You might also like

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Detailed Scenario Analysis of Microsoft's Acquisition of SkypeDocument42 pagesDetailed Scenario Analysis of Microsoft's Acquisition of SkypeStephen Castellano67% (3)

- 5 Stock To DoubleDocument25 pages5 Stock To DoubleLao ZhuNo ratings yet

- Crocs Case AnalysisDocument8 pagesCrocs Case Analysissiddis316No ratings yet

- LTCMDocument2 pagesLTCMskalidasNo ratings yet

- 10 Highest Rated Stocks - ToolsDocument15 pages10 Highest Rated Stocks - Toolsanon-469745100% (4)

- Ten Baggers Portfolio AmbitDocument18 pagesTen Baggers Portfolio AmbitPuneet367No ratings yet

- 15分鐘告訴你回報率在15%或更多的保險類股票Document15 pages15分鐘告訴你回報率在15%或更多的保險類股票jjy1234No ratings yet

- Best Stock Picks of Best Hedge FundsDocument141 pagesBest Stock Picks of Best Hedge FundsstockholmesNo ratings yet

- The Outlook: Tech KnowledgeDocument8 pagesThe Outlook: Tech KnowledgeNorbertCampeauNo ratings yet

- Third Point Q2 15Document10 pagesThird Point Q2 15marketfolly.comNo ratings yet

- Spin OffsDocument5 pagesSpin Offseurodental5923100% (1)

- Ufa#Ed 2#Sol#Chap 06Document18 pagesUfa#Ed 2#Sol#Chap 06api-3824657No ratings yet

- Investopedia - Advanced Financial Statement Analysis (2006)Document74 pagesInvestopedia - Advanced Financial Statement Analysis (2006)Denis100% (40)

- Ten Baggers - AmbitDocument18 pagesTen Baggers - Ambitsh_niravNo ratings yet

- Delgado - Forex: The Fundamental Analysis.Document10 pagesDelgado - Forex: The Fundamental Analysis.Franklin Delgado VerasNo ratings yet

- 7stock ReportDocument11 pages7stock ReportNacharyZewellNo ratings yet

- Greenhaven+ (2018+Q2)Document10 pagesGreenhaven+ (2018+Q2)l chanNo ratings yet

- 5 Safe and Cheap Dividend Stocks To Invest in (February 2021) - Seeking AlphaDocument12 pages5 Safe and Cheap Dividend Stocks To Invest in (February 2021) - Seeking Alphachang liuNo ratings yet

- Fundamental Analysis Versus Technical AnalysisDocument12 pagesFundamental Analysis Versus Technical AnalysisShakti ShuklaNo ratings yet

- Wrigley AnalysisDocument140 pagesWrigley AnalysisBoonggy Boong25% (4)

- BUS 800 Supplemental Chapter F 2015, W 2016Document16 pagesBUS 800 Supplemental Chapter F 2015, W 2016Charlie XiangNo ratings yet

- Aig Best of Bernstein SlidesDocument50 pagesAig Best of Bernstein SlidesYA2301100% (1)

- Imp. InfoDocument2 pagesImp. InfoAnupam KumarNo ratings yet

- 2017 q3 Cef Investor LetterDocument6 pages2017 q3 Cef Investor LetterKini TinerNo ratings yet

- Due Diligence in 10 Easy StepsDocument4 pagesDue Diligence in 10 Easy StepsSameer ChalkeNo ratings yet

- CH 18Document40 pagesCH 18Louina YnciertoNo ratings yet

- Corsair Capital Q4 2011Document3 pagesCorsair Capital Q4 2011angadsawhneyNo ratings yet

- Basic To Understanding StocksDocument3 pagesBasic To Understanding StocksDavidNo ratings yet

- GuessDocument87 pagesGuessharsh1881100% (1)

- Aquilo Capital 1Q2011 Investor LetterDocument2 pagesAquilo Capital 1Q2011 Investor Letterblanche21No ratings yet

- Thesis Stock ValuationDocument4 pagesThesis Stock ValuationKarin Faust100% (2)

- Summary The Intelligent InvestorDocument6 pagesSummary The Intelligent InvestorDion GerriNo ratings yet

- Artko Capital 2016 Q2 LetterDocument8 pagesArtko Capital 2016 Q2 LetterSmitty WNo ratings yet

- Private Equity Research PapersDocument5 pagesPrivate Equity Research Papersc9rvz6mm100% (1)

- Financial Statements - IntroductionDocument75 pagesFinancial Statements - Introductiontopeq100% (6)

- Chapter 6 Prospective Analysis: ForecastingDocument10 pagesChapter 6 Prospective Analysis: ForecastingSheep ersNo ratings yet

- Financial Statements: Introduction: Printer Friendly Version (PDF Format)Document9 pagesFinancial Statements: Introduction: Printer Friendly Version (PDF Format)Rajveer SinghNo ratings yet

- Comparison of Five Popular StrategiesDocument12 pagesComparison of Five Popular StrategiesNam Dang ThanhNo ratings yet

- Market Notes May 3 TuesdayDocument2 pagesMarket Notes May 3 TuesdayJC CalaycayNo ratings yet

- SA Case StudyDocument6 pagesSA Case StudyKanika MaheshwariNo ratings yet

- Ambit Research Report Turnaround StocksDocument76 pagesAmbit Research Report Turnaround StocksArunddhuti RayNo ratings yet

- Calculate Self Sustainable Growth Rate (SSGR) of A CompanyDocument25 pagesCalculate Self Sustainable Growth Rate (SSGR) of A CompanymusiboyinaNo ratings yet

- Annexure Detailed Guideline On Project ReportDocument4 pagesAnnexure Detailed Guideline On Project Reportmohamed firdousNo ratings yet

- 3 Reasons You May Consider Selling Your Shares of CrowdStrike (NASDAQCRWD) Seeking AlphaDocument1 page3 Reasons You May Consider Selling Your Shares of CrowdStrike (NASDAQCRWD) Seeking Alphaygn728bn8rNo ratings yet

- Target-Date Series Research Paper 2013 Industry SurveyDocument6 pagesTarget-Date Series Research Paper 2013 Industry SurveyuylijwzndNo ratings yet

- Research Paper On Stock SplitDocument6 pagesResearch Paper On Stock Splitlyn0l1gamop2100% (1)

- Ambit Strategy Thematic Tomorrows Ten Baggers 19jan2012Document15 pagesAmbit Strategy Thematic Tomorrows Ten Baggers 19jan2012jainvivekNo ratings yet

- Paper CostcoDocument4 pagesPaper CostcoDhe SagalaNo ratings yet

- Greenlight Qlet2017 01Document5 pagesGreenlight Qlet2017 01Zerohedge100% (1)

- Greenhaven Road Capital Q1 2017Document12 pagesGreenhaven Road Capital Q1 2017superinvestorbulletiNo ratings yet

- What We Don'T Own: Greenhaven Road CapitalDocument11 pagesWhat We Don'T Own: Greenhaven Road Capitall chanNo ratings yet

- Artko Capital 2019 Q3 LetterDocument10 pagesArtko Capital 2019 Q3 LetterSmitty WNo ratings yet

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)From EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)No ratings yet

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)From EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)No ratings yet

- Stock Fundamental Analysis Mastery: Unlocking Company Stock Financials for Profitable TradingFrom EverandStock Fundamental Analysis Mastery: Unlocking Company Stock Financials for Profitable TradingNo ratings yet

- How to Make Money in Stocks: A Successful Strategy for Prosperous and Challenging TimesFrom EverandHow to Make Money in Stocks: A Successful Strategy for Prosperous and Challenging TimesNo ratings yet

- Performance of Private Equity-Backed IPOs. Evidence from the UK after the financial crisisFrom EverandPerformance of Private Equity-Backed IPOs. Evidence from the UK after the financial crisisNo ratings yet

- Ascendere Associates LLC Actionable Long/Short Equity ResearchDocument12 pagesAscendere Associates LLC Actionable Long/Short Equity ResearchStephen CastellanoNo ratings yet

- Financial Statement Model Example Stephen CastellanoDocument11 pagesFinancial Statement Model Example Stephen CastellanoStephen CastellanoNo ratings yet

- Income Statement Model - NuVasive, Inc. (NUVA)Document8 pagesIncome Statement Model - NuVasive, Inc. (NUVA)Stephen CastellanoNo ratings yet

- 27 Stocks For August 2015Document14 pages27 Stocks For August 2015Stephen CastellanoNo ratings yet

- 32 Stocks For May 2015Document11 pages32 Stocks For May 2015Stephen CastellanoNo ratings yet

- 23 Stocks For March 2015Document11 pages23 Stocks For March 2015Stephen CastellanoNo ratings yet

- 25 Stocks For July 2015Document11 pages25 Stocks For July 2015Stephen CastellanoNo ratings yet

- 25 Stocks For June 2015Document12 pages25 Stocks For June 2015Stephen CastellanoNo ratings yet

- Monthly 25 Stocks For October 2014Document10 pagesMonthly 25 Stocks For October 2014Stephen CastellanoNo ratings yet

- 26 Stocks For November 2014Document10 pages26 Stocks For November 2014Stephen CastellanoNo ratings yet

- Ascendere Associates LLC Innovative Long/Short Equity ResearchDocument10 pagesAscendere Associates LLC Innovative Long/Short Equity ResearchStephen CastellanoNo ratings yet

- The Best 25 Stocks For 2015Document13 pagesThe Best 25 Stocks For 2015Stephen CastellanoNo ratings yet

- Ascendere Associates LLC Innovative Long/Short Equity ResearchDocument10 pagesAscendere Associates LLC Innovative Long/Short Equity ResearchStephen CastellanoNo ratings yet

- Ascendere Associates LLC Innovative Long/Short Equity ResearchDocument10 pagesAscendere Associates LLC Innovative Long/Short Equity ResearchStephen CastellanoNo ratings yet

- Ascendere Price Targets For Feb 28, 2014 ModelDocument8 pagesAscendere Price Targets For Feb 28, 2014 ModelStephen CastellanoNo ratings yet

- 24 Stocks For March 2014Document12 pages24 Stocks For March 2014Stephen CastellanoNo ratings yet

- 24 Stocks For May 2014Document11 pages24 Stocks For May 2014Stephen CastellanoNo ratings yet

- Ascendere Associates LLC Innovative Long/Short Equity ResearchDocument10 pagesAscendere Associates LLC Innovative Long/Short Equity ResearchStephen CastellanoNo ratings yet

- 24 Stocks For June 2014Document10 pages24 Stocks For June 2014Stephen CastellanoNo ratings yet

- 27 GARP Stocks For April 2014Document11 pages27 GARP Stocks For April 2014Stephen CastellanoNo ratings yet

- Yahoo! Cash Flow and ROIC Analysis - September 9, 2011Document11 pagesYahoo! Cash Flow and ROIC Analysis - September 9, 2011Stephen CastellanoNo ratings yet

- 22 Stocks For February 2014Document13 pages22 Stocks For February 2014Stephen CastellanoNo ratings yet

- The Best 26 Stocks For 2014Document13 pagesThe Best 26 Stocks For 2014Stephen CastellanoNo ratings yet

- Westlake Chemical - Sell Off Based On Industry Peak Fears PrematureDocument9 pagesWestlake Chemical - Sell Off Based On Industry Peak Fears PrematureStephen CastellanoNo ratings yet

- The Best Bank Stocks in The KBW IndexDocument14 pagesThe Best Bank Stocks in The KBW IndexStephen CastellanoNo ratings yet

- Analyst Revision Trends - June 3, 2011Document18 pagesAnalyst Revision Trends - June 3, 2011Stephen CastellanoNo ratings yet

- Ascendere Daily Update - January 31, 2011 - Our Record of Presaging 45 Sell Side Upgrades With A 25-Stock Model Portfolio in January 2011Document17 pagesAscendere Daily Update - January 31, 2011 - Our Record of Presaging 45 Sell Side Upgrades With A 25-Stock Model Portfolio in January 2011Stephen CastellanoNo ratings yet

- Ascendere Daily Update - January 27, 2011 - Companies With Expanding ROIC Tend To Surprise To The UpsideDocument16 pagesAscendere Daily Update - January 27, 2011 - Companies With Expanding ROIC Tend To Surprise To The UpsideStephen CastellanoNo ratings yet

- SFP ACT 2021 Answer SheetDocument1 pageSFP ACT 2021 Answer SheetmoreNo ratings yet

- Module - 2 Informal Risk Capital & Venture CapitalDocument26 pagesModule - 2 Informal Risk Capital & Venture Capitalpvsagar2001No ratings yet

- Harris Kamala D. 2021 Annual 278Document15 pagesHarris Kamala D. 2021 Annual 278Daniel ChaitinNo ratings yet

- CapbudgetingproblemsDocument3 pagesCapbudgetingproblemsVishal PaithankarNo ratings yet

- Company LawDocument390 pagesCompany Lawchotu shahNo ratings yet

- The Study On Indian Financial System Post Liberalization: A Project Report Under The Guidance of MR - Satish KumarDocument106 pagesThe Study On Indian Financial System Post Liberalization: A Project Report Under The Guidance of MR - Satish Kumarnitinsood0% (1)

- Guide To Forex Price ActionDocument5 pagesGuide To Forex Price Action조선관 Tony ChoNo ratings yet

- Chapter 14 Marketing Planning Implementation and ControlDocument35 pagesChapter 14 Marketing Planning Implementation and ControlJENOVIC KAYEMBE MUSELENo ratings yet

- 2021 Saudi Arabia Venture Capital Report 2021Document25 pages2021 Saudi Arabia Venture Capital Report 2021Rania DirarNo ratings yet

- What Is Stock Market.-1Document25 pagesWhat Is Stock Market.-1Algo TraderNo ratings yet

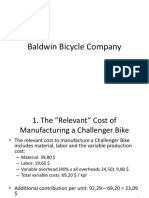

- Baldwin Bicycle Company EngDocument8 pagesBaldwin Bicycle Company EngChayan Kothari IDD,Biochem, IT-BHU, Varanasi (INDIA)No ratings yet

- Chap 7.MCQDocument7 pagesChap 7.MCQThanh Tung NgNo ratings yet

- Aarti Pandey ProjectDocument66 pagesAarti Pandey ProjectAmar Nath BabarNo ratings yet

- EmperadorIncPSEEMI PublicCompanyDocument1 pageEmperadorIncPSEEMI PublicCompanyLester FarewellNo ratings yet

- Principles of Marketing 15th Edition Kotler Test BankDocument46 pagesPrinciples of Marketing 15th Edition Kotler Test Bankpatricksenaxp0dw100% (28)

- Cash and Cash EquivalentsDocument3 pagesCash and Cash EquivalentsnikkitaaaNo ratings yet

- Pert. Ke 3. Analisa Kinerja KeuanganDocument25 pagesPert. Ke 3. Analisa Kinerja KeuanganYULIANTONo ratings yet

- Monopoly: Imba Nccu Managerial Economics Jack WuDocument26 pagesMonopoly: Imba Nccu Managerial Economics Jack WuMelina KurniawanNo ratings yet

- Ezz Steel Ratio Analysis - Fall21Document10 pagesEzz Steel Ratio Analysis - Fall21farahNo ratings yet

- Mastery in Business MathDocument2 pagesMastery in Business MathglaizacoseNo ratings yet

- Hull White PDFDocument64 pagesHull White PDFstehbar9570No ratings yet

- Partnership LiquidationDocument6 pagesPartnership LiquidationMonica MangobaNo ratings yet

- MJ 2021Document11 pagesMJ 2021Yusuf MohamedNo ratings yet

- Accn. Lockdown Worksheet 1Document3 pagesAccn. Lockdown Worksheet 1Wonder Bee NzamaNo ratings yet

- Chapter 2 Preparation of Financial Statements For Sole Traders SDocument6 pagesChapter 2 Preparation of Financial Statements For Sole Traders Skhoagoku147No ratings yet

- Murree Brewery: Beverage IndustryDocument12 pagesMurree Brewery: Beverage Industrykinza bashirNo ratings yet

- Introduction To The Money Market and The Roles Played by Governments and Security DealersDocument32 pagesIntroduction To The Money Market and The Roles Played by Governments and Security DealersAaqib MunirNo ratings yet

- 2011 Traders ManualDocument107 pages2011 Traders ManualPtg Futures100% (2)

- Financial Accounting Fundamentals: John J. Wild 2009 EditionDocument38 pagesFinancial Accounting Fundamentals: John J. Wild 2009 EditionMariamiNo ratings yet