You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Airline ReportDocument9 pagesAirline ReportRaheel AhmedNo ratings yet

- Bis-Electrical Code Is - sp.30.2011Document411 pagesBis-Electrical Code Is - sp.30.2011Seema SharmaNo ratings yet

- Construction Contracts An AnalysisDocument29 pagesConstruction Contracts An Analysisemmanuel JohnyNo ratings yet

- Employement CertificateDocument1 pageEmployement Certificateemmanuel JohnyNo ratings yet

- Material of As 28Document48 pagesMaterial of As 28emmanuel JohnyNo ratings yet

- Highlight of Union Budget 2011-12Document11 pagesHighlight of Union Budget 2011-12emmanuel JohnyNo ratings yet

- Resources Transferred To States and U.T. Govt (Union Budget 2010-11 Tabular Presenation)Document2 pagesResources Transferred To States and U.T. Govt (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNo ratings yet

- Raju and The Money TreeDocument10 pagesRaju and The Money TreeChandan MundhraNo ratings yet

- Material of As 16Document21 pagesMaterial of As 16emmanuel JohnyNo ratings yet

- RBI MoneyKumar ComicDocument24 pagesRBI MoneyKumar Comicbhoopathy100% (1)

- Highlights of Central Plan 2010-2011 (Union Budget 2010-11 Tabular Presenation)Document8 pagesHighlights of Central Plan 2010-2011 (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNo ratings yet

- Revenue Account - DisbursementsDocument3 pagesRevenue Account - Disbursementsemmanuel JohnyNo ratings yet

- Receipts (Union Budget 2010-11 Tabular Presenation)Document2 pagesReceipts (Union Budget 2010-11 Tabular Presenation)emmanuel Johny100% (1)

- Central Plan Outlay by Ministries/Departments (Union Budget 2010-11 Tabular Presenation)Document4 pagesCentral Plan Outlay by Ministries/Departments (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNo ratings yet

- Central Plan Outlay by Sectors (Union Budget 2010-11 Tabular Presenation)Document2 pagesCentral Plan Outlay by Sectors (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNo ratings yet

- Expenditure (Union Budget 2010-11 Tabular Presenation)Document4 pagesExpenditure (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNo ratings yet

- Central Plan Outlay (Union Budget 2010-11 Tabular Presenation)Document1 pageCentral Plan Outlay (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNo ratings yet

- Revenue Account - ReceiptsDocument3 pagesRevenue Account - Receiptsemmanuel JohnyNo ratings yet

- Budget at A Glance (Union Budget 2010-11 Tabular Presenation)Document2 pagesBudget at A Glance (Union Budget 2010-11 Tabular Presenation)emmanuel JohnyNo ratings yet

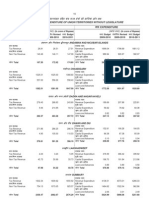

- Receipts and Expenditure of Union Territories Without LegislatureDocument1 pageReceipts and Expenditure of Union Territories Without Legislatureemmanuel JohnyNo ratings yet

- Macro Economic Framework Statement 2010 11Document6 pagesMacro Economic Framework Statement 2010 11emmanuel JohnyNo ratings yet

- Geprek BensuDocument16 pagesGeprek BensuPutri AriyaniNo ratings yet

- Next Gen BankingDocument8 pagesNext Gen BankingTarang Shah0% (1)

- Fashion IndustryDocument2 pagesFashion IndustryKadam BhavsarNo ratings yet

- European Crowdfunding Framework Oct 2012Document40 pagesEuropean Crowdfunding Framework Oct 2012Abigail KimNo ratings yet

- Amortization of A 30-Year, $130,000 Loan at 8.5%Document10 pagesAmortization of A 30-Year, $130,000 Loan at 8.5%Ponleu MamNo ratings yet

- Seem 3490Document5 pagesSeem 3490Gloria HigueraNo ratings yet

- Title XDocument9 pagesTitle XJana marieNo ratings yet

- Presentation HIRARCDocument12 pagesPresentation HIRARCahmad syouqiNo ratings yet

- PERMIAS Sponsorship Proposal 2022Document21 pagesPERMIAS Sponsorship Proposal 2022Sarah JasmineNo ratings yet

- Metrolab Industries Inc Vs Roldan-Confesor - 108855 - February 28 2996 - KapDocument28 pagesMetrolab Industries Inc Vs Roldan-Confesor - 108855 - February 28 2996 - KapJia Chu ChuaNo ratings yet

- Alex Boz CV PDFDocument2 pagesAlex Boz CV PDFAlex BozNo ratings yet

- Pfizer Annual Report - 2012-13Document92 pagesPfizer Annual Report - 2012-13Dipali ManjuchaNo ratings yet

- Invoice Samsung SoundBarDocument1 pageInvoice Samsung SoundBardumtakaNo ratings yet

- Company Law Tutorial Questions Semester 1-2014-2016Document3 pagesCompany Law Tutorial Questions Semester 1-2014-2016Latanya BridgemohanNo ratings yet

- Practice Makes Perfect: 28 June 2007 Nottingham Trent UniversityDocument16 pagesPractice Makes Perfect: 28 June 2007 Nottingham Trent UniversityArjun SinghNo ratings yet

- Resume HemaDocument2 pagesResume Hemaanil007rajuNo ratings yet

- Project of Pankaj MishraDocument69 pagesProject of Pankaj MishraNitesh SharmaNo ratings yet

- I) Increase in Utilities Expense J) Decrease in LandDocument3 pagesI) Increase in Utilities Expense J) Decrease in LandRosendo Bisnar Jr.No ratings yet

- Indian Frozen Yogurt MarketDocument14 pagesIndian Frozen Yogurt Marketaakriti aroraNo ratings yet

- Kajian Investasi Bisnis Hotel Budget Di Medan: Lokasi Bandara KualanamuDocument10 pagesKajian Investasi Bisnis Hotel Budget Di Medan: Lokasi Bandara KualanamufitrifirdaNo ratings yet

- Confirmation of Product Type Approval 14/FEB/2011: Beele Engineering BV Model Name(s) : Slipsil# Sealing PlugsDocument2 pagesConfirmation of Product Type Approval 14/FEB/2011: Beele Engineering BV Model Name(s) : Slipsil# Sealing PlugsleandroschroederNo ratings yet

- Questionnaire (Filled)Document3 pagesQuestionnaire (Filled)mayur0072007No ratings yet

- Home First Finance CompanyDocument12 pagesHome First Finance CompanyJ BNo ratings yet

- Perenco - Oil and Gas - A Leading Independent Exploration and Production CompanyDocument3 pagesPerenco - Oil and Gas - A Leading Independent Exploration and Production CompanyCHO ACHIRI HUMPHREYNo ratings yet

- Statement - Assumption PDFDocument7 pagesStatement - Assumption PDFShweta TomarNo ratings yet

- Accounting MaterialDocument161 pagesAccounting MaterialMithun Nair MNo ratings yet

- SWOT Analysis of Meezan BankDocument10 pagesSWOT Analysis of Meezan Banksufyanbutt007No ratings yet

- Bloomberg Markets - November 2013 USADocument142 pagesBloomberg Markets - November 2013 USAYong Liu100% (1)

- Samsung Redefining A BrandDocument7 pagesSamsung Redefining A BrandAditiaSoviaNo ratings yet