You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- TD Business Convenience Plus: Account SummaryDocument4 pagesTD Business Convenience Plus: Account SummaryMarleny AriasNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

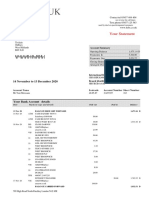

- 2020 12 13 - StatementDocument7 pages2020 12 13 - StatementToni MirosanuNo ratings yet

- Mar-2021, Apr-2021, May-2021, Jun-2021, Aug-2021Document4 pagesMar-2021, Apr-2021, May-2021, Jun-2021, Aug-2021James Franklin100% (3)

- It's A Civil Matter Report 110608Document19 pagesIt's A Civil Matter Report 110608Govan Law CentreNo ratings yet

- FIA FA1 Mock Exam - QuestionsDocument16 pagesFIA FA1 Mock Exam - Questionsmarlynrich3652100% (5)

- PDFDocument3 pagesPDFRojan BhattaraiNo ratings yet

- Debt Farming Report Dec 2011Document10 pagesDebt Farming Report Dec 2011Govan Law CentreNo ratings yet

- PF Glasgow V Parveen Akram-1Document6 pagesPF Glasgow V Parveen Akram-1Govan Law CentreNo ratings yet

- Letter To Alex Neil MSP 171109Document3 pagesLetter To Alex Neil MSP 171109Govan Law CentreNo ratings yet

- Mike Dailly's Opening Speech For The OppositionDocument4 pagesMike Dailly's Opening Speech For The OppositionGovan Law CentreNo ratings yet

- Stage1 Homeowner& DebtorProtecDocument4 pagesStage1 Homeowner& DebtorProtecGovan Law CentreNo ratings yet

- GLC Mediation ReportDocument43 pagesGLC Mediation ReportGovan Law CentreNo ratings yet

- Abolition of Poindings and Warrant Sales Bill - Stage 1 GLC Evidence 171199Document13 pagesAbolition of Poindings and Warrant Sales Bill - Stage 1 GLC Evidence 171199Govan Law CentreNo ratings yet

- UK Lloyds BankDocument3 pagesUK Lloyds BankflaviofernandezfigueiredoNo ratings yet

- 1 5136803172601299942 PDFDocument3 pages1 5136803172601299942 PDFnurulamin00023No ratings yet

- CHP 22 Business FinanceDocument6 pagesCHP 22 Business FinanceHiNo ratings yet

- INTERNSHIP BankDocument29 pagesINTERNSHIP Banksanmathi sundarNo ratings yet

- Sap In-House Cash Help Ecc6 Ehp8 Sp13 Part 1Document85 pagesSap In-House Cash Help Ecc6 Ehp8 Sp13 Part 1prognostech0% (2)

- Summer Training Finance Project On WORKING CAPITAL MANAGEMENTDocument264 pagesSummer Training Finance Project On WORKING CAPITAL MANAGEMENTHarmeet SinghNo ratings yet

- DI CFS FSI Outlook-BankingDocument70 pagesDI CFS FSI Outlook-Bankinghuizhi guoNo ratings yet

- Aasb 107 "Cash Flow Statements": Statement of Cash FlowsDocument5 pagesAasb 107 "Cash Flow Statements": Statement of Cash FlowsLin YaoNo ratings yet

- 17-Banking Services ProceduresDocument37 pages17-Banking Services ProceduresjayNo ratings yet

- Initiating Coverage On Olam International - Strong SellDocument133 pagesInitiating Coverage On Olam International - Strong SellFranck JocktaneNo ratings yet

- Wells Fargo Opportunity CheckingDocument4 pagesWells Fargo Opportunity Checkingson tungNo ratings yet

- Ucc 4Document66 pagesUcc 4Glenn Augenstein67% (3)

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- ECSS Regular Donation 20210319Document2 pagesECSS Regular Donation 20210319Hanny BoonNo ratings yet

- Vedic International SchoolDocument13 pagesVedic International SchoolRiyaNo ratings yet

- P2 Exam Practice KitDocument281 pagesP2 Exam Practice Kitimmaculate7933% (3)

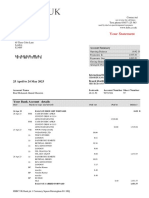

- 2023 05 24 - StatementDocument7 pages2023 05 24 - StatementRiad GhoneimNo ratings yet

- Russell Laffitte Sentencing MemorandumDocument35 pagesRussell Laffitte Sentencing MemorandumJoseph EricksonNo ratings yet

- Rights of Consumer Under Consumer Protection Act 1986 16-5-14Document70 pagesRights of Consumer Under Consumer Protection Act 1986 16-5-14anees.pathan2No ratings yet

- List of Services & Fees Effective Date: May 24, 2022: TD Canada TrustDocument7 pagesList of Services & Fees Effective Date: May 24, 2022: TD Canada TrustJor NormanNo ratings yet

- Banking FacilitiesDocument3 pagesBanking FacilitiesOsama AhmedNo ratings yet

- Mifos - Data - SheetJuly 2015 PDFDocument4 pagesMifos - Data - SheetJuly 2015 PDFmariaduque9No ratings yet

- Commercial Banks in IndiaDocument29 pagesCommercial Banks in IndiaVarsha SinghNo ratings yet

- Polytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsDocument15 pagesPolytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsYassi CurtisNo ratings yet

- Working CapitalDocument72 pagesWorking CapitalSyaapeNo ratings yet