloss-10 11 06Document3 pagesSchloss-10 11 06Logic Gate CapitalNo ratings yet

- Scott Miller of Greenhaven Road Capital: Long On Zix CorpDocument0 pagesScott Miller of Greenhaven Road Capital: Long On Zix CorpcurrygoatNo ratings yet

- OakTree Real EstateDocument13 pagesOakTree Real EstateCanadianValue100% (1)

- Summary of Heather Brilliant & Elizabeth Collins's Why Moats MatterFrom EverandSummary of Heather Brilliant & Elizabeth Collins's Why Moats MatterNo ratings yet

- Buffett On ValuationDocument7 pagesBuffett On ValuationAyush AggarwalNo ratings yet

- Income Taxation Notes On BanggawanDocument5 pagesIncome Taxation Notes On BanggawanHopey100% (4)

- EVA Vyaderm Case QDocument14 pagesEVA Vyaderm Case QMANSI SHARMANo ratings yet

- Dangers of DCF MortierDocument12 pagesDangers of DCF MortierKitti WongtuntakornNo ratings yet

- Einhorn Q4 2015Document7 pagesEinhorn Q4 2015CanadianValueNo ratings yet

- Starboard Value LP AAP Presentation 09.30.15Document23 pagesStarboard Value LP AAP Presentation 09.30.15marketfolly.com100% (1)

- The Incredible Shrinking Universe of StocksDocument29 pagesThe Incredible Shrinking Universe of StocksErsin Seçkin100% (1)

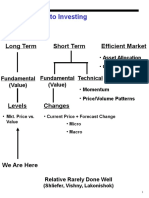

- Approaches To Investing: Long Term Short Term Efficient MarketDocument71 pagesApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeNo ratings yet

- The Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachFrom EverandThe Executive Guide to Boosting Cash Flow and Shareholder Value: The Profit Pool ApproachNo ratings yet

- Clear Thinking About Share RepurchaseDocument29 pagesClear Thinking About Share RepurchaseVrtpy CiurbanNo ratings yet

- H. Kevin Byun's Q4 2013 Denali Investors LetterDocument4 pagesH. Kevin Byun's Q4 2013 Denali Investors LetterValueInvestingGuy100% (1)

- Merits of CFROIDocument7 pagesMerits of CFROIfreemind3682No ratings yet

- Profit Guru Bill NygrenDocument5 pagesProfit Guru Bill NygrenekramcalNo ratings yet

- Day 3 Lecture SlidesDocument25 pagesDay 3 Lecture SlidesyebegashetNo ratings yet

- Allan Mecham Interview PDFDocument6 pagesAllan Mecham Interview PDFRajeev BahugunaNo ratings yet

- Klarman Yield PigDocument2 pagesKlarman Yield Pigalexg6No ratings yet

- Summary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingFrom EverandSummary of Bruce C. Greenwald, Judd Kahn & Paul D. Sonkin's Value InvestingNo ratings yet

- Seth Klarman's Baupost Fund Semi-Annual Report 19991Document24 pagesSeth Klarman's Baupost Fund Semi-Annual Report 19991nabsNo ratings yet

- Decision Making 36 Practice Questions & SolutionsDocument33 pagesDecision Making 36 Practice Questions & SolutionsAbdullah Naeem57% (7)

- Greenlight UnlockedDocument7 pagesGreenlight UnlockedZerohedgeNo ratings yet

- Entrepreneurship Development Workbook For LearnersDocument311 pagesEntrepreneurship Development Workbook For LearnersNoah Mzyece DhlaminiNo ratings yet

- Guggenheim ROIC PDFDocument16 pagesGuggenheim ROIC PDFJames PattersonNo ratings yet

- One Job: Counterpoint Global InsightsDocument25 pagesOne Job: Counterpoint Global Insightscartigayan100% (1)

- Competitive Advantage in Investing: Building Winning Professional PortfoliosFrom EverandCompetitive Advantage in Investing: Building Winning Professional PortfoliosNo ratings yet

- SuperInvestorInsight Issue 20Document10 pagesSuperInvestorInsight Issue 20johanschNo ratings yet

- Q&A With Bluegrass CapitalDocument9 pagesQ&A With Bluegrass CapitalPook Kei JinNo ratings yet

- Outperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueFrom EverandOutperform with Expectations-Based Management: A State-of-the-Art Approach to Creating and Enhancing Shareholder ValueNo ratings yet

- MS - Good Losses, Bad LossesDocument13 pagesMS - Good Losses, Bad LossesResearch ReportsNo ratings yet

- Aquamarine - 2013Document84 pagesAquamarine - 2013sb86No ratings yet

- Stan Druckenmiller Sohn TranscriptDocument8 pagesStan Druckenmiller Sohn Transcriptmarketfolly.com100% (1)

- Li Lu's 2010 Lecture at Columbia My Previous Transcript View A More Recent LectureDocument14 pagesLi Lu's 2010 Lecture at Columbia My Previous Transcript View A More Recent Lecturepa_langstrom100% (1)

- Lisa Rapuano Finding Your Way Along The Many Paths of ValueDocument29 pagesLisa Rapuano Finding Your Way Along The Many Paths of ValueValueWalk100% (1)

- On Streaks: Perception, Probability, and SkillDocument5 pagesOn Streaks: Perception, Probability, and Skilljohnwang_174817No ratings yet

- Carl Icahn's Letter To Apple's Tim CookDocument4 pagesCarl Icahn's Letter To Apple's Tim CookCanadianValueNo ratings yet

- Arithmetic of EquitiesDocument5 pagesArithmetic of Equitiesrwmortell3580No ratings yet

- Value Investor Insight Play Your GameDocument4 pagesValue Investor Insight Play Your Gamevouzvouz7127100% (1)

- Free Cash Flow Investing 04-18-11Document6 pagesFree Cash Flow Investing 04-18-11lowbankNo ratings yet

- To: From: Christopher M. Begg, CFA - CEO, Chief Investment Officer, and Co-Founder Date: July 16, 2012 ReDocument13 pagesTo: From: Christopher M. Begg, CFA - CEO, Chief Investment Officer, and Co-Founder Date: July 16, 2012 Recrees25No ratings yet

- Michael Mauboussin - Seeking Portfolio Manager Skill 2-24-12Document13 pagesMichael Mauboussin - Seeking Portfolio Manager Skill 2-24-12Phaedrus34No ratings yet

- Market Macro Myths Debts Deficits and DelusionsDocument13 pagesMarket Macro Myths Debts Deficits and DelusionsCanadianValueNo ratings yet

- Financial Fine Print: Uncovering a Company's True ValueFrom EverandFinancial Fine Print: Uncovering a Company's True ValueRating: 3 out of 5 stars3/5 (3)

- Active Alpha: A Portfolio Approach to Selecting and Managing Alternative InvestmentsFrom EverandActive Alpha: A Portfolio Approach to Selecting and Managing Alternative InvestmentsNo ratings yet

- Investor Call Re Valeant PharmaceuticalsDocument39 pagesInvestor Call Re Valeant PharmaceuticalsCanadianValueNo ratings yet

- Stan Druckenmiller The Endgame SohnDocument10 pagesStan Druckenmiller The Endgame SohnCanadianValueNo ratings yet

- 1995.12.13 - The More Things Change, The More They Stay The SameDocument20 pages1995.12.13 - The More Things Change, The More They Stay The SameYury PopovNo ratings yet

- Fill and KillDocument12 pagesFill and Killad9292No ratings yet

- Eminence CapitalMen's WarehouseDocument0 pagesEminence CapitalMen's WarehouseCanadianValueNo ratings yet

- Einhorn Consol PresentationDocument107 pagesEinhorn Consol PresentationCanadianValueNo ratings yet

- Munger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16Document12 pagesMunger-Daily Journal Annual Mtg-Adam Blum Notes-2!10!16CanadianValueNo ratings yet

- Summary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingFrom EverandSummary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingNo ratings yet

- Value Investing Congress NY 2010 AshtonDocument26 pagesValue Investing Congress NY 2010 Ashtonbrian4877No ratings yet

- Cafe Paradiso Sample Business PlanDocument48 pagesCafe Paradiso Sample Business Planehsaanuk100% (6)

- Budget Project - PAD 5227Document23 pagesBudget Project - PAD 5227Sabrina SmithNo ratings yet

- Amitabh Singhvi L MOI Interview L JUNE-2011Document6 pagesAmitabh Singhvi L MOI Interview L JUNE-2011Wayne GonsalvesNo ratings yet

- Redleaf Andy Absolute Return WhiteboxDocument6 pagesRedleaf Andy Absolute Return WhiteboxMatt Taylor100% (1)

- David Einhorn NYT-Easy Money - Hard TruthsDocument2 pagesDavid Einhorn NYT-Easy Money - Hard TruthstekesburNo ratings yet

- RV Capital June 2015 LetterDocument8 pagesRV Capital June 2015 LetterCanadianValueNo ratings yet

- Austrian Economics & InvestingDocument20 pagesAustrian Economics & InvestingRaj KumarNo ratings yet

- David Einhorn MSFT Speech-2006Document5 pagesDavid Einhorn MSFT Speech-2006mikesfbayNo ratings yet

- Boyar's Intrinsic Value Research Forgotten FourtyDocument49 pagesBoyar's Intrinsic Value Research Forgotten FourtyValueWalk100% (1)

- Aquamarine Fund PresentationDocument25 pagesAquamarine Fund PresentationVijay MalikNo ratings yet

- 5x5x5 InterviewDocument7 pages5x5x5 InterviewspachecofdzNo ratings yet

- Distressed Debt InvestingDocument5 pagesDistressed Debt Investingjt322No ratings yet

- Still Powerful - The Internet's Hidden OrderDocument17 pagesStill Powerful - The Internet's Hidden Orderpjs15No ratings yet

- Yacktman PresentationDocument34 pagesYacktman PresentationVijay MalikNo ratings yet

- Investing in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketFrom EverandInvesting in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketNo ratings yet

- The Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500Document6 pagesThe Stock Market As Monetary Policy Junkie Quantifying The Fed's Impact On The S P 500dpbasicNo ratings yet

- Hussman Funds Semi-Annual ReportDocument84 pagesHussman Funds Semi-Annual ReportCanadianValueNo ratings yet

- Charlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFDocument18 pagesCharlie Munger 2016 Daily Journal Annual Meeting Transcript 2 10 16 PDFaakashshah85No ratings yet

- KaseFundannualletter 2015Document20 pagesKaseFundannualletter 2015CanadianValueNo ratings yet

- Whitney Tilson Favorite Long and Short IdeasDocument103 pagesWhitney Tilson Favorite Long and Short IdeasCanadianValueNo ratings yet

- Letter To Clients and ShareholdersDocument3 pagesLetter To Clients and ShareholdersJulia Reynolds La RocheNo ratings yet

- Absolute Return Oct 2015Document9 pagesAbsolute Return Oct 2015CanadianValue0% (1)

- Wood Plastic Composite (WPC) Manufacturing Business-623225Document69 pagesWood Plastic Composite (WPC) Manufacturing Business-623225Zemenfes AbrehaNo ratings yet

- Examiner's Report: MA2 Managing Costs & Finance December 2012Document4 pagesExaminer's Report: MA2 Managing Costs & Finance December 2012Ahmad Hafid Hanifah100% (1)

- Reviewer in Intermediate Accounting (Midterm)Document9 pagesReviewer in Intermediate Accounting (Midterm)Czarhiena SantiagoNo ratings yet

- Becker DerivativesDocument15 pagesBecker DerivativesRhea Samson0% (1)

- Accounting For ManagersDocument14 pagesAccounting For ManagersKabo Lucas67% (3)

- TG Therapeutics Inc. (TGTX) - Reiterating Our Cautious View Ahead of Ublituximab's PDUFADocument10 pagesTG Therapeutics Inc. (TGTX) - Reiterating Our Cautious View Ahead of Ublituximab's PDUFASergey KNo ratings yet

- True Wealth & Savings: W I M T B WDocument61 pagesTrue Wealth & Savings: W I M T B WDonna Franciledo-Acero0% (1)

- Baskin Horror Decision TreeDocument9 pagesBaskin Horror Decision Treespectrum_480% (2)

- Solutions Chapter 8 - 2d EditionDocument29 pagesSolutions Chapter 8 - 2d Editionafsdasdf3qf4341f4asDNo ratings yet

- All in or Nothing: Brief History of Harish Chandra PrasadDocument3 pagesAll in or Nothing: Brief History of Harish Chandra PrasadRishav AnkitNo ratings yet

- Offer Letter - InternsDocument5 pagesOffer Letter - InternsAnkita SinghNo ratings yet

- Cacao Production in MindanaoDocument17 pagesCacao Production in MindanaoBREN G. CATUNAONo ratings yet

- CG RoadshowDocument33 pagesCG RoadshowSivaram NaiduNo ratings yet

- 01 - Karakteristik Organisasi Sektor PublikDocument12 pages01 - Karakteristik Organisasi Sektor PublikGabriel Sepania Parlindungan SianiparNo ratings yet

- Sugar Cane Plantation and Processing in EthiopiaDocument13 pagesSugar Cane Plantation and Processing in EthiopiaEduardo AlcivarNo ratings yet

- FX III PracticeDocument10 pagesFX III PracticeFinanceman4100% (1)

- Annual Report 2017Document208 pagesAnnual Report 2017Arham WaseemNo ratings yet

- 2012 Book of AccountsDocument27 pages2012 Book of AccountsChrismand CongeNo ratings yet

- Acc 252 Practice ExamDocument5 pagesAcc 252 Practice ExamEmy ManiyarNo ratings yet

- 1st Prelim Reviewer in FinanceDocument7 pages1st Prelim Reviewer in FinancemarieNo ratings yet

- Company Law Ii PDFDocument95 pagesCompany Law Ii PDFNYAMEKYE ADOMAKONo ratings yet

- Gist of IFRS 16Document6 pagesGist of IFRS 16Aswathy JejuNo ratings yet