You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Facebook 2010 Law Enforcement GuidelinesDocument5 pagesFacebook 2010 Law Enforcement GuidelinesbowssenNo ratings yet

- Rebels With A Cause: The December 2008 Greek Youth Movement As The Condensation of Deeper Social and Political ContradictionsDocument7 pagesRebels With A Cause: The December 2008 Greek Youth Movement As The Condensation of Deeper Social and Political ContradictionsbowssenNo ratings yet

- The Impact of The Global Financial Crisis On Social Protection in Developing CountriesDocument15 pagesThe Impact of The Global Financial Crisis On Social Protection in Developing CountriesbowssenNo ratings yet

- Beyond BPDocument2 pagesBeyond BPbowssenNo ratings yet

- A Toolbox For Stronger Economic Governance in EuropeDocument3 pagesA Toolbox For Stronger Economic Governance in EuropebowssenNo ratings yet

- Social Watch Report 2009 - Making Finances Work: People FirstDocument228 pagesSocial Watch Report 2009 - Making Finances Work: People FirstbowssenNo ratings yet

- Civil Society Background Document On The UN Conference On The World Financial and Economic Crisis and Its Impact On DevelopmentDocument9 pagesCivil Society Background Document On The UN Conference On The World Financial and Economic Crisis and Its Impact On DevelopmentbowssenNo ratings yet

- What Needs To Be DoneDocument9 pagesWhat Needs To Be DonebowssenNo ratings yet

- István Mészáros, Pathfinder of SocialismDocument4 pagesIstván Mészáros, Pathfinder of SocialismbowssenNo ratings yet

- The Credit CrisisDocument13 pagesThe Credit CrisisbowssenNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Tax Motivated Film Financing at Rexford StudiosDocument13 pagesTax Motivated Film Financing at Rexford StudiosNiketPaithankarNo ratings yet

- BPI V Trinidad DigestDocument2 pagesBPI V Trinidad DigestTon Ton CananeaNo ratings yet

- Guingona V City FiscalDocument1 pageGuingona V City FiscalFaye Jennifer Pascua PerezNo ratings yet

- Spouses Silos v. PNBDocument2 pagesSpouses Silos v. PNBFrancisco Ashley AcedilloNo ratings yet

- Internet BankingDocument93 pagesInternet BankingRajesh TyagiNo ratings yet

- SFCK PresentnDocument43 pagesSFCK PresentnFasna FathimaNo ratings yet

- 12 Chapter 9 - Risk Management in Banks NBFCsDocument4 pages12 Chapter 9 - Risk Management in Banks NBFCsgarima_kukreja_dceNo ratings yet

- Bcom 25 04Document278 pagesBcom 25 04Abila RevathyNo ratings yet

- The Federal Savings & Loan Insurance Corp., Etc., and First Gibraltar Bank, FSB, Intervenor-Appellee v. Jack Griffin, 935 F.2d 691, 1st Cir. (1991)Document15 pagesThe Federal Savings & Loan Insurance Corp., Etc., and First Gibraltar Bank, FSB, Intervenor-Appellee v. Jack Griffin, 935 F.2d 691, 1st Cir. (1991)Scribd Government DocsNo ratings yet

- Commercial Banking in IndiaDocument11 pagesCommercial Banking in IndiaTony SharmaNo ratings yet

- Jaime Cooper Consulting (Business Development Resume)Document2 pagesJaime Cooper Consulting (Business Development Resume)jcooper_bostonNo ratings yet

- Alice Blue Financial Service PVT LTD: Client Registration FormDocument26 pagesAlice Blue Financial Service PVT LTD: Client Registration FormAzhar ShaikhNo ratings yet

- Credit Authorisation SchemeDocument6 pagesCredit Authorisation SchemeOngwang KonyakNo ratings yet

- Cash and Cash Equivalents C5 Valix 2006Document5 pagesCash and Cash Equivalents C5 Valix 2006Ghaill CruzNo ratings yet

- Banking Laws Cases Part 1Document181 pagesBanking Laws Cases Part 1Keisha Yna V. RamirezNo ratings yet

- Statement 115377 Oct-2022Document8 pagesStatement 115377 Oct-2022Mary MacLellanNo ratings yet

- SWOT Analysis Template For YOUR ROCKSTAR FINTECH: Strengths OpportunitiesDocument2 pagesSWOT Analysis Template For YOUR ROCKSTAR FINTECH: Strengths OpportunitiesAntónio FerreiraNo ratings yet

- Export Credit Agencies - The Unsung Giants of International Trade and FinanceDocument207 pagesExport Credit Agencies - The Unsung Giants of International Trade and Financeace187No ratings yet

- Developing A Vision For Financial InclusionDocument75 pagesDeveloping A Vision For Financial InclusionnasiddikNo ratings yet

- Swot Analysis of MCBDocument4 pagesSwot Analysis of MCBAbdulMoeedMalikNo ratings yet

- Status and Future Scope of Floriculture in SLDocument10 pagesStatus and Future Scope of Floriculture in SLJames HavocNo ratings yet

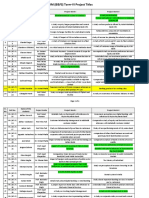

- PGDM (B&FS) Project Titles-1Document5 pagesPGDM (B&FS) Project Titles-1PranitNo ratings yet

- 2013-12-22Document2 pages2013-12-22Simbarashe MarisaNo ratings yet

- Banc One Case Study PDF FreeDocument10 pagesBanc One Case Study PDF FreeFathima KamalNo ratings yet

- Case Study 1234Document2 pagesCase Study 1234Gemma RetesNo ratings yet

- Khan Muhammad: PeshawarDocument3 pagesKhan Muhammad: PeshawarBilalKhanNo ratings yet

- TheEconomist 2022 05 14Document314 pagesTheEconomist 2022 05 14bibi michelleNo ratings yet

- Ebill 0101266763Document2 pagesEbill 0101266763Dele OlatunjiNo ratings yet

- Innovation in Indian Banking Sector UseDocument14 pagesInnovation in Indian Banking Sector UseKamran YousafNo ratings yet

- Federal Deposit Insurance Corporation, Etc. v. Leonard Caporale, Etc., 931 F.2d 1, 1st Cir. (1991)Document4 pagesFederal Deposit Insurance Corporation, Etc. v. Leonard Caporale, Etc., 931 F.2d 1, 1st Cir. (1991)Scribd Government DocsNo ratings yet