You might also like

- 2010 Summer City Center Concerts, Danbury CTDocument1 page2010 Summer City Center Concerts, Danbury CTRick SchwartzNo ratings yet

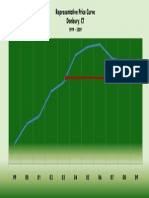

- Representative Price Curve 99-09Document1 pageRepresentative Price Curve 99-09Rick SchwartzNo ratings yet

- Representative Price Curve 05-09Document1 pageRepresentative Price Curve 05-09Rick SchwartzNo ratings yet

- Western CT Self Storage FacilitiesDocument1 pageWestern CT Self Storage FacilitiesRick SchwartzNo ratings yet

- Where Will The Jobs Come From: Source - The Kauffman FoundationDocument16 pagesWhere Will The Jobs Come From: Source - The Kauffman FoundationRick SchwartzNo ratings yet

- HVCASA Parent Awareness WorkshopDocument1 pageHVCASA Parent Awareness WorkshopRick SchwartzNo ratings yet

- Housing Help For UnemployedDocument3 pagesHousing Help For UnemployedRick SchwartzNo ratings yet

- myFICO Understanding Your Credit ScoreDocument20 pagesmyFICO Understanding Your Credit Scorecolonelcash100% (1)

- Weekdays Via Southeast Station To New FairfieldDocument2 pagesWeekdays Via Southeast Station To New FairfieldRick SchwartzNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Fundamentals of Retailing and Shopper MarketingDocument40 pagesFundamentals of Retailing and Shopper MarketingErose StNo ratings yet

- Rev CTA 8835 8790 Chevron Holdings Inc vs. CIRDocument20 pagesRev CTA 8835 8790 Chevron Holdings Inc vs. CIRJerome Delos ReyesNo ratings yet

- 1800s Lacked Self-Sufficiency Due To Limited Crops And Goods(39Document1 page1800s Lacked Self-Sufficiency Due To Limited Crops And Goods(39Garret Wilkenson SiaNo ratings yet

- OkcDocument2 pagesOkcpsiyer2000No ratings yet

- A Study On Digital Payment Awareness Among Small Scale VendorsDocument4 pagesA Study On Digital Payment Awareness Among Small Scale VendorsEditor IJTSRDNo ratings yet

- McKinsey 7 S FrameworkDocument9 pagesMcKinsey 7 S FrameworkRahul GautamNo ratings yet

- Quality Assessor Resume SampleDocument1 pageQuality Assessor Resume Sampleresume7.com100% (1)

- CSR DataDocument7 pagesCSR DataNilesh ShobhaneNo ratings yet

- Exam Financial ManagementDocument5 pagesExam Financial ManagementMaha MansoorNo ratings yet

- Revised Organizational Structure of Railway BoardDocument4 pagesRevised Organizational Structure of Railway BoardThirunavukkarasu ThirunavukkarasuNo ratings yet

- Promotion & DistributionDocument18 pagesPromotion & DistributionKertik SinghNo ratings yet

- Cheetah Digital Econsultancy 2022 Digital Consumer Trends Index Infographic 2Document1 pageCheetah Digital Econsultancy 2022 Digital Consumer Trends Index Infographic 2Mark MendozaNo ratings yet

- Macro Economics For Managers: Course HandoutDocument65 pagesMacro Economics For Managers: Course HandoutChetan WodeyarNo ratings yet

- 689140894Document7 pages689140894HATEMNo ratings yet

- Your Adv Plus Banking Preferred Rewards Gold: Account SummaryDocument6 pagesYour Adv Plus Banking Preferred Rewards Gold: Account SummaryGUILLERMO ALVAREZNo ratings yet

- Keynesian Liquidity Preference TheoryDocument12 pagesKeynesian Liquidity Preference TheorySatavisha RayNo ratings yet

- EY The Science of Winning in Financial ServicesDocument24 pagesEY The Science of Winning in Financial ServicesccmehtaNo ratings yet

- Llamasoft Gartner Issue1 PDFDocument22 pagesLlamasoft Gartner Issue1 PDFDarshan HDNo ratings yet

- TMF Forum API PosterDocument1 pageTMF Forum API PosterRamesh BalakrishnanNo ratings yet

- Svensson Case V Luxembourg - Case LawDocument2 pagesSvensson Case V Luxembourg - Case LawEzgi BaşNo ratings yet

- Prueba Pisa 2022 - Resultados de PerúDocument3 pagesPrueba Pisa 2022 - Resultados de PerúDiario GestiónNo ratings yet

- Social audit checklist for factory complianceDocument2 pagesSocial audit checklist for factory complianceRifat Ahmed100% (1)

- Entrepreneurship Development BBA Notes, EbookDocument80 pagesEntrepreneurship Development BBA Notes, EbookSatish Kumar RanjanNo ratings yet

- Auditing The Human Resource Management Process: © Mcgraw-Hill Education 2014 © Mcgraw-Hill Education 2014Document27 pagesAuditing The Human Resource Management Process: © Mcgraw-Hill Education 2014 © Mcgraw-Hill Education 2014NaeemNo ratings yet

- Prepared By: Dr. Riham AdelDocument26 pagesPrepared By: Dr. Riham AdelAbdelrahman GalalNo ratings yet

- The Social Pillar: Investing in The People of KenyaDocument44 pagesThe Social Pillar: Investing in The People of KenyaJerusha Kimani KoskeyNo ratings yet

- Assign 3 Sir FazeelDocument20 pagesAssign 3 Sir FazeelAmna ShahbazNo ratings yet

- Jola PublishingDocument4 pagesJola PublishingSabrina LaganàNo ratings yet

- 4.7 Ethical Issues Sales ManagementDocument12 pages4.7 Ethical Issues Sales ManagementRishab Jain 2027203No ratings yet

- Default notice promissory letterDocument4 pagesDefault notice promissory letterAlyssa Pinar AñanaNo ratings yet