You might also like

- Marketing of Consumer Financial Products: Insights From Service MarketingFrom EverandMarketing of Consumer Financial Products: Insights From Service MarketingNo ratings yet

- Measuring Progress on Women's Financial Inclusion and Entrepreneurship in the Philippines: Results from Micro, Small, and Medium-Sized Enterprise SurveyFrom EverandMeasuring Progress on Women's Financial Inclusion and Entrepreneurship in the Philippines: Results from Micro, Small, and Medium-Sized Enterprise SurveyNo ratings yet

- 7.P Syamala DeviDocument4 pages7.P Syamala DeviSachin SahooNo ratings yet

- Micro Finance - Keys & Challenges:-A Review Mohit RewariDocument13 pagesMicro Finance - Keys & Challenges:-A Review Mohit Rewarisonia khuranaNo ratings yet

- Problems Faced by Borrowers of Micro FinanceDocument19 pagesProblems Faced by Borrowers of Micro Financepassionpec100% (1)

- Chapter 4 Rural Banking and Micro Financing 1Document16 pagesChapter 4 Rural Banking and Micro Financing 1saloniNo ratings yet

- Financial Inclusion & Financial Literacy: SBI InitiativesDocument5 pagesFinancial Inclusion & Financial Literacy: SBI Initiativesprashaant4uNo ratings yet

- Assignment 3 Part ADocument6 pagesAssignment 3 Part AALEN AUGUSTINENo ratings yet

- CRISIL Ratings India Top 50 MfisDocument68 pagesCRISIL Ratings India Top 50 MfisDavid Raju GollapudiNo ratings yet

- SMART PUSHNOTE - An Agent Based Intelligent Push Notification System 2017-18Document60 pagesSMART PUSHNOTE - An Agent Based Intelligent Push Notification System 2017-18sachin mohanNo ratings yet

- State Bank of India: First Five Year PlanDocument5 pagesState Bank of India: First Five Year PlanrirannaNo ratings yet

- Lack CollateralDocument4 pagesLack CollateralMudassir AliNo ratings yet

- Feature ArticleDocument4 pagesFeature Articlechan DesignsNo ratings yet

- Banking - Banking Sector in IndiaDocument65 pagesBanking - Banking Sector in Indiapraveen_rautela100% (1)

- Micro-Finance in The India: The Changing Face of Micro-Credit SchemesDocument11 pagesMicro-Finance in The India: The Changing Face of Micro-Credit SchemesMahesh ChavanNo ratings yet

- Microfinance Research PaperfinalDocument9 pagesMicrofinance Research PaperfinalChauhan NeelamNo ratings yet

- Sustainability of MFI's in India After Y.H.Malegam CommitteeDocument18 pagesSustainability of MFI's in India After Y.H.Malegam CommitteeAnup BmNo ratings yet

- The Future of Microfinance in IndiaDocument3 pagesThe Future of Microfinance in IndiaSurbhi AgarwalNo ratings yet

- Strategic Plans of Microfinance FirmDocument23 pagesStrategic Plans of Microfinance FirmAnatol PaladeNo ratings yet

- Project On Micro FinanceDocument44 pagesProject On Micro Financeredrose_luv23o.in@yahoo.co.in88% (8)

- FinancDocument3 pagesFinancRahul Rao JanagamNo ratings yet

- Ujjivan's Commitment To Help India's Urban Poor: Parinaam FoundationDocument3 pagesUjjivan's Commitment To Help India's Urban Poor: Parinaam Foundationrecoil25No ratings yet

- FINLATICSDocument9 pagesFINLATICSshweta lotNo ratings yet

- What Is Financial Inclusion: Chillibreeze WriterDocument4 pagesWhat Is Financial Inclusion: Chillibreeze WriterTenzin SontsaNo ratings yet

- BEPDocument9 pagesBEPDebashree NandaNo ratings yet

- Project On Standard Charted BankDocument82 pagesProject On Standard Charted BankViPul82% (11)

- Report On Micro FinanceDocument55 pagesReport On Micro Financearvind.vns14395% (73)

- Srushti Mahale - Pol Sci Ca 2Document9 pagesSrushti Mahale - Pol Sci Ca 2srushtijmahaleNo ratings yet

- Awareness of MicrofinanceDocument34 pagesAwareness of MicrofinanceDisha Tiwari100% (1)

- 13 - Conclusion and SuggestionsDocument4 pages13 - Conclusion and SuggestionsjothiNo ratings yet

- A Study On Cooperative and Microfinance: Assignment 1Document8 pagesA Study On Cooperative and Microfinance: Assignment 1Anjali PaneruNo ratings yet

- Project On Micro FinanceDocument68 pagesProject On Micro FinanceKapil RaoNo ratings yet

- Project On Micro Finance by Bragesh BahadurDocument119 pagesProject On Micro Finance by Bragesh BahadurMohit SachdevNo ratings yet

- Chapter - 1Document53 pagesChapter - 1Divya RatnagiriNo ratings yet

- Research Paper Suhail Khakil 2010Document13 pagesResearch Paper Suhail Khakil 2010Khaki AudilNo ratings yet

- MicrofinanceDocument58 pagesMicrofinanceSamuel Davis100% (1)

- Rural Entrepreneurship - Byst An Entrepreneurship Case - Study in Faridabad"Document12 pagesRural Entrepreneurship - Byst An Entrepreneurship Case - Study in Faridabad"nagajagreenNo ratings yet

- SIP PresentationDocument24 pagesSIP PresentationGorang MuthaNo ratings yet

- Training Report PGBDocument88 pagesTraining Report PGBsonampandhiNo ratings yet

- IJRAR19D1475Document11 pagesIJRAR19D1475niloferpasha95No ratings yet

- Statement of PurposeDocument5 pagesStatement of PurposeShalini SinghNo ratings yet

- Micro Finance in IndiaDocument59 pagesMicro Finance in IndiaApurva Bangera100% (1)

- Problem Statement 2017Document5 pagesProblem Statement 2017PG93No ratings yet

- Microfinance ResearchDocument17 pagesMicrofinance ResearchKausik KskNo ratings yet

- What Is Financial InclusionDocument10 pagesWhat Is Financial InclusionSanjeev ReddyNo ratings yet

- 07 - Chapter 1 MudraDocument16 pages07 - Chapter 1 Mudrayogesh sharmaNo ratings yet

- Initiatives: Financial Inclusion and Financial Literacy: Andhra Bank'sDocument8 pagesInitiatives: Financial Inclusion and Financial Literacy: Andhra Bank'sJagamohan OjhaNo ratings yet

- SvatantraDocument9 pagesSvatantradevilcaeser2010No ratings yet

- Group 9 - EE - Role of Microfinance - CompressedDocument31 pagesGroup 9 - EE - Role of Microfinance - CompressedSwati PorwalNo ratings yet

- AcknowledgementDocument18 pagesAcknowledgementpurnimapibmNo ratings yet

- Minukumari Amity ProposalDocument6 pagesMinukumari Amity ProposalMinu kumariNo ratings yet

- Accounting and Auditing Update October 2014Document32 pagesAccounting and Auditing Update October 2014bhatepoonamNo ratings yet

- Micro FinanceDocument33 pagesMicro Financemohit katoleNo ratings yet

- 05 Chapter-1 PDFDocument52 pages05 Chapter-1 PDFRohitNo ratings yet

- The Future of Microfinance in IndiaDocument6 pagesThe Future of Microfinance in Indiaanushri2No ratings yet

- The Functional Microfinance Bank: Strategies for SurvivalFrom EverandThe Functional Microfinance Bank: Strategies for SurvivalNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Financial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeFrom EverandFinancial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeNo ratings yet

- Employee WelfareDocument76 pagesEmployee Welfareni123sha67% (6)

- CaseDocument5 pagesCaseAshish GuptaNo ratings yet

- HSBCDocument2 pagesHSBCAshish GuptaNo ratings yet

- Case: - : Foldrite Furniture Co.: Planning To Meet A Surge in DemandDocument19 pagesCase: - : Foldrite Furniture Co.: Planning To Meet A Surge in DemandAshish Gupta100% (1)

- Indian Distributor'S Information SystemDocument19 pagesIndian Distributor'S Information SystemAshish GuptaNo ratings yet

- Global Shipping at Erken Apparel International: Group No: 9, Section: BDocument23 pagesGlobal Shipping at Erken Apparel International: Group No: 9, Section: BAshish Gupta50% (2)

- Leveraging Digital Channels For Enhancing Customer Experience and Analysis of Micro MarketsDocument22 pagesLeveraging Digital Channels For Enhancing Customer Experience and Analysis of Micro MarketsTashioNo ratings yet

- Internet BankingDocument67 pagesInternet BankingRaj Kumar0% (2)

- FAR Preweek Lecture (B42)Document14 pagesFAR Preweek Lecture (B42)Ciarie Mae Salgado50% (4)

- Analisis Perbandingan Kinerja Keuangan Pada PT Kalbe Farma TBK Dan Kimia Farma TBK PERIODE 2014 - 2016Document18 pagesAnalisis Perbandingan Kinerja Keuangan Pada PT Kalbe Farma TBK Dan Kimia Farma TBK PERIODE 2014 - 2016BAngelina Christy WalangitanNo ratings yet

- Sec Cert Sample - Bank AcctDocument2 pagesSec Cert Sample - Bank AcctJennifer Peng NavarreteNo ratings yet

- Icici 2Document9 pagesIcici 2Hack MeNo ratings yet

- CH 06Document84 pagesCH 06Indah LestariNo ratings yet

- Fedai Daily Quiz Questions Archives - Bank Accounts: Correct Answer: 2 Correct Answer: 2Document22 pagesFedai Daily Quiz Questions Archives - Bank Accounts: Correct Answer: 2 Correct Answer: 2Somdutt Gujjar100% (2)

- Ey Good Group Alternative Format 2021Document163 pagesEy Good Group Alternative Format 2021Michael Boules100% (1)

- Seabank Statement FEB PDFDocument1 pageSeabank Statement FEB PDFMhd Aref SiregarNo ratings yet

- Conference Call Presentation 2021Document36 pagesConference Call Presentation 2021suedtNo ratings yet

- MBBsavings - 158118 107625 - 2016 12 31Document7 pagesMBBsavings - 158118 107625 - 2016 12 31Zahar ZekNo ratings yet

- NN IP Guidebook To Alternative CreditDocument140 pagesNN IP Guidebook To Alternative CreditBernardNo ratings yet

- Annual Report - Norinchukin BankDocument180 pagesAnnual Report - Norinchukin BankSenthil KumaranNo ratings yet

- Final Report KasbDocument70 pagesFinal Report KasbtrueliarerNo ratings yet

- ACC 503: Chapter 10 - Exercise 1Document8 pagesACC 503: Chapter 10 - Exercise 1BaderNo ratings yet

- Chapter 02 MOOCDocument30 pagesChapter 02 MOOCNur JulianieNo ratings yet

- BharatPe Corporate ProfileDocument5 pagesBharatPe Corporate Profileoneoceannetwork3No ratings yet

- Financial System in MalaysiaDocument8 pagesFinancial System in MalaysiaqairunnisaNo ratings yet

- Cambridge O Level: Accounting 7707/23Document15 pagesCambridge O Level: Accounting 7707/23Prince AhmedNo ratings yet

- At A Glance Corporate Fact SheetDocument4 pagesAt A Glance Corporate Fact SheetpanchoNo ratings yet

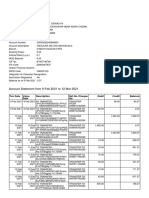

- Account Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceABHINAV DEWALIYANo ratings yet

- Bibliography: BooksDocument14 pagesBibliography: BooksDilip KumarNo ratings yet

- Ayala Corp Reflection PaperDocument4 pagesAyala Corp Reflection PaperAaron HuangNo ratings yet

- 021CLSM012 Innovations in Indian Banking Sector.Document4 pages021CLSM012 Innovations in Indian Banking Sector.SasidharNo ratings yet

- ITC Corporate ValuationDocument6 pagesITC Corporate ValuationSakshi Jain Jaipuria JaipurNo ratings yet

- CE Period CloseDocument11 pagesCE Period CloseMd MuzaffarNo ratings yet

- MR - Yogesh Daulat Chhaproo: Page 1 of 2 M-864489Document2 pagesMR - Yogesh Daulat Chhaproo: Page 1 of 2 M-864489Yogesh ChhaprooNo ratings yet

- AFB-Short Notes by Murugan - Bonds (Finance) - Present ValueDocument123 pagesAFB-Short Notes by Murugan - Bonds (Finance) - Present ValueJITENDRA KUMAR AVINASHINo ratings yet

- Eastern Bank Limited: Name: ID: American International University of Bangladesh Course Name: Faculty Name: Due DateDocument6 pagesEastern Bank Limited: Name: ID: American International University of Bangladesh Course Name: Faculty Name: Due DateTasheen MahabubNo ratings yet