You might also like

- Access to Finance: Microfinance Innovations in the People's Republic of ChinaFrom EverandAccess to Finance: Microfinance Innovations in the People's Republic of ChinaNo ratings yet

- Financial System in India and ChinaDocument12 pagesFinancial System in India and ChinaNavdeep KhokharNo ratings yet

- China Microfinance Industry Assessment ReportDocument72 pagesChina Microfinance Industry Assessment Reportapi-17447836No ratings yet

- Role of Commercial Bank in The Economic Development of INDIADocument5 pagesRole of Commercial Bank in The Economic Development of INDIAVaibhavRanjankar0% (1)

- Money and BankingDocument15 pagesMoney and BankingNaina SobtiNo ratings yet

- Banking LawDocument18 pagesBanking LawMunesh PandeyNo ratings yet

- Changing Scenario of Indian Banking SectorDocument14 pagesChanging Scenario of Indian Banking Sectorrupeshdahake8586100% (2)

- Chapter 1,2,3 PDFDocument36 pagesChapter 1,2,3 PDFprapoorna chintaNo ratings yet

- Pakistans PostReforms Banking SectorDocument5 pagesPakistans PostReforms Banking SectorAyeshaJangdaNo ratings yet

- Comparative Analysis of MSME Financial Institutions in Select CountriesDocument75 pagesComparative Analysis of MSME Financial Institutions in Select CountriesGogol SarinNo ratings yet

- Evolution of Indian Financial System: A Critical Review: Saraswathi Chandrashekhar DR Yogesh MaheshwariDocument12 pagesEvolution of Indian Financial System: A Critical Review: Saraswathi Chandrashekhar DR Yogesh Maheshwarividhyashekar93No ratings yet

- Financial InclusionDocument90 pagesFinancial InclusionRohan Mehra0% (1)

- Role of Commercial Banks in Economic Development: Indian PerspectiveDocument6 pagesRole of Commercial Banks in Economic Development: Indian PerspectivekapuNo ratings yet

- Banking in India - Reforms and Reorganization: Rajesh - Chakrabarti@mgt - Gatech.eduDocument27 pagesBanking in India - Reforms and Reorganization: Rajesh - Chakrabarti@mgt - Gatech.eduilusonaNo ratings yet

- Introduction and Design of The Study: NBFCS: A Historical BackgroundDocument51 pagesIntroduction and Design of The Study: NBFCS: A Historical BackgroundSWATHIKRISHNA RNo ratings yet

- The Impact of Deregulation On Commercial Banks and Their CustomersDocument14 pagesThe Impact of Deregulation On Commercial Banks and Their Customersshoaib_shebi6022No ratings yet

- Biased Lending and Non-Performing Loans in ChinasDocument24 pagesBiased Lending and Non-Performing Loans in ChinasmeronNo ratings yet

- Full Report On Al Barakah Islamic BankingDocument60 pagesFull Report On Al Barakah Islamic BankingDil NawazNo ratings yet

- Role of Financial Institutions in Economic Development of Pakistan Essay Sample - Papers and Articles On Bla Bla WritingDocument5 pagesRole of Financial Institutions in Economic Development of Pakistan Essay Sample - Papers and Articles On Bla Bla WritingMuhammad Shahid Saddique33% (3)

- Chapter 3 The Role of Financial Institutions in The Economic Development of Malawi: Commercial Banks PerspectiveDocument27 pagesChapter 3 The Role of Financial Institutions in The Economic Development of Malawi: Commercial Banks PerspectiveBasilio MaliwangaNo ratings yet

- Privatisation in BankDocument9 pagesPrivatisation in BankGaurav TripathiNo ratings yet

- Project Report 4th Sem 1Document51 pagesProject Report 4th Sem 1Neha SachdevaNo ratings yet

- Turnell On BankingReformInMyanmar-1Document17 pagesTurnell On BankingReformInMyanmar-1Su Wai MNo ratings yet

- Indian Banking: in Age of Hi-Tech EraDocument16 pagesIndian Banking: in Age of Hi-Tech Eraagrawal uditNo ratings yet

- Assessment of Corporate Governance Challenges Problems of MFIs in Ethiopia and The Way ForwardDocument28 pagesAssessment of Corporate Governance Challenges Problems of MFIs in Ethiopia and The Way ForwardhanyimwdmNo ratings yet

- College Magazine Latest KrishnanDocument6 pagesCollege Magazine Latest KrishnanChalil KrishnanNo ratings yet

- 03 - Review of LiteretureDocument7 pages03 - Review of LitereturePratham GadaNo ratings yet

- The Role of Regional Rural Banks (RRBS) in Financial Inclusion: An Empirical Study On West Bengal State in IndiaDocument12 pagesThe Role of Regional Rural Banks (RRBS) in Financial Inclusion: An Empirical Study On West Bengal State in IndiaKaran JainNo ratings yet

- Microfinance in VietnamDocument11 pagesMicrofinance in VietnamHoang Nang ThangNo ratings yet

- Group Assignment - Research FinalllyaDocument10 pagesGroup Assignment - Research FinalllyaMusurmonqul ChorievNo ratings yet

- Assignment On Role of Financial Institution: Rukmini Devi Institute OF Advanced StudiesDocument12 pagesAssignment On Role of Financial Institution: Rukmini Devi Institute OF Advanced StudiesHarshita ShekhawatNo ratings yet

- The Present and Future of China's New Rural Financial InstitutionsDocument4 pagesThe Present and Future of China's New Rural Financial InstitutionsaijbmNo ratings yet

- Performance and Financial Ratios of Commercial Banks in Malaysia and ChinaDocument12 pagesPerformance and Financial Ratios of Commercial Banks in Malaysia and Chinatedy hermawanNo ratings yet

- Chapter On Banking SectorDocument19 pagesChapter On Banking Sectorvikas jainNo ratings yet

- The Role of Financial Institutions in Long Run Economic GrowthDocument12 pagesThe Role of Financial Institutions in Long Run Economic GrowthPrateek GaurNo ratings yet

- Case 2 Uas IC COSO Bank ChinaDocument9 pagesCase 2 Uas IC COSO Bank ChinaAndreas NainggolanNo ratings yet

- Sustainability 10 01194 v2 PDFDocument20 pagesSustainability 10 01194 v2 PDFRajendra LamsalNo ratings yet

- Chinese Financial SystemDocument5 pagesChinese Financial Systemsanjana sureshNo ratings yet

- Role of Nationalised Banks in The EconomyDocument5 pagesRole of Nationalised Banks in The EconomyAshis karmakar100% (1)

- CHAPTER 1: Introduction: 1.1 Definition of BanksDocument99 pagesCHAPTER 1: Introduction: 1.1 Definition of BanksTushar KhandelwalNo ratings yet

- Banking Sector Reforms Lesson From PakistanDocument15 pagesBanking Sector Reforms Lesson From Pakistanzainahmedrajput224No ratings yet

- The Impact of Macro Factors On The Profitability of China's Commercial Banks in The Decade After WTO AccessionDocument6 pagesThe Impact of Macro Factors On The Profitability of China's Commercial Banks in The Decade After WTO AccessiondinandaNo ratings yet

- Institutii de Credit Articol 10Document10 pagesInstitutii de Credit Articol 10Liliana DNo ratings yet

- Banking SectorDocument8 pagesBanking SectorSupreet KaurNo ratings yet

- Banking Law NotesDocument49 pagesBanking Law NotesABINASH NRUSINGHANo ratings yet

- Term Paper On Development of Banking Sector in EthiopiaDocument13 pagesTerm Paper On Development of Banking Sector in EthiopiaSHALAMA DESTA TUSANo ratings yet

- Analysis of Growth Prospects of Non BankDocument7 pagesAnalysis of Growth Prospects of Non Bankmahesh toshniwalNo ratings yet

- Emmanuel Ngaga - ProposalDocument26 pagesEmmanuel Ngaga - Proposalhamzasadick99No ratings yet

- SMFISF270412 - Strengthening Governance in Micro Finance Institutions (MFIs) - Some Random ThoughtsDocument17 pagesSMFISF270412 - Strengthening Governance in Micro Finance Institutions (MFIs) - Some Random ThoughtsKhushboo KarnNo ratings yet

- A Study On Financial Statement Analysis of HDFCDocument63 pagesA Study On Financial Statement Analysis of HDFCKeleti SanthoshNo ratings yet

- A Review of Role and Challenges of Non-Banking Financial Companies in Economic Development of IndiaDocument9 pagesA Review of Role and Challenges of Non-Banking Financial Companies in Economic Development of IndiaSushm GiriNo ratings yet

- Fin 301Document6 pagesFin 301Mostafa ZubaerNo ratings yet

- Performance Appraisal of Urban Cooperative Banks: A Case StudyDocument15 pagesPerformance Appraisal of Urban Cooperative Banks: A Case StudyChethan KumarNo ratings yet

- Financial Inclusion in IndiaDocument7 pagesFinancial Inclusion in IndiaAsim MahatoNo ratings yet

- Role of Commercial Banks in Development Financing in BangladeshDocument31 pagesRole of Commercial Banks in Development Financing in Bangladeshfind4mohsinNo ratings yet

- Role of Finacial Institution in Industrial DevelopmentDocument56 pagesRole of Finacial Institution in Industrial DevelopmentTasmay EnterprisesNo ratings yet

- 15 - Chapter 6 PDFDocument30 pages15 - Chapter 6 PDFRukminiNo ratings yet

- 2WPSN140313Document29 pages2WPSN140313Rakesh BetiwarNo ratings yet

- Pratima Pudasaini Thesis of Credit Management 7 1Document67 pagesPratima Pudasaini Thesis of Credit Management 7 1Pradipta KafleNo ratings yet

- Ma 0027Document17 pagesMa 0027sathishNo ratings yet

- 10 International Conference On Problem and Possibilities in Online Education in ManagementDocument39 pages10 International Conference On Problem and Possibilities in Online Education in ManagementProf Dr Chowdari PrasadNo ratings yet

- Prof Chowdari Prasad CV 26112018Document11 pagesProf Chowdari Prasad CV 26112018Prof Dr Chowdari PrasadNo ratings yet

- A Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsDocument15 pagesA Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsProf Dr Chowdari PrasadNo ratings yet

- Second Innings September 2019Document52 pagesSecond Innings September 2019Prof Dr Chowdari PrasadNo ratings yet

- Performance of Crowd Funding in India: Issues and ChallengesDocument19 pagesPerformance of Crowd Funding in India: Issues and ChallengesProf Dr Chowdari Prasad100% (1)

- Consumer Protection Act 1986Document41 pagesConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- Digital Banking in India 2016Document21 pagesDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Recent Trends of PE Funding in IndiaDocument38 pagesRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadNo ratings yet

- Tapmi Update 2013Document120 pagesTapmi Update 2013Prof Dr Chowdari PrasadNo ratings yet

- HR As A Strategic Business PartnerDocument36 pagesHR As A Strategic Business PartnerProf Dr Chowdari PrasadNo ratings yet

- MFI National ConferenceDocument12 pagesMFI National ConferenceProf Dr Chowdari PrasadNo ratings yet

- Social Entrepreneurship2015Document45 pagesSocial Entrepreneurship2015Prof Dr Chowdari PrasadNo ratings yet

- Lean and Green Banking in India 2012Document20 pagesLean and Green Banking in India 2012Prof Dr Chowdari Prasad100% (2)

- Women Achievers Ebook2Document95 pagesWomen Achievers Ebook2Prof Dr Chowdari PrasadNo ratings yet

- Profile of Banks 2010-11Document99 pagesProfile of Banks 2010-11Vishesh KumarNo ratings yet

- Sibm, RBCBDocument20 pagesSibm, RBCBProf Dr Chowdari PrasadNo ratings yet

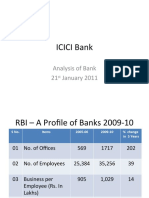

- Icici Bank: Analysis of Bank 21 January 2011Document6 pagesIcici Bank: Analysis of Bank 21 January 2011Prof Dr Chowdari PrasadNo ratings yet

- List of Books On Micro FinanceDocument32 pagesList of Books On Micro FinanceProf Dr Chowdari Prasad71% (7)

- Myths of Microfinance - Global South Development Magazine JAN 2011Document42 pagesMyths of Microfinance - Global South Development Magazine JAN 2011Silver Lining CreationNo ratings yet

- TAPMI ManipalDocument18 pagesTAPMI ManipalProf Dr Chowdari Prasad100% (1)

- Syndicate Institute of Bank Management, ManipalDocument67 pagesSyndicate Institute of Bank Management, ManipalProf Dr Chowdari PrasadNo ratings yet

- Remedial Law 2015-2018Document31 pagesRemedial Law 2015-2018FrancisNo ratings yet

- Activity Sheets: Quarter 2 - MELC 3Document11 pagesActivity Sheets: Quarter 2 - MELC 3John Zyrone Cayondong100% (1)

- Multifamily ResearchDocument4 pagesMultifamily ResearchNephenteNo ratings yet

- Cash and ReceivablesDocument6 pagesCash and ReceivablesNylan AnyerNo ratings yet

- CFADS Calculation & Application PDFDocument2 pagesCFADS Calculation & Application PDFJORGE PUENTESNo ratings yet

- Prudential Regulations For Microfinance BanksDocument40 pagesPrudential Regulations For Microfinance BanksSajid Ali MaariNo ratings yet

- The Great Debt Transformation Households Financialization and Policy ResponsesDocument305 pagesThe Great Debt Transformation Households Financialization and Policy ResponsesSam SamNo ratings yet

- Hire PurchaseDocument14 pagesHire Purchasesouvik.icfai50% (4)

- Retail Banking DR M PrasadaraoDocument11 pagesRetail Banking DR M PrasadaraoDr. M.Prasada RaoNo ratings yet

- Full 2014 2015 PDFDocument282 pagesFull 2014 2015 PDFFarjana Hossain DharaNo ratings yet

- Kimatu - Determinants of Loan Defaults in Saccos in Kenya - A Case of Metropolitan National Sacco LTD in KenyaDocument55 pagesKimatu - Determinants of Loan Defaults in Saccos in Kenya - A Case of Metropolitan National Sacco LTD in KenyaFahad SalumNo ratings yet

- Stone Mountain Capital Partners DDQDocument30 pagesStone Mountain Capital Partners DDQapi-276349208No ratings yet

- Branch Manager or Loan Analyst or VP of Lending or Loan ManagerDocument5 pagesBranch Manager or Loan Analyst or VP of Lending or Loan Managerapi-121643461No ratings yet

- CPF - Form For RPS Funding and GuidelinesDocument9 pagesCPF - Form For RPS Funding and Guidelinesapi-3803117No ratings yet

- Basel III and Its Implications On Banking SectorDocument56 pagesBasel III and Its Implications On Banking Sectoradityavikram009No ratings yet

- Loan PricingDocument39 pagesLoan PricingBhagath GottipatiNo ratings yet

- Debt CollectionDocument2 pagesDebt CollectionramNo ratings yet

- Math Solution - Session 11Document8 pagesMath Solution - Session 11Saoda Feel IslamNo ratings yet

- TransportationDocument4 pagesTransportationYuni ArdiyantiNo ratings yet

- Annual Report PPFDocument71 pagesAnnual Report PPFBhuvanesh Narayana SamyNo ratings yet

- Senior Vice President Lending in Dallas FT Worth TX Resume Kenneth OpieDocument2 pagesSenior Vice President Lending in Dallas FT Worth TX Resume Kenneth OpieKennethOpieNo ratings yet

- PT Bank HSBC Indonesia Annual Report 2020Document357 pagesPT Bank HSBC Indonesia Annual Report 2020Salsabila MaharaniNo ratings yet

- The Times - June.17.2023Document96 pagesThe Times - June.17.2023daniel leivaNo ratings yet

- CMPCir1656 12Document95 pagesCMPCir1656 12sunilNo ratings yet

- Auto Loan Data Completion Sheet 11.5.19Document9 pagesAuto Loan Data Completion Sheet 11.5.19Maria AlvarezNo ratings yet

- Investment Law For ReportersDocument19 pagesInvestment Law For ReportersJessica BernardoNo ratings yet

- Balloon Loan Calculator: InputsDocument9 pagesBalloon Loan Calculator: Inputsmy.nafi.pmp5283No ratings yet

- EMIS Insights - Mexico Consumer Goods and Retail Sector Report 2019 - 2020Document75 pagesEMIS Insights - Mexico Consumer Goods and Retail Sector Report 2019 - 2020Pily CorroNo ratings yet

- Itlog Ni JanDocument10 pagesItlog Ni JanAlejandro Javellana Paras IVNo ratings yet

- Banking 101 - Large Cap Bank Primer - Deutsche Bank (2011) PDFDocument112 pagesBanking 101 - Large Cap Bank Primer - Deutsche Bank (2011) PDFJcove100% (2)