You might also like

- Leading Your HOA: A 1-Hour Guide to Being a Successful HOA Board MemberFrom EverandLeading Your HOA: A 1-Hour Guide to Being a Successful HOA Board MemberNo ratings yet

- A Self Help Group Approach and Community Organization in a Rural VillageFrom EverandA Self Help Group Approach and Community Organization in a Rural VillageNo ratings yet

- Self Help Groups: BY N.Manoj KumarDocument14 pagesSelf Help Groups: BY N.Manoj KumarManoj Kumar NNo ratings yet

- Microfinance in NepalDocument13 pagesMicrofinance in NepalGyan PokhrelNo ratings yet

- SHG & JLGDocument5 pagesSHG & JLGManasi PatilNo ratings yet

- VillageAction Micro Finance ProfileDocument11 pagesVillageAction Micro Finance ProfileAuroville Village Action GroupNo ratings yet

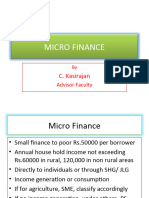

- Micro FinanceDocument34 pagesMicro FinanceABDUL KALAMNo ratings yet

- Self Help GroupDocument32 pagesSelf Help GroupRishi KeshavNo ratings yet

- SHGs in India Mbfi Unit 2Document32 pagesSHGs in India Mbfi Unit 2Yenkee Adarsh AroraNo ratings yet

- Microfinance Management: Chapter - 3 Self-Help Groups: Institution Building, OperationsDocument16 pagesMicrofinance Management: Chapter - 3 Self-Help Groups: Institution Building, Operationssunit dasNo ratings yet

- Self Help Group Upsc Notes 14Document5 pagesSelf Help Group Upsc Notes 14Ajay RohithNo ratings yet

- Self Help GroupDocument28 pagesSelf Help Groupvanithajeyasankar100% (3)

- Shg's in IndiaDocument1 pageShg's in IndiaSanjay NegiNo ratings yet

- SHG Detail PunjabDocument60 pagesSHG Detail Punjabgoldy2soni2003No ratings yet

- Economics Project - Arpit JainDocument24 pagesEconomics Project - Arpit Jainarpit100% (1)

- VSL - Introduction and OverviewDocument23 pagesVSL - Introduction and OverviewPeddie BaclagonNo ratings yet

- Micro Finance SHG PPT 120928142952 Phpapp01Document30 pagesMicro Finance SHG PPT 120928142952 Phpapp01karanjangid17No ratings yet

- SHG Profiles and Study AreaDocument29 pagesSHG Profiles and Study AreaRavi ShankarNo ratings yet

- Sarvodaya Nano FinanceDocument33 pagesSarvodaya Nano FinanceRahul RenceNo ratings yet

- Commerce Class G11 Topic - Cooperative Society Grade - G11 Subject - Commerce Week - 5 Cooperative SocietyDocument7 pagesCommerce Class G11 Topic - Cooperative Society Grade - G11 Subject - Commerce Week - 5 Cooperative SocietyAdeola YusufNo ratings yet

- MF Module 4Document23 pagesMF Module 4Rekha MadhuNo ratings yet

- Presentation On Self Help Groups - RPADocument13 pagesPresentation On Self Help Groups - RPAAnshulUpadhyayNo ratings yet

- Introduction To Table Banking PDFDocument14 pagesIntroduction To Table Banking PDFlittlebluefountains100% (5)

- Micro Finance LastDocument30 pagesMicro Finance Lastnishantbali100% (11)

- Sterling Institute of Management StudiesDocument12 pagesSterling Institute of Management StudieskristokunsNo ratings yet

- Self Help GroupsDocument34 pagesSelf Help GroupsManashvi karthikeyanNo ratings yet

- Financial Products and ServicesDocument41 pagesFinancial Products and ServicesMohammed AslamNo ratings yet

- SHG ConceptDocument12 pagesSHG ConceptShishir KumarNo ratings yet

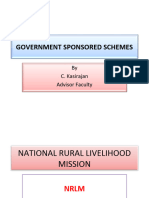

- NRLMDocument64 pagesNRLMABDUL KALAMNo ratings yet

- 01f7e13. Rating and Grading PDFDocument11 pages01f7e13. Rating and Grading PDFTushar RajpalNo ratings yet

- AccountsDocument9 pagesAccountssuheb100% (2)

- Detail-Self Help Group ProgrammeDocument5 pagesDetail-Self Help Group ProgrammeSuresh MuruganNo ratings yet

- Micro FInancingDocument54 pagesMicro FInancingShivam SachdevaNo ratings yet

- Unit 2 MFRBDocument31 pagesUnit 2 MFRBSweety TuladharNo ratings yet

- Self Help Groups (SHGS)Document24 pagesSelf Help Groups (SHGS)abhinavjogNo ratings yet

- Levwa - Micro FinanceDocument12 pagesLevwa - Micro FinanceGowri J BabuNo ratings yet

- Microfinance & Pandyan Grama Bank ModelDocument20 pagesMicrofinance & Pandyan Grama Bank ModelParitosh AnandNo ratings yet

- Self Help Groups: Women EmpowermentDocument12 pagesSelf Help Groups: Women EmpowermentArun Kumar SinghNo ratings yet

- Unit 4: Self Help Groups and Micro FinanceDocument15 pagesUnit 4: Self Help Groups and Micro Financeknsvel2000No ratings yet

- SHG ProjectDocument26 pagesSHG ProjectShreyaaNo ratings yet

- Self Help Group: Abhishek Kumar Ranjan Mentor: Dr. Sandeep Singh MBA MBA2210006Document9 pagesSelf Help Group: Abhishek Kumar Ranjan Mentor: Dr. Sandeep Singh MBA MBA2210006Utsav JaiswalNo ratings yet

- Women Saving Scheme (Self Help Group)Document17 pagesWomen Saving Scheme (Self Help Group)Revathi RamaswamiNo ratings yet

- Main Project of SHGDocument27 pagesMain Project of SHGMinal DalviNo ratings yet

- Micro Finance SHG PPT 120928142952 Phpapp01Document30 pagesMicro Finance SHG PPT 120928142952 Phpapp01Aaryan Singh100% (2)

- Group Work in Different SettingsDocument109 pagesGroup Work in Different Settingsakshar pandavNo ratings yet

- Shri Siddheshwar Co-Operative BankDocument11 pagesShri Siddheshwar Co-Operative BankPrabhu Mandewali50% (2)

- 001 HUD COOPERATIVE PMES PresentationDocument26 pages001 HUD COOPERATIVE PMES PresentationJane NuwrhayyahNo ratings yet

- MicrofinanceDocument27 pagesMicrofinancevchouha9993No ratings yet

- Ch3. Money and CreditDocument30 pagesCh3. Money and CreditGarima GoelNo ratings yet

- Rural and Women EnterpreneurshipDocument60 pagesRural and Women Enterpreneurshipgurudarshan100% (1)

- Self Help Group ThesisDocument6 pagesSelf Help Group Thesistiffanymillerlittlerock100% (2)

- Banking and Finance AnswersDocument6 pagesBanking and Finance AnswersStan leeNo ratings yet

- SHG 3Document12 pagesSHG 3PjNo ratings yet

- Sec Notes-15 Rural Development Sem-3Document6 pagesSec Notes-15 Rural Development Sem-3JimmyNo ratings yet

- The Scope of Micro Finance in Rural AreaDocument23 pagesThe Scope of Micro Finance in Rural AreavirugargNo ratings yet

- Management of Self Help Groups LAVSDocument11 pagesManagement of Self Help Groups LAVSBiplab PandaNo ratings yet

- MyDocument19 pagesMyUmesh BachhavNo ratings yet

- MC 2017-02 Prs For New Registering CooperativesDocument122 pagesMC 2017-02 Prs For New Registering CooperativesnonoyjaymeNo ratings yet

- Co Operatives MGMTDocument15 pagesCo Operatives MGMTAbhishek ShettyNo ratings yet

- Micro Finance PPT FinalDocument37 pagesMicro Finance PPT FinalVaibhav Alawa100% (2)

- Maternity Benefit ActDocument1 pageMaternity Benefit ActDHAVAL PATELNo ratings yet

- A Credit CrisisDocument1 pageA Credit CrisisDHAVAL PATELNo ratings yet

- Different Courses in EngineeringDocument11 pagesDifferent Courses in EngineeringDHAVAL PATELNo ratings yet

- Marketing Your Business: A Web Quest Designed byDocument14 pagesMarketing Your Business: A Web Quest Designed byDHAVAL PATELNo ratings yet

- 100 Keyboard ShortcutsDocument7 pages100 Keyboard ShortcutsDHAVAL PATELNo ratings yet

- Euro Debt-1Document7 pagesEuro Debt-1DHAVAL PATELNo ratings yet

- 10 10 How Useful Are Your Questionnaires Revised 03Document17 pages10 10 How Useful Are Your Questionnaires Revised 03DHAVAL PATELNo ratings yet

- SHG FederationsDocument11 pagesSHG FederationsDHAVAL PATELNo ratings yet

- CAT FAQsDocument6 pagesCAT FAQsDHAVAL PATELNo ratings yet

- Euro DebtDocument18 pagesEuro DebtDHAVAL PATELNo ratings yet

- ApsrtcDocument1 pageApsrtcDHAVAL PATELNo ratings yet

- A Project On Study of Housing FinanceDocument9 pagesA Project On Study of Housing FinanceDHAVAL PATELNo ratings yet