You might also like

- India - RBI Mobile Banking Guidelines - 20081010 Via Medianama - ComDocument7 pagesIndia - RBI Mobile Banking Guidelines - 20081010 Via Medianama - Commixedbag100% (3)

- Project Report On Mobile BankingDocument45 pagesProject Report On Mobile BankingTulika Agrawal Rawool57% (7)

- Guidelines On Mobile Financial ServicesDocument4 pagesGuidelines On Mobile Financial ServicesAhsan ZamanNo ratings yet

- BRANCHLESS BANKING OVERVIEWDocument45 pagesBRANCHLESS BANKING OVERVIEWZab JaanNo ratings yet

- Indian Banking Industry-Customer Satisfaction & PreferencesDocument12 pagesIndian Banking Industry-Customer Satisfaction & PreferencesakankaroraNo ratings yet

- How RBI Is Changing Trends in M-PaymentDocument14 pagesHow RBI Is Changing Trends in M-PaymentVikash GopalanNo ratings yet

- Bnkingc CaseDocument5 pagesBnkingc CaseDishant PatelNo ratings yet

- Bangladesh Bank Guidelines On Mobile BankingDocument11 pagesBangladesh Bank Guidelines On Mobile BankingIshtiaq Oni RahmanNo ratings yet

- Annex - IDocument9 pagesAnnex - IRicha RaghuvanshiNo ratings yet

- E-Banking Services of RbiDocument14 pagesE-Banking Services of RbiSrinivasan SrinivasanNo ratings yet

- Mobile Banking PolicyDocument12 pagesMobile Banking PolicySuraj GCNo ratings yet

- INTERNET BANKING SawarnimDocument12 pagesINTERNET BANKING SawarnimSwarnim RamolaNo ratings yet

- XIM Bhubaneswar Commercial Banking Group Potential of M-BankingDocument27 pagesXIM Bhubaneswar Commercial Banking Group Potential of M-BankingNeetesh SinghNo ratings yet

- Role of It in BankingDocument5 pagesRole of It in BankingSamaira SheikhNo ratings yet

- Importance of Branchless Banking & Moblle Banking in PakistanDocument24 pagesImportance of Branchless Banking & Moblle Banking in PakistanDaniyal NasirNo ratings yet

- Emergence of Doorstep BankingDocument62 pagesEmergence of Doorstep BankingAkshay TambeNo ratings yet

- Project On IMPS (Immediate Payment Service)Document46 pagesProject On IMPS (Immediate Payment Service)Nayeem100% (1)

- Complete Guide to Banking Awareness & General KnowledgeDocument467 pagesComplete Guide to Banking Awareness & General KnowledgeSivaji Haldar50% (2)

- 12 03 29 RBI Paper On MBankingDocument9 pages12 03 29 RBI Paper On MBankingvivekanandsNo ratings yet

- RECENT DEVELOPMENTS IN INDIA'S BANKING SECTORDocument20 pagesRECENT DEVELOPMENTS IN INDIA'S BANKING SECTORSatyajit SahooNo ratings yet

- Convergence of Mobile Banking, Financial Inclusion and Consumer Protection-TrendDocument3 pagesConvergence of Mobile Banking, Financial Inclusion and Consumer Protection-TrendCiocoiu Vlad AndreiNo ratings yet

- Ijrar Issue 20543089Document3 pagesIjrar Issue 20543089Muruga.v maddyNo ratings yet

- Banking Structure and Functions in IndiaDocument39 pagesBanking Structure and Functions in IndianidahassainNo ratings yet

- Chapter-8 Summary of Findings, Conclusion and SuggestionsDocument28 pagesChapter-8 Summary of Findings, Conclusion and SuggestionsJCMMPROJECTNo ratings yet

- Airtel Payments Bank Launches with 7.25% Interest on SavingsDocument40 pagesAirtel Payments Bank Launches with 7.25% Interest on SavingsPrabhaNo ratings yet

- Rise of Core Banking in IndiaDocument4 pagesRise of Core Banking in IndiaShambhavi SinghNo ratings yet

- Mobile BankingDocument54 pagesMobile BankingUjwal JaiswalNo ratings yet

- Core Banking ProjectDocument25 pagesCore Banking ProjectKamlesh Negi55% (11)

- Role of It in BankingDocument4 pagesRole of It in BankingKisha NelsonNo ratings yet

- RBI DIgital Banking UnitsDocument7 pagesRBI DIgital Banking UnitsAmrish Trivedi100% (1)

- Interlink Branch Banking: Banking & Insurance Prepared By: Pratik ShrimaliDocument18 pagesInterlink Branch Banking: Banking & Insurance Prepared By: Pratik ShrimaliPratik ShrimaliNo ratings yet

- Rbi-Guidelines - Prepaid-Payments-Medianama - ComDocument7 pagesRbi-Guidelines - Prepaid-Payments-Medianama - Commixedbag100% (2)

- Final Guidelines For Payment BanksDocument3 pagesFinal Guidelines For Payment BanksAnkaj MohindrooNo ratings yet

- M-Banking in India - Regulations and Rationale : K. C. ChakrabartyDocument4 pagesM-Banking in India - Regulations and Rationale : K. C. ChakrabartyeexploreerNo ratings yet

- Branch Less BankingDocument48 pagesBranch Less Bankingsyedasiftanveer100% (2)

- The Banking Ombudsman Scheme: Annual Report 2006-2007Document63 pagesThe Banking Ombudsman Scheme: Annual Report 2006-2007Deepesh AgrawalNo ratings yet

- Project Report On e BankingDocument88 pagesProject Report On e BankingDhirender Chauhan80% (10)

- SBI Traning ReportDocument66 pagesSBI Traning ReportAmardeep SinghNo ratings yet

- Current Scenario in IndiaDocument24 pagesCurrent Scenario in IndiaMeenuNo ratings yet

- Mobile Banking: A Tool For Financial Inclusion: K. Meena KumariDocument8 pagesMobile Banking: A Tool For Financial Inclusion: K. Meena KumariTJPRC PublicationsNo ratings yet

- Bank of IndiaDocument94 pagesBank of IndiaOm Prakash Singh100% (2)

- Important RationalsDocument37 pagesImportant RationalsSalil JoshiNo ratings yet

- Guidelines on Agent BankingDocument7 pagesGuidelines on Agent BankingEEL KfWBMZ2.1No ratings yet

- Frequently Asked Questions Frequently Asked Questions Frequently Asked QuestionsDocument9 pagesFrequently Asked Questions Frequently Asked Questions Frequently Asked QuestionsPavan Kalyan J PspkNo ratings yet

- Chapter 12 Audit of BanksDocument42 pagesChapter 12 Audit of Bankshamza hamzaNo ratings yet

- Mobile Banking and Customer SatisfactionDocument8 pagesMobile Banking and Customer SatisfactionVDC CommerceNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaFrom EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaNo ratings yet

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceFrom EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinanceRating: 4 out of 5 stars4/5 (9)

- Managing the Development of Digital Marketplaces in AsiaFrom EverandManaging the Development of Digital Marketplaces in AsiaNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Road Map for Developing an Online Platform to Trade Nonperforming Loans in Asia and the PacificFrom EverandRoad Map for Developing an Online Platform to Trade Nonperforming Loans in Asia and the PacificNo ratings yet

- Bank Fundamentals: An Introduction to the World of Finance and BankingFrom EverandBank Fundamentals: An Introduction to the World of Finance and BankingRating: 4.5 out of 5 stars4.5/5 (4)

- Asia Small and Medium-Sized Enterprise Monitor 2021 Volume III: Digitalizing Microfinance in Bangladesh: Findings from the Baseline SurveyFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2021 Volume III: Digitalizing Microfinance in Bangladesh: Findings from the Baseline SurveyNo ratings yet

- Financial Digitalization and Its Implications for ASEAN+3 Regional Financial StabilityFrom EverandFinancial Digitalization and Its Implications for ASEAN+3 Regional Financial StabilityNo ratings yet

- IAMAI - Pre Budget MemorandumDocument21 pagesIAMAI - Pre Budget MemorandummixedbagNo ratings yet

- q209 OnMobile Global Consolidated ResultsDocument2 pagesq209 OnMobile Global Consolidated ResultsmixedbagNo ratings yet

- India 3g Auctions Notice Inviting Applications 2010 25 10 MedianamaDocument113 pagesIndia 3g Auctions Notice Inviting Applications 2010 25 10 MedianamamixedbagNo ratings yet

- India 3g Auctions Q&a 2010 25 10 MedianamaDocument98 pagesIndia 3g Auctions Q&a 2010 25 10 MedianamamixedbagNo ratings yet

- q209 OnMobile Global Standalone ResultsDocument2 pagesq209 OnMobile Global Standalone ResultsmixedbagNo ratings yet

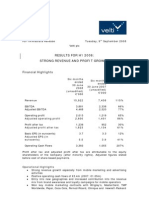

- Results For H1 2008: Strong Revenue and Profit Growth: Financial HighlightsDocument18 pagesResults For H1 2008: Strong Revenue and Profit Growth: Financial HighlightsmixedbagNo ratings yet

- Q3 2009 UTV Software Communications Financials Uploaded by MediaNamaDocument1 pageQ3 2009 UTV Software Communications Financials Uploaded by MediaNamamixedbagNo ratings yet

- Doordarshan MobileTV Tender MediaNamaDocument39 pagesDoordarshan MobileTV Tender MediaNamamixedbag100% (5)

- UTV Software Communications LimitedDocument13 pagesUTV Software Communications LimitedmixedbagNo ratings yet

- Rbi-Guidelines - Prepaid-Payments-Medianama - ComDocument7 pagesRbi-Guidelines - Prepaid-Payments-Medianama - Commixedbag100% (2)

- GSM Monthly Oct08 Medianama - ComDocument9 pagesGSM Monthly Oct08 Medianama - Commixedbag100% (1)

- Q209 Reliance Communications Quarterly ReportDocument36 pagesQ209 Reliance Communications Quarterly Reportmixedbag100% (4)

- Tel No:-011-2321 7914 Fax: - 011-2321 1998 Email: - Skgupta@trai - Gov.in WebsiteDocument5 pagesTel No:-011-2321 7914 Fax: - 011-2321 1998 Email: - Skgupta@trai - Gov.in Websitemixedbag100% (1)

- 2008 - Music Sales Data 2006-2010 - Final (India)Document1 page2008 - Music Sales Data 2006-2010 - Final (India)mixedbag100% (1)

- 2009 q2 Financials RediffDocument1 page2009 q2 Financials RediffmixedbagNo ratings yet

- q1 09 IOL Netcom ResultsDocument1 pageq1 09 IOL Netcom ResultsmixedbagNo ratings yet

- Utv Financials 2qfy2009Document1 pageUtv Financials 2qfy2009mixedbagNo ratings yet

- Northgate Financials 2009q2Document2 pagesNorthgate Financials 2009q2mixedbagNo ratings yet

- Web18-Q2-2008-09 FinancialsDocument14 pagesWeb18-Q2-2008-09 Financialsmixedbag100% (1)

- Utv Earnings Release 2qfy2009Document9 pagesUtv Earnings Release 2qfy2009mixedbagNo ratings yet

- q209 - Airtel Published FinancialsDocument7 pagesq209 - Airtel Published Financialsmixedbag100% (2)

- q209 - Airtel Quarterly ReportDocument45 pagesq209 - Airtel Quarterly Reportmixedbag100% (1)

- q209 - Airtel Press - ReleaseDocument2 pagesq209 - Airtel Press - ReleasemixedbagNo ratings yet

- Annual Report - 2007-08 Info EdgeDocument121 pagesAnnual Report - 2007-08 Info EdgemixedbagNo ratings yet

- 2009-10-24 Info Edge q2 FinancialsDocument1 page2009-10-24 Info Edge q2 FinancialsmixedbagNo ratings yet

- Annual Report - 2007-08 Info EdgeDocument121 pagesAnnual Report - 2007-08 Info EdgemixedbagNo ratings yet

- Geodesic Shows Robust Growth in The Second QuarterDocument3 pagesGeodesic Shows Robust Growth in The Second QuartermixedbagNo ratings yet

- q2 ResultsDocument2 pagesq2 ResultsmixedbagNo ratings yet

- q2 Consol ResultsDocument2 pagesq2 Consol ResultsmixedbagNo ratings yet

- HTMedia Q209ResultsDocument10 pagesHTMedia Q209Resultsmixedbag100% (1)

- An Overview of Block-Chain Technology and Related Security Attacks: Systematic Literature ReviewDocument15 pagesAn Overview of Block-Chain Technology and Related Security Attacks: Systematic Literature Reviewindex PubNo ratings yet

- Cyber SecurityDocument6 pagesCyber SecuritySugam GiriNo ratings yet

- Sec Brksec-3540 PDFDocument94 pagesSec Brksec-3540 PDFSayaOtanashiNo ratings yet

- Interscan Messaging Security Virtual Appliance: Installation GuideDocument152 pagesInterscan Messaging Security Virtual Appliance: Installation GuideeunaotoakiNo ratings yet

- Eaton Certificate PolicyDocument33 pagesEaton Certificate PolicyAl MullenNo ratings yet

- ISO27k Standards Listing PDFDocument7 pagesISO27k Standards Listing PDFZulkkanNo ratings yet

- Ny - NR Nodes KpiDocument11 pagesNy - NR Nodes KpiSudeep KumarNo ratings yet

- MktLit AX-S4-ICCP 082014Document2 pagesMktLit AX-S4-ICCP 082014davidNo ratings yet

- A Comparison Between Encryption and Decryption'Document15 pagesA Comparison Between Encryption and Decryption'2010roomiNo ratings yet

- Key Cyber Resiliency Terms and ConceptsDocument3 pagesKey Cyber Resiliency Terms and ConceptsCharleston FernandesNo ratings yet

- Blockchain Lecture Notes November 12, 2022Document2 pagesBlockchain Lecture Notes November 12, 2022aiza eroyNo ratings yet

- CCNA Security 210-260Document2 pagesCCNA Security 210-260Chris BuenaventuraNo ratings yet

- v1 Script HTML Facebook DirectDocument1 pagev1 Script HTML Facebook DirectIwan IwanNo ratings yet

- Ais615 July 22Document11 pagesAis615 July 22Yusuf WaldanNo ratings yet

- Leni Andriani - 1.0.1.2 Class Activity - Top Hacker Shows Us How It Is DoneDocument2 pagesLeni Andriani - 1.0.1.2 Class Activity - Top Hacker Shows Us How It Is DoneLeni AndrianiNo ratings yet

- Information Assurance - Defined and ExplainedDocument3 pagesInformation Assurance - Defined and ExplainedHarris AliNo ratings yet

- MSCIS Project (Aniruddh Sharma-MSEP-038) - 2107702623Document103 pagesMSCIS Project (Aniruddh Sharma-MSEP-038) - 2107702623Aniruddh SharmaNo ratings yet

- A Nest For Cyber Criminals The Dark WebDocument5 pagesA Nest For Cyber Criminals The Dark WebGuru Ke Singh100% (1)

- Steps - eAccReg EnrollmentDocument9 pagesSteps - eAccReg EnrollmentEloisa Moaje AtienzaNo ratings yet

- Antony Kungu - Final Project AssignmentDocument11 pagesAntony Kungu - Final Project Assignmentapi-420816837No ratings yet

- Security Best Practices For Postgresql: WhitepaperDocument14 pagesSecurity Best Practices For Postgresql: WhitepaperLUIS FERNANDO MEJÍA TORRESNo ratings yet

- Tafjmessage IntegrityDocument22 pagesTafjmessage IntegrityNghiêm TuấnNo ratings yet

- Nitin Yadav: Brain, Mind and Markets Lab The University of MelbourneDocument61 pagesNitin Yadav: Brain, Mind and Markets Lab The University of Melbournevanessa8pangestuNo ratings yet

- Cyber Security ServicesDocument3 pagesCyber Security ServicesSuryakumar GubbalaNo ratings yet

- Network Security - Cryptography OverviewDocument32 pagesNetwork Security - Cryptography OverviewsusmiNo ratings yet

- Accounting Information Systems: Fourteenth EditionDocument17 pagesAccounting Information Systems: Fourteenth EditionElshafa KiranaNo ratings yet

- Whatsapp SecurityDocument6 pagesWhatsapp SecurityYousseff MooNo ratings yet

- Kubernetese HardeningDocument59 pagesKubernetese HardeningRM KamariNo ratings yet

- Aruba Switch Configuration for Authentication and Access ControlDocument26 pagesAruba Switch Configuration for Authentication and Access ControlAhmed MaherNo ratings yet

- KPN PKIoverheid CPS v5.3 EnglishDocument91 pagesKPN PKIoverheid CPS v5.3 Englishbob cellNo ratings yet