You might also like

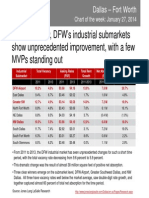

- DFW Industrial Market Shows Unprecedented ImprovementDocument1 pageDFW Industrial Market Shows Unprecedented ImprovementWalter BialasNo ratings yet

- Transportation Improvements Pave The Way For Continued Suburban Office Growth in DallasDocument1 pageTransportation Improvements Pave The Way For Continued Suburban Office Growth in DallasWalter BialasNo ratings yet

- Dallas' Top Office SubmarketsDocument1 pageDallas' Top Office SubmarketsWalter BialasNo ratings yet

- JLL - Dallas Skyline Review - Spring 2014Document1 pageJLL - Dallas Skyline Review - Spring 2014Walter BialasNo ratings yet

- Legacy Town Center's Performance Driven by Amenities and Mixed-UseDocument1 pageLegacy Town Center's Performance Driven by Amenities and Mixed-UseWalter BialasNo ratings yet

- High Tenant Diversity - Technology, Finance and Business Services Leadind Sectors in Far North Dallas SubmarketDocument1 pageHigh Tenant Diversity - Technology, Finance and Business Services Leadind Sectors in Far North Dallas SubmarketWalter BialasNo ratings yet

- Recent Home Prices and Demand in Dallas - Fort WorthDocument1 pageRecent Home Prices and Demand in Dallas - Fort WorthWalter BialasNo ratings yet

- Industrial and Flex Product Sales Transactions Steady in Dallas - Fort WorthDocument1 pageIndustrial and Flex Product Sales Transactions Steady in Dallas - Fort WorthWalter BialasNo ratings yet

- Build-To-Suit Projects and Retailers Driving Dallas' Industrial ConstructionDocument1 pageBuild-To-Suit Projects and Retailers Driving Dallas' Industrial ConstructionWalter BialasNo ratings yet

- Fort Worth Economy Shows Resilience Over Last Economic Cycels and Is Poised For Future GrowthDocument1 pageFort Worth Economy Shows Resilience Over Last Economic Cycels and Is Poised For Future GrowthWalter BialasNo ratings yet

- Alliance Airport, A Key Logistics Cetner in The DFW RegionDocument1 pageAlliance Airport, A Key Logistics Cetner in The DFW RegionWalter BialasNo ratings yet

- Nebraska Furniture Mart Expanding To DallasDocument1 pageNebraska Furniture Mart Expanding To DallasWalter BialasNo ratings yet

- Continued Hotel Recovery in Dallas Should Fuel Revenue IncreasesDocument1 pageContinued Hotel Recovery in Dallas Should Fuel Revenue IncreasesWalter BialasNo ratings yet

- Planning, Patience and Public Investment Shaping Dallas' CBD Into A "New" DowntownDocument1 pagePlanning, Patience and Public Investment Shaping Dallas' CBD Into A "New" DowntownWalter BialasNo ratings yet

- Long-Term Planning Creates New Downtown Dallas GatewayDocument1 pageLong-Term Planning Creates New Downtown Dallas GatewayWalter BialasNo ratings yet

- Retail Distress in Major Markets - Shopping Center Leasing Makes Headway at Reducing DistressDocument2 pagesRetail Distress in Major Markets - Shopping Center Leasing Makes Headway at Reducing DistressWalter BialasNo ratings yet

- Development Trends in The Rosslyn-Ballston CorridorDocument1 pageDevelopment Trends in The Rosslyn-Ballston CorridorWalter BialasNo ratings yet

- Projects Begin To Crystalize Around New Gateway To Downtown DallasDocument1 pageProjects Begin To Crystalize Around New Gateway To Downtown DallasWalter BialasNo ratings yet

- Retail Spending Patterns - Where We StandDocument2 pagesRetail Spending Patterns - Where We StandWalter BialasNo ratings yet

- Case Shiller Index ReviewDocument2 pagesCase Shiller Index ReviewWalter BialasNo ratings yet

- The Latest Job Report - "Where's The Beef"...Document2 pagesThe Latest Job Report - "Where's The Beef"...Walter BialasNo ratings yet

- DC Retail Space Leasing LeaderDocument1 pageDC Retail Space Leasing LeaderWalter BialasNo ratings yet

- Rosslyn-Ballston Versus Bethesda-Chevy ChaseDocument1 pageRosslyn-Ballston Versus Bethesda-Chevy ChaseWalter BialasNo ratings yet

- Case Shiller Index ReviewDocument2 pagesCase Shiller Index ReviewWalter BialasNo ratings yet

- DC Region Jobs - Part 2Document1 pageDC Region Jobs - Part 2Walter BialasNo ratings yet

- DC Front-Runner in Office LeasingDocument1 pageDC Front-Runner in Office LeasingWalter BialasNo ratings yet

- DC Region Jobs - Part 1Document1 pageDC Region Jobs - Part 1Walter BialasNo ratings yet

- Net Office Absorption As A Share of Leasing in DCDocument1 pageNet Office Absorption As A Share of Leasing in DCWalter BialasNo ratings yet

- Recovery in Commercial Real Estate - Wanting For JobsDocument2 pagesRecovery in Commercial Real Estate - Wanting For JobsWalter BialasNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- BCG Breaking Compromises May1997Document3 pagesBCG Breaking Compromises May1997anahata2014No ratings yet

- CarmaxDocument29 pagesCarmaxGuan Jie Xue100% (1)

- Strategic Management 2nd Edition Rothaermel Solutions Manual 1Document19 pagesStrategic Management 2nd Edition Rothaermel Solutions Manual 1dorothy100% (46)

- Best Buy Co., Inc. Customer-CentricityDocument8 pagesBest Buy Co., Inc. Customer-CentricityjddykesNo ratings yet

- AnalyticsDocument49 pagesAnalyticsdebashisdasNo ratings yet

- Progress Test Elementary Units 7, 8 and 9Document3 pagesProgress Test Elementary Units 7, 8 and 9emmrodriguez8100% (1)

- Value Investor Insight 2006-12Document20 pagesValue Investor Insight 2006-12Lucas Beaumont100% (1)

- Business Analytics: Company: BlackberryDocument15 pagesBusiness Analytics: Company: BlackberryAngelica EsguireroNo ratings yet

- ACCT2119 ABO Assessment 1 Case Study Sem 1 2024Document3 pagesACCT2119 ABO Assessment 1 Case Study Sem 1 2024ytzhang315No ratings yet

- Best BuyDocument15 pagesBest BuySharifah Norhafiza Syed Othman100% (1)

- ManagerDocument2 pagesManagerapi-78015046No ratings yet

- Strategy Formulation. Action Plan Choice (2023)Document52 pagesStrategy Formulation. Action Plan Choice (2023)Basit AliNo ratings yet

- Case Assignment MNGMNT BirhaassasaDocument9 pagesCase Assignment MNGMNT BirhaassasaBirhanu BerihunNo ratings yet

- Brand AuthenticityDocument17 pagesBrand AuthenticitySuryaWigunaNo ratings yet

- Circuit City Case StudyDocument2 pagesCircuit City Case Studyjannetka1100% (1)

- Corporate VenturingDocument28 pagesCorporate Venturingniveditha2495No ratings yet

- Case Study 1Document2 pagesCase Study 1Bizuwork Simeneh100% (2)

- Team-8 ResidencyPPTDocument17 pagesTeam-8 ResidencyPPTsai raoNo ratings yet

- 9382 - Best Buy Growth Through Segmentation.Document7 pages9382 - Best Buy Growth Through Segmentation.CfhunSaatNo ratings yet

- Best Buy's mission to make technology deliver on its promises to customersDocument12 pagesBest Buy's mission to make technology deliver on its promises to customersMiles Allen I. BenemeritoNo ratings yet

- Case Study - Circuit City CaseDocument4 pagesCase Study - Circuit City CaseMohammedNo ratings yet

- Compensation Chap 1Document23 pagesCompensation Chap 1Evelyn Grace Edwin RajanNo ratings yet

- The Everything Store Jeff Bezos and The Age of Amazon-Notebook (PDFDrive)Document24 pagesThe Everything Store Jeff Bezos and The Age of Amazon-Notebook (PDFDrive)Roman TilahunNo ratings yet

- Argyle Conversation With Steven WolkDocument6 pagesArgyle Conversation With Steven WolkMindtree LtdNo ratings yet

- Chapter One The Pay Model: 1 - 1 Compensation - Thirteenth EditionDocument23 pagesChapter One The Pay Model: 1 - 1 Compensation - Thirteenth EditionJerome Formalejo100% (1)

- Circuit City: By: Nicholas Holt, Silvana Karam, Ashish PatelDocument24 pagesCircuit City: By: Nicholas Holt, Silvana Karam, Ashish PatelAl AminNo ratings yet