You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Running Head: A Financial Forecast For New World Chemicals IncDocument9 pagesRunning Head: A Financial Forecast For New World Chemicals IncTimNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Financial Analysis ToolDocument50 pagesFinancial Analysis ToolContessa PetriniNo ratings yet

- Tesla'S Valuation & Financial ModelingDocument7 pagesTesla'S Valuation & Financial ModelingElliNo ratings yet

- Strategic ManagementDocument5 pagesStrategic Managementmohit789No ratings yet

- Ethics or MoneyDocument3 pagesEthics or Moneymohit789No ratings yet

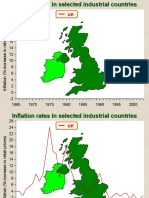

- Inflation Rates in Different EconomiesDocument10 pagesInflation Rates in Different Economiesmohit789No ratings yet

- Inflation Rates in Different EconomiesDocument10 pagesInflation Rates in Different Economiesmohit789No ratings yet

- FiiDocument18 pagesFiiVinod KumarNo ratings yet

- Inflation Rates in Different EconomiesDocument10 pagesInflation Rates in Different Economiesmohit789No ratings yet

- Strategic ManagementDocument20 pagesStrategic Managementmohit789No ratings yet

- Article Harcopy PartDocument2 pagesArticle Harcopy Partmohit789No ratings yet

- Activity 3 - TolentinoDocument7 pagesActivity 3 - TolentinoDJazel Tolentino100% (1)

- 15 A Introduction To Financial Statement Analysis - AnswersDocument13 pages15 A Introduction To Financial Statement Analysis - AnswersNhi Cúnn'ssNo ratings yet

- KietPHMSS170832 ACC101 Individual AssignmentDocument17 pagesKietPHMSS170832 ACC101 Individual AssignmentMinh Kiet Pham HuuNo ratings yet

- Raymond LTD Balance SheetDocument15 pagesRaymond LTD Balance Sheetvaibhav guptaNo ratings yet

- 1 Adoption - of - IFRS - Spain PDFDocument31 pages1 Adoption - of - IFRS - Spain PDFJULIO CESAR MILLAN SOLARTENo ratings yet

- Lembar Kerja PT PAULIN ABADI SEJAHTERADocument7 pagesLembar Kerja PT PAULIN ABADI SEJAHTERAguillaume amaryllisNo ratings yet

- Engineering Economics FormulasDocument5 pagesEngineering Economics FormulasDeo WarrenNo ratings yet

- Fundamental Accounting Principles Canadian Vol 2 Canadian 14th Edition Larson Solutions ManualDocument46 pagesFundamental Accounting Principles Canadian Vol 2 Canadian 14th Edition Larson Solutions Manualstarlikeharrowerexwp5100% (27)

- Adjusting Entries and Promissory NotesDocument6 pagesAdjusting Entries and Promissory Noteselma wagwagNo ratings yet

- Quiz Budgeting and Standard CostingDocument2 pagesQuiz Budgeting and Standard CostingAli SwizzleNo ratings yet

- 006 Discounted Dividend Valuation PDFDocument71 pages006 Discounted Dividend Valuation PDFAprajita VishainNo ratings yet

- Report On Fundamental Analysis of EquityDocument56 pagesReport On Fundamental Analysis of EquityHarshada Jadhav100% (1)

- Indvi Assignment 2 Investment and Port MGTDocument3 pagesIndvi Assignment 2 Investment and Port MGTaddisie temesgen100% (1)

- Test 3 QuestionsDocument8 pagesTest 3 QuestionsArt and Fashion galleryNo ratings yet

- Adam SugarDocument11 pagesAdam SugarshirazhaqNo ratings yet

- 2018 Problem&Solution MojakoeDocument19 pages2018 Problem&Solution Mojakoedara ibthiaNo ratings yet

- AS14Document13 pagesAS14Browse PurposeNo ratings yet

- Capital Structure and Firm ValueDocument22 pagesCapital Structure and Firm ValueGaurav gusaiNo ratings yet

- Financial PerformanceDocument76 pagesFinancial Performancesatishj8750% (2)

- SolutionDocument23 pagesSolutionKavita WadhwaNo ratings yet

- Acc 1102Document19 pagesAcc 1102Bonatan S. MuzzammilNo ratings yet

- Break Even Analysis TotalDocument3 pagesBreak Even Analysis Totalm.rahimianNo ratings yet

- Insurance AccountingDocument34 pagesInsurance Accountingrcpgeneral100% (1)

- (Financial Analysis) MANALO, Frances M. LM2-1Document3 pages(Financial Analysis) MANALO, Frances M. LM2-11900118No ratings yet

- PST Quiz PA Chap 2Document5 pagesPST Quiz PA Chap 2Phuong PhamNo ratings yet

- MEDINA - Homework 2 (Midterm)Document9 pagesMEDINA - Homework 2 (Midterm)Von Andrei MedinaNo ratings yet

- CH.7 Plant Assets, Natural Resources, & IntangiblesDocument98 pagesCH.7 Plant Assets, Natural Resources, & IntangiblesJuan Andres MarquezNo ratings yet