You might also like

- Canadian Housing BubbleDocument52 pagesCanadian Housing Bubblecwinsor1No ratings yet

- Fundamental Index Newsletter January 2010Document5 pagesFundamental Index Newsletter January 2010api-26324170No ratings yet

- NullDocument8 pagesNullapi-26324170No ratings yet

- Fund Selector EditionDocument3 pagesFund Selector Editionapi-26324170No ratings yet

- 10Y and 2Y YieldsDocument1 page10Y and 2Y Yieldsapi-26324170No ratings yet

- A Bubble in Search of A PinDocument10 pagesA Bubble in Search of A Pinapi-26324170No ratings yet

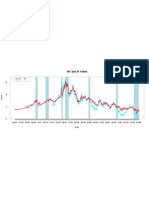

- 10yr 2yrDocument1 page10yr 2yrapi-26324170No ratings yet

- David A. Rosenberg Chief Economist & Strategist Drosenberg@Gluskinsheff - Com + 1Document7 pagesDavid A. Rosenberg Chief Economist & Strategist Drosenberg@Gluskinsheff - Com + 1api-26324170No ratings yet

- David Einhorn Speech Againts Lehman May 08Document9 pagesDavid Einhorn Speech Againts Lehman May 08Andri ChandraNo ratings yet

- Equities and Tobin's QDocument18 pagesEquities and Tobin's Qapi-26324170No ratings yet

- WSJ Says Gold Is A Lousy Investment. That Might VeryDocument6 pagesWSJ Says Gold Is A Lousy Investment. That Might Veryapi-26324170No ratings yet

- Gold and Your PortfolioDocument7 pagesGold and Your Portfolioapi-26324170No ratings yet

- Clarium Save Now Invest LaterDocument22 pagesClarium Save Now Invest Latermarketfolly.comNo ratings yet

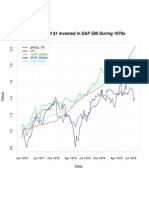

- Growth of $1 Invested in S&P 500 During 1970s: 10YR - BONDDocument1 pageGrowth of $1 Invested in S&P 500 During 1970s: 10YR - BONDapi-26324170No ratings yet

- San Fran Fed On BubblesDocument5 pagesSan Fran Fed On BubblesZerohedgeNo ratings yet

- Where's The Smoking Gun? A Study of Underwriting Standards For US Subprime MortgagesDocument38 pagesWhere's The Smoking Gun? A Study of Underwriting Standards For US Subprime Mortgagesapi-26324170No ratings yet

- Nomura EquityResearch The Business of AgeingDocument136 pagesNomura EquityResearch The Business of Ageingstarbak777No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Sadbhav Infrastructure ProjectDocument16 pagesSadbhav Infrastructure ProjectbardhanNo ratings yet

- 2013 CBA Annual Report 19 AuguCBAst 2013Document198 pages2013 CBA Annual Report 19 AuguCBAst 2013tusharyourfriend2958No ratings yet

- PolaroidDocument6 pagesPolaroidKumar100% (1)

- Yap Ling 1007Document35 pagesYap Ling 1007Shucheng ChamNo ratings yet

- Accounting Terms and ConceptsDocument4 pagesAccounting Terms and ConceptsNirajNo ratings yet

- Securities Fraud in The CourtsDocument32 pagesSecurities Fraud in The Courtsmike97% (38)

- Portfolio Investment ProcessDocument17 pagesPortfolio Investment ProcessPrashant DubeyNo ratings yet

- Axial Website - Transitioning CEO Tips - Some Points Here To Use in IOIkDocument6 pagesAxial Website - Transitioning CEO Tips - Some Points Here To Use in IOIkgalindoalfonsoNo ratings yet

- New Millennium Iron Corp. Announces Review Process For Taconite Project Heads of Agreement With Tata Steel (Company Update)Document3 pagesNew Millennium Iron Corp. Announces Review Process For Taconite Project Heads of Agreement With Tata Steel (Company Update)Shyam SunderNo ratings yet

- Orange Stock PitchDocument32 pagesOrange Stock PitchCameron FenNo ratings yet

- Jindal Steel EIC AnalysisDocument5 pagesJindal Steel EIC AnalysisNavneet MakhariaNo ratings yet

- Presentation ThyssenKrupp CS GS and MC PDFDocument95 pagesPresentation ThyssenKrupp CS GS and MC PDFSaran BaskarNo ratings yet

- IFRS 9 Part II Classification & Measurement CPD November 2015Document55 pagesIFRS 9 Part II Classification & Measurement CPD November 2015Nicolaus CopernicusNo ratings yet

- Green CriminologyDocument28 pagesGreen CriminologyCarmen FerranNo ratings yet

- Project Management: Generation & Screening of Project IdeasDocument16 pagesProject Management: Generation & Screening of Project Ideasshital_vyas1987No ratings yet

- Oslo Innovation Magazine WebDocument36 pagesOslo Innovation Magazine WebOslo Business MemoNo ratings yet

- Divya Merge PDFDocument86 pagesDivya Merge PDFLïkïth RäjNo ratings yet

- Cfa Curriculum: I. Ethical and Professional Standards (15%)Document2 pagesCfa Curriculum: I. Ethical and Professional Standards (15%)mohammad shadabNo ratings yet

- Investor Digest: Equity Research - 28 March 2019Document9 pagesInvestor Digest: Equity Research - 28 March 2019Rising PKN STANNo ratings yet

- of Kingfisher AirlinesDocument8 pagesof Kingfisher AirlinesSneha KumarNo ratings yet

- Eric ArroyoDocument2 pagesEric Arroyoeearroyo100% (1)

- By-Laws of The Namibian Savings and Credit CooperativeDocument18 pagesBy-Laws of The Namibian Savings and Credit CooperativeMilton LouwNo ratings yet

- ChitDocument9 pagesChitprashanthNo ratings yet

- Accounting As A Form of CommunicationDocument12 pagesAccounting As A Form of CommunicationLolNo ratings yet

- Shriram Finanace NewDocument43 pagesShriram Finanace NewRavi GuptaNo ratings yet

- Data AnanysisDocument14 pagesData AnanysisDrishty BishtNo ratings yet

- BBMF 2013 Tutorial 1Document5 pagesBBMF 2013 Tutorial 1BPLim94No ratings yet

- Gazprom Annual Report 2016 en PDFDocument200 pagesGazprom Annual Report 2016 en PDFMauricio AceroNo ratings yet

- Accounting As The Language of BusinessDocument2 pagesAccounting As The Language of BusinessjuliahuiniNo ratings yet