You might also like

- Residences - OG ChartDocument1 pageResidences - OG ChartPoh Yih ChernNo ratings yet

- Tekla - Steel Detailing - Basic Training DrawingDocument160 pagesTekla - Steel Detailing - Basic Training DrawingEileen Christopher100% (1)

- Staircase RailingDocument1 pageStaircase RailingPoh Yih ChernNo ratings yet

- 300 Solved Problems in Geotechnical EngineeringDocument0 pages300 Solved Problems in Geotechnical Engineeringmote3488% (17)

- Advance Installation 2013 enDocument64 pagesAdvance Installation 2013 enPoh Yih ChernNo ratings yet

- Brochure CEPCODocument2 pagesBrochure CEPCOMat Uyin0% (1)

- HARTA-Annual Report 2014 PDFDocument177 pagesHARTA-Annual Report 2014 PDFPoh Yih Chern100% (1)

- SikaGrout-215 2011-11 - 1 PDFDocument4 pagesSikaGrout-215 2011-11 - 1 PDFFaiz RahmatNo ratings yet

- Spun PileDocument7 pagesSpun Pileمحمد فيذول100% (2)

- Tie Rod CalculationDocument1 pageTie Rod CalculationPoh Yih ChernNo ratings yet

- Tekla - Steel Detailing - Basic Training DrawingDocument160 pagesTekla - Steel Detailing - Basic Training DrawingEileen Christopher100% (1)

- Module 5 (Lunar Landing)Document3 pagesModule 5 (Lunar Landing)Poh Yih ChernNo ratings yet

- Lect-3-Risk and Return (Compatibility Mode)Document70 pagesLect-3-Risk and Return (Compatibility Mode)Poh Yih ChernNo ratings yet

- Tie Rod CalculationDocument1 pageTie Rod CalculationPoh Yih ChernNo ratings yet

- ViewDocument3 pagesViewPoh Yih ChernNo ratings yet

- Arahan Teknik Jalan 2D-85-RoadMarkingDileanationDocument39 pagesArahan Teknik Jalan 2D-85-RoadMarkingDileanationAhmad Idham100% (1)

- SAP 2000 Truss Analysis TutorialDocument28 pagesSAP 2000 Truss Analysis TutorialPoh Yih ChernNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

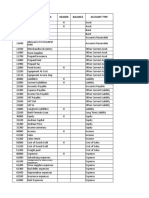

- Account Name Header Balance Account Type Account NumberDocument5 pagesAccount Name Header Balance Account Type Account NumberJohanNo ratings yet

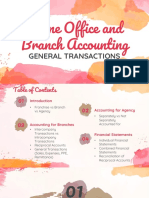

- 1.1.1. Hoba - General TransactionsDocument29 pages1.1.1. Hoba - General TransactionsJane DizonNo ratings yet

- CFA Secret Sauce QuintedgeDocument23 pagesCFA Secret Sauce QuintedgejagjitbhaimbbsNo ratings yet

- Chapter 12-The Cost of Capital: Multiple ChoiceDocument27 pagesChapter 12-The Cost of Capital: Multiple ChoiceJean CabigaoNo ratings yet

- ar40771-LingBaoGold 2008Document137 pagesar40771-LingBaoGold 2008nikkei225traderNo ratings yet

- Cleanliness Is Next To Godliness EssayDocument4 pagesCleanliness Is Next To Godliness Essayafabeaida100% (2)

- Business AnalysisDocument26 pagesBusiness AnalysisAfnanNo ratings yet

- Debt and Policy Value CaseDocument6 pagesDebt and Policy Value CaseUche Mba100% (2)

- CBSE Class 12 Accountancy - Cash Flow StatementDocument14 pagesCBSE Class 12 Accountancy - Cash Flow StatementVandna Bhaskar38% (8)

- Intermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesDocument7 pagesIntermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesdeeznutsNo ratings yet

- Resa Afar 2205 Quiz 2Document14 pagesResa Afar 2205 Quiz 2Rafael Bautista100% (1)

- Corporate Accounting ProblemDocument6 pagesCorporate Accounting ProblemparameshwaraNo ratings yet

- Internal Test - 2 - FSA - QuestionDocument3 pagesInternal Test - 2 - FSA - Questionsalil naik100% (1)

- Ar Elnusa 2018Document458 pagesAr Elnusa 2018Arif fikriNo ratings yet

- Grand Kartech Tbk. (S) : Company Report: July 2015 As of 31 July 2015Document3 pagesGrand Kartech Tbk. (S) : Company Report: July 2015 As of 31 July 2015Rina AfriyaniNo ratings yet

- Chapter - 6 Investment EvaluationDocument33 pagesChapter - 6 Investment EvaluationbelaynehNo ratings yet

- Managerial Accounting Und Erst A DingsDocument98 pagesManagerial Accounting Und Erst A DingsDebasish PadhyNo ratings yet

- MSU Accounting Departmental QuizDocument8 pagesMSU Accounting Departmental QuizMica R.No ratings yet

- Corporations Equity MCQDocument10 pagesCorporations Equity MCQMagdy KamelNo ratings yet

- Insas BerhadDocument3 pagesInsas BerhadventriaNo ratings yet

- AccountingDocument6 pagesAccountingMarjon Villanueva0% (1)

- Colgate Estados Financieros 2021Document3 pagesColgate Estados Financieros 2021Lluvia RamosNo ratings yet

- F7 Revision Test Section A and B 1Document15 pagesF7 Revision Test Section A and B 1Farman ShaikhNo ratings yet

- Chapter 1 Accounting in ActionDocument52 pagesChapter 1 Accounting in ActionAnonymous EvbW4o1U7100% (1)

- Financial Accounting Ch04Document57 pagesFinancial Accounting Ch04b2dm2k100% (1)

- Appendix FDocument17 pagesAppendix FD3 Pajak 315No ratings yet

- Day 1 Master Class by CS S Sudhakar Dividend KMP 20-6-2020 PDFDocument91 pagesDay 1 Master Class by CS S Sudhakar Dividend KMP 20-6-2020 PDFsmchmpNo ratings yet

- Financial Statements Analysis - StudentsDocument63 pagesFinancial Statements Analysis - StudentsThanh TienNo ratings yet

- IBIG 04 05 Valuation DCF AnalysisDocument118 pagesIBIG 04 05 Valuation DCF AnalysisCarloNo ratings yet

- Cfas midterm flashcardsDocument17 pagesCfas midterm flashcardsCleofe Mae Piñero AseñasNo ratings yet