You might also like

- How To Stay Rational in An Irrational World - Vitaliy KatsenelsonDocument37 pagesHow To Stay Rational in An Irrational World - Vitaliy KatsenelsonVitaliyKatsenelson100% (23)

- VALUEx Vail 2014 - Visa PresentationDocument19 pagesVALUEx Vail 2014 - Visa PresentationVitaliyKatsenelson100% (1)

- VALUEx Vail 2014 - Visa PresentationDocument19 pagesVALUEx Vail 2014 - Visa PresentationVitaliyKatsenelson100% (1)

- How To Stay Rational in An Irrational World - Vitaliy KatsenelsonDocument37 pagesHow To Stay Rational in An Irrational World - Vitaliy KatsenelsonVitaliyKatsenelson100% (23)

- Closed End Funds A Unique OpportunityDocument13 pagesClosed End Funds A Unique OpportunityValueWalkNo ratings yet

- Investment Case For Blucora - Motiwala CapitalDocument19 pagesInvestment Case For Blucora - Motiwala CapitalCanadianValueNo ratings yet

- HealthSouth Presentation Laughing Water CapitalDocument29 pagesHealthSouth Presentation Laughing Water CapitalCanadianValueNo ratings yet

- ValueXVail 2013 - Dan FerrisDocument14 pagesValueXVail 2013 - Dan FerrisVitaliyKatsenelsonNo ratings yet

- ValueXVail 2013 - Ethan BergDocument35 pagesValueXVail 2013 - Ethan BergVitaliyKatsenelsonNo ratings yet

- Greg Porter Lancashire Holdings Limited - ValueX 2014 Presentation FinalDocument25 pagesGreg Porter Lancashire Holdings Limited - ValueX 2014 Presentation FinalValueWalkNo ratings yet

- ValueXVail 2012 - Barry PasikovDocument13 pagesValueXVail 2012 - Barry PasikovVitaliyKatsenelsonNo ratings yet

- QR Energy Qre Valuex Vail 2014Document3 pagesQR Energy Qre Valuex Vail 2014ValueWalkNo ratings yet

- Active Value Investing Process by Vitaliy Katsenelson, CFADocument16 pagesActive Value Investing Process by Vitaliy Katsenelson, CFAVitaliyKatsenelsonNo ratings yet

- ValueXVail 2013 - Brian BosseDocument51 pagesValueXVail 2013 - Brian BosseVitaliyKatsenelsonNo ratings yet

- ValueXVail 2013 - Chris KarlinDocument26 pagesValueXVail 2013 - Chris KarlinVitaliyKatsenelsonNo ratings yet

- Hiding in Plain Site: Diving Deeply Into SEC FilingsDocument8 pagesHiding in Plain Site: Diving Deeply Into SEC FilingsfootnotedNo ratings yet

- Vail ValueX Presentation PublicDocument35 pagesVail ValueX Presentation Publicmarketfolly.comNo ratings yet

- Value Investor Congress Las Vegas 2013 - I Like Big Dividends and I Cannot Lie - Vitaliy KatsenelsonDocument47 pagesValue Investor Congress Las Vegas 2013 - I Like Big Dividends and I Cannot Lie - Vitaliy KatsenelsonVitaliyKatsenelsonNo ratings yet

- Active Value Investing Process by Vitaliy Katsenelson, CFADocument16 pagesActive Value Investing Process by Vitaliy Katsenelson, CFAVitaliyKatsenelsonNo ratings yet

- ValueXVail 2012 - Jon MarkmanDocument39 pagesValueXVail 2012 - Jon MarkmanVitaliyKatsenelsonNo ratings yet

- ValueXVail 2012 - Joe CornellDocument13 pagesValueXVail 2012 - Joe CornellVitaliyKatsenelsonNo ratings yet

- ValueXVail 2012 - Kai ShihDocument30 pagesValueXVail 2012 - Kai ShihVitaliyKatsenelsonNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Chapter 1 Basic Consid & Formation FinalDocument50 pagesChapter 1 Basic Consid & Formation FinalTheresa Timonan86% (14)

- Cost of Environmental Degradation Training ManualDocument483 pagesCost of Environmental Degradation Training ManualNath RoussetNo ratings yet

- JP Morgan Chase - DeckDocument9 pagesJP Morgan Chase - DeckRahul Girish KumarNo ratings yet

- Aurora Textile Company (SPREADSHEET) F-1536X - FCVDocument15 pagesAurora Textile Company (SPREADSHEET) F-1536X - FCVPaco ColínNo ratings yet

- Financial Statement Analysis NotesDocument9 pagesFinancial Statement Analysis Notesshe lacks wordsNo ratings yet

- ACCA F3 Exam Kit 2013 Emile Woolf PDFDocument181 pagesACCA F3 Exam Kit 2013 Emile Woolf PDFTinh Linh90% (20)

- Financial Accounting and Reporting EllioDocument181 pagesFinancial Accounting and Reporting EllioThủy Thiều Thị HồngNo ratings yet

- Set 1 PM - ADocument36 pagesSet 1 PM - AMUHAMMAD SAFWAN AHMAD MUSLIMNo ratings yet

- Advanced Accounting ExamDocument10 pagesAdvanced Accounting ExamMendoza Ron NixonNo ratings yet

- Chapter Five: Tax Avoidance and EvasionDocument14 pagesChapter Five: Tax Avoidance and Evasionembiale ayaluNo ratings yet

- 11 16 18 10 06 705Document2 pages11 16 18 10 06 705Finance - SnackerStreetNo ratings yet

- MRSUQ2C04Document2 pagesMRSUQ2C04Chinna ThambiNo ratings yet

- Finnish TaxationDocument217 pagesFinnish TaxationTobi MemoryNo ratings yet

- Sporting Business Value and Price - DamodaranDocument20 pagesSporting Business Value and Price - DamodaranFrancisco AlemanNo ratings yet

- Front Office TerminologyDocument7 pagesFront Office TerminologyKiran Mayi67% (3)

- AnupamDocument61 pagesAnupamviralNo ratings yet

- Logistics CostingDocument21 pagesLogistics CostingRuchita RajaniNo ratings yet

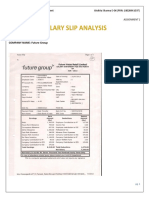

- Sector: Retail COMPANY NAME: Future GroupDocument3 pagesSector: Retail COMPANY NAME: Future GroupAkshita SharmaNo ratings yet

- Role of Board of DirectorsDocument3 pagesRole of Board of DirectorsFarhan JawedNo ratings yet

- Skripsi Rifa'atul Mahmudah "Analisis Usaha Jamur Tiram"Document89 pagesSkripsi Rifa'atul Mahmudah "Analisis Usaha Jamur Tiram"Rifa'atul Mahmudah Al Masir100% (1)

- Accbusco Chapter 16Document14 pagesAccbusco Chapter 16PaupauNo ratings yet

- Act 624 Finance No.2 Act 2002Document23 pagesAct 624 Finance No.2 Act 2002Adam Haida & CoNo ratings yet

- Khuram Cement TuanaDocument115 pagesKhuram Cement TuanaZeeshan ChaudhryNo ratings yet

- FI515 Homework1Document5 pagesFI515 Homework1andiemaeNo ratings yet

- Cost SheetDocument4 pagesCost SheetQuestionscastle FriendNo ratings yet

- Housekeeping ProposalDocument2 pagesHousekeeping Proposalprabhav_rrcNo ratings yet

- Auditing Project Sem 3Document33 pagesAuditing Project Sem 3Vivek Tiwari50% (2)

- FAR - Learning Assessment 2 - For PostingDocument6 pagesFAR - Learning Assessment 2 - For PostingDarlene JacaNo ratings yet

- ISE 2040 Excel HWDocument20 pagesISE 2040 Excel HWPatch HavanasNo ratings yet