You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Introduction to Networks Visual GuideDocument1 pageIntroduction to Networks Visual GuideWorldNo ratings yet

- NDA Template Non Disclosure Non Circumvent No Company NameDocument9 pagesNDA Template Non Disclosure Non Circumvent No Company NamepvorsterNo ratings yet

- Total Product Marketing Procedures: A Case Study On "BSRM Xtreme 500W"Document75 pagesTotal Product Marketing Procedures: A Case Study On "BSRM Xtreme 500W"Yasir Alam100% (1)

- DepEd K to 12 Awards PolicyDocument29 pagesDepEd K to 12 Awards PolicyAstraea Knight100% (1)

- TAFC R10 SP54 Release NotesDocument10 pagesTAFC R10 SP54 Release NotesBejace NyachhyonNo ratings yet

- TDS Tetrapur 100 (12-05-2014) enDocument2 pagesTDS Tetrapur 100 (12-05-2014) enCosmin MușatNo ratings yet

- Soap - WikipediaDocument57 pagesSoap - Wikipediayash BansalNo ratings yet

- Sky Education: Organisation of Commerce and ManagementDocument12 pagesSky Education: Organisation of Commerce and ManagementKiyaara RathoreNo ratings yet

- FE 405 Ps 3 AnsDocument12 pagesFE 405 Ps 3 Anskannanv93No ratings yet

- (Section-A / Aip) : Delhi Public School GandhinagarDocument2 pages(Section-A / Aip) : Delhi Public School GandhinagarVvs SadanNo ratings yet

- Monson, Concilio Di TrentoDocument38 pagesMonson, Concilio Di TrentoFrancesca Muller100% (1)

- Booklet - CopyxDocument20 pagesBooklet - CopyxHåkon HallenbergNo ratings yet

- Blood Culture & Sensitivity (2011734)Document11 pagesBlood Culture & Sensitivity (2011734)Najib AimanNo ratings yet

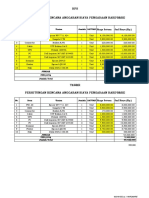

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANDocument2 pagesHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriNo ratings yet

- SPACES Nepal - Green Schools Building The FutureDocument3 pagesSPACES Nepal - Green Schools Building The FutureBimal ThapaNo ratings yet

- Protein Synthesis: Class Notes NotesDocument2 pagesProtein Synthesis: Class Notes NotesDale HardingNo ratings yet

- Prof Ed 7 ICT Policies and Issues Implications To Teaching and LearningDocument11 pagesProf Ed 7 ICT Policies and Issues Implications To Teaching and Learnings.angelicamoradaNo ratings yet

- Commercial Contractor Exam Study GuideDocument7 pagesCommercial Contractor Exam Study Guidejclark13010No ratings yet

- Saic P 3311Document7 pagesSaic P 3311Arshad ImamNo ratings yet

- Garner Fructis ShampooDocument3 pagesGarner Fructis Shampooyogesh0794No ratings yet

- BAFINAR - Midterm Draft (R) PDFDocument11 pagesBAFINAR - Midterm Draft (R) PDFHazel Iris Caguingin100% (1)

- Basic Principles of Social Stratification - Sociology 11 - A SY 2009-10Document9 pagesBasic Principles of Social Stratification - Sociology 11 - A SY 2009-10Ryan Shimojima67% (3)

- Texas COVID-19 Vaccine Distribution PlanDocument38 pagesTexas COVID-19 Vaccine Distribution PlandmnpoliticsNo ratings yet

- Effectiveness of Laundry Detergents and Bars in Removing Common StainsDocument9 pagesEffectiveness of Laundry Detergents and Bars in Removing Common StainsCloudy ClaudNo ratings yet

- Test Bank For Understanding Pathophysiology 4th Edition Sue e HuetherDocument36 pagesTest Bank For Understanding Pathophysiology 4th Edition Sue e Huethercarotin.shallowupearp100% (41)

- 2020052336Document4 pages2020052336Kapil GurunathNo ratings yet

- Christian Mission and Conversion. Glimpses About Conversion, Constitution, Right To ReligionDocument8 pagesChristian Mission and Conversion. Glimpses About Conversion, Constitution, Right To ReligionSudheer Siripurapu100% (1)

- Republic vs. Maria Lee and IAC, G.R. No. 64818, May 13, 1991 (197 SCRA)Document1 pageRepublic vs. Maria Lee and IAC, G.R. No. 64818, May 13, 1991 (197 SCRA)PatNo ratings yet

- Qatar Star Network - As of April 30, 2019Document7 pagesQatar Star Network - As of April 30, 2019Gends DavoNo ratings yet

- EDMOTO 4th TopicDocument24 pagesEDMOTO 4th TopicAngel Delos SantosNo ratings yet