You might also like

- Project Report On Idbi BankDocument45 pagesProject Report On Idbi BankFriends InternetNo ratings yet

- A Case Study Analysis On Non-Performing Assets at Union Bank of IndiaDocument56 pagesA Case Study Analysis On Non-Performing Assets at Union Bank of IndiaRahulKrishnanNo ratings yet

- Study of New Area of Customer Centric Initiatives For Retail CustomerDocument109 pagesStudy of New Area of Customer Centric Initiatives For Retail CustomerAnonymous 1B7dRLlNqNo ratings yet

- NPA Management in SBI PDFDocument118 pagesNPA Management in SBI PDFGangu DeepikaNo ratings yet

- Commodity Market QuestionnaireDocument86 pagesCommodity Market Questionnairearjunmba119624100% (1)

- Mba ProjectDocument66 pagesMba ProjectGaurav SharmaNo ratings yet

- Working Capital ProjectDocument48 pagesWorking Capital ProjectkunjapNo ratings yet

- Boney Hector D Cruz Am Ar U3com08013 Final ProjectDocument63 pagesBoney Hector D Cruz Am Ar U3com08013 Final ProjectthinckollamNo ratings yet

- DENA BANK REPORTDocument25 pagesDENA BANK REPORTJaved ShaikhNo ratings yet

- MBA Project Report of Indira Gandhi National Open UniversityDocument4 pagesMBA Project Report of Indira Gandhi National Open UniversityPrakashB144No ratings yet

- A Project On Working Capital ManagementDocument77 pagesA Project On Working Capital ManagementGurucharan SorenNo ratings yet

- Study on NPAs at SBIDocument85 pagesStudy on NPAs at SBIBasappaSarkarNo ratings yet

- Financial Literacy Project Final FileDocument70 pagesFinancial Literacy Project Final Fileaddusaiki9999No ratings yet

- Navdeep Project FinanceDocument81 pagesNavdeep Project Financedushyants65No ratings yet

- Co-Operative Banks and The Reserve Bank of India: The Regulatory Framework'Document19 pagesCo-Operative Banks and The Reserve Bank of India: The Regulatory Framework'Prachi VermaNo ratings yet

- MBA ProjectDocument59 pagesMBA ProjectRahul GordeNo ratings yet

- A Project Report On Ratio Analysis at Gadag Textile Mill Project Report Mba Finance Bec Bagalkot MbaDocument87 pagesA Project Report On Ratio Analysis at Gadag Textile Mill Project Report Mba Finance Bec Bagalkot Mbaqari saibNo ratings yet

- Gangadhar Meher University: A Study On Non Performing Asset of Scheduled Commercial Banks of India"Document42 pagesGangadhar Meher University: A Study On Non Performing Asset of Scheduled Commercial Banks of India"Sushmita BarlaNo ratings yet

- Training Report On Anand RathiDocument92 pagesTraining Report On Anand Rathirahulsogani123No ratings yet

- Sanjana Financial Statement ProjectDocument50 pagesSanjana Financial Statement ProjectPooja SahaniNo ratings yet

- Chandigarh Group of College: JhanjeriDocument65 pagesChandigarh Group of College: JhanjeriayushiNo ratings yet

- Balance Sheet Analysis of Thirumala Cotton & Agro Products Pvt LtdDocument101 pagesBalance Sheet Analysis of Thirumala Cotton & Agro Products Pvt Ltddurga prasadNo ratings yet

- Bajaj Finserv Consumer Loan StudyDocument48 pagesBajaj Finserv Consumer Loan StudyDashing HemantNo ratings yet

- SBI Non Performing AssetsDocument43 pagesSBI Non Performing AssetsVikram RokadeNo ratings yet

- Project ReportDocument15 pagesProject ReportAshish KhadakhadeNo ratings yet

- Final Project MbaDocument78 pagesFinal Project MbaMohit Goyal100% (1)

- Micro Finance ProjectDocument50 pagesMicro Finance Projectnikesh moreNo ratings yet

- A Project Report OnDocument67 pagesA Project Report OnRidhima KatiyarNo ratings yet

- Axis BankDocument91 pagesAxis BankKushambu SinghNo ratings yet

- All Project ReportDocument8 pagesAll Project Reportsrin100% (1)

- Investors' Attitude Towards Mutual FundsDocument76 pagesInvestors' Attitude Towards Mutual FundsAkshaysinh RathodNo ratings yet

- Mba ProjectDocument57 pagesMba Projectkavitha n100% (1)

- Mba Project TitlesDocument25 pagesMba Project Titlesprasad_1818No ratings yet

- Introduction to the Hotel IndustryDocument25 pagesIntroduction to the Hotel IndustryParas WaliaNo ratings yet

- List of Project Topics For MbaDocument18 pagesList of Project Topics For MbaRaj VermaNo ratings yet

- Comparative Study On Working Capital Management. at Bhilai Steel by Anil SinghDocument86 pagesComparative Study On Working Capital Management. at Bhilai Steel by Anil Singhsattu_luvNo ratings yet

- Mba ProjectDocument91 pagesMba Projectsaur1No ratings yet

- Research Project ReportDocument77 pagesResearch Project ReportsumitNo ratings yet

- Maruti Suzuki India Limited. Gurgaon: Working Capital ManagementDocument95 pagesMaruti Suzuki India Limited. Gurgaon: Working Capital ManagementMR Jems100% (1)

- SIP Project Report 2Document52 pagesSIP Project Report 2pallabi singha royNo ratings yet

- Dissertation ReportDocument47 pagesDissertation ReportSunil Kumar SharmaNo ratings yet

- Comparative Analysis of Capital Structure & Financial Performance of SBI and ICICI BankDocument85 pagesComparative Analysis of Capital Structure & Financial Performance of SBI and ICICI BankSuraj DubeyNo ratings yet

- Profit Minimisation of Icici and HDFC Ban11111Document44 pagesProfit Minimisation of Icici and HDFC Ban11111Ķālãm RãinNo ratings yet

- A Summer Training ProjectDocument130 pagesA Summer Training ProjectMansi TiwariNo ratings yet

- Sundaram Finance LTD - Financial Analysis StudyDocument10 pagesSundaram Finance LTD - Financial Analysis StudyFinance Project ReportsNo ratings yet

- Npa of SbiDocument40 pagesNpa of SbiLOCAL ADDA WAALENo ratings yet

- Comparative Analysis of Working Capital Management of Different Companies in Textile SectorDocument39 pagesComparative Analysis of Working Capital Management of Different Companies in Textile SectorMahmudul Hassan100% (1)

- MBA Fi Project NameDocument2 pagesMBA Fi Project Namerameshwar6No ratings yet

- Project Study Report of Aditya KhandelwalDocument87 pagesProject Study Report of Aditya KhandelwalAditya khandelwalNo ratings yet

- Mba M&e 2020 Project SynopsisDocument9 pagesMba M&e 2020 Project SynopsisBharathi Kannamma100% (1)

- Desk Project On Financial Risk ManagementDocument28 pagesDesk Project On Financial Risk ManagementAamirNo ratings yet

- A Comparative Study of Some Selected Mutual Fund Schemes: Project ReportDocument70 pagesA Comparative Study of Some Selected Mutual Fund Schemes: Project ReportNawnit KediaNo ratings yet

- Institute of Management Science: (Shepa) Nibia, Bachchaon, VRM Bypass Varanasi - 221001Document79 pagesInstitute of Management Science: (Shepa) Nibia, Bachchaon, VRM Bypass Varanasi - 221001dctarang50% (4)

- The Human in Human ResourceFrom EverandThe Human in Human ResourceNo ratings yet

- Green Products A Complete Guide - 2020 EditionFrom EverandGreen Products A Complete Guide - 2020 EditionRating: 5 out of 5 stars5/5 (1)

- Kotak Mahindra Bank MBA Porject Report Prince DudhatraDocument122 pagesKotak Mahindra Bank MBA Porject Report Prince DudhatrapRiNcE DuDhAtRaNo ratings yet

- CKSBDocument53 pagesCKSBRaj TiwariNo ratings yet

- History of SBI in 38Document57 pagesHistory of SBI in 38Mitali AmagdavNo ratings yet

- Stress MGMTDocument78 pagesStress MGMThiren9090No ratings yet

- LC 1Document20 pagesLC 1hiren9090No ratings yet

- LC 1Document20 pagesLC 1hiren9090No ratings yet

- Jeans: Product Project Report OnDocument76 pagesJeans: Product Project Report Onhiren9090No ratings yet

- Identifying Market Segments and TargetsDocument7 pagesIdentifying Market Segments and Targetshiren9090No ratings yet

- Excel Crop Care LTD BhujDocument105 pagesExcel Crop Care LTD Bhujhiren9090100% (4)

- Maintenance of Boeing 777 Aircraft at Air IndiaDocument56 pagesMaintenance of Boeing 777 Aircraft at Air Indiaananya100% (1)

- Summer Training Project Report SbimfDocument41 pagesSummer Training Project Report SbimfPrateek PanchalNo ratings yet

- Strategic AlliancesDocument15 pagesStrategic AlliancesAli AhmadNo ratings yet

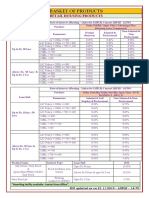

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNo ratings yet

- Mitsubishi GroupDocument3 pagesMitsubishi GroupAurang Zeb KhanNo ratings yet

- Holcim Plant ListDocument4 pagesHolcim Plant ListAkhilesh Shukla0% (1)

- J Mike Football Camp Round 2 Donations - Sheet1Document2 pagesJ Mike Football Camp Round 2 Donations - Sheet1api-322701803No ratings yet

- Chapter 9 ProblemsDocument55 pagesChapter 9 Problemsashibhallau0% (2)

- Cheat Sheet Strategy Exam MiguelDocument2 pagesCheat Sheet Strategy Exam MiguelMiguel GarçãoNo ratings yet

- Chinabank Vehicles ListDocument10 pagesChinabank Vehicles ListrapturereadyNo ratings yet

- Comprehensive Exam-Income TaxationDocument5 pagesComprehensive Exam-Income TaxationKaren May JimenezNo ratings yet

- Forms of Business Organizations and CapitalizationDocument40 pagesForms of Business Organizations and CapitalizationCindy Ortiz GastonNo ratings yet

- Marketing Group 3 - Vietjet AirDocument10 pagesMarketing Group 3 - Vietjet AirAnhNo ratings yet

- Ryanair'S Quality: Rajiv Babu ChintalaDocument11 pagesRyanair'S Quality: Rajiv Babu ChintalaexpairtiseNo ratings yet

- Bella v1Document4 pagesBella v1ug8No ratings yet

- Greene Vs MtGox Preliminary Injunction 8 April 2014Document354 pagesGreene Vs MtGox Preliminary Injunction 8 April 2014Peter N. SteinmetzNo ratings yet

- Corporate Strategies: 10 Case StudiesDocument7 pagesCorporate Strategies: 10 Case StudiesBskTeja0% (2)

- Persons. English Jurisprudence. Question and Answer. Toppers Law College. 2013-2014Document3 pagesPersons. English Jurisprudence. Question and Answer. Toppers Law College. 2013-2014Zeeshan Hussain Adil100% (1)

- 3 M Mastery ProblemDocument4 pages3 M Mastery ProblemAdam Hobbs100% (1)

- Venture Capital Firms in SoCalDocument4 pagesVenture Capital Firms in SoCalmcarney7100% (1)

- How To Trade With 5 Minute Charts - Learn The SetupsDocument18 pagesHow To Trade With 5 Minute Charts - Learn The SetupsAnshuman GuptaNo ratings yet

- Vendor Supplier Registration Information SheetDocument3 pagesVendor Supplier Registration Information SheetEnzo MarquezNo ratings yet

- Neft ProjectDocument69 pagesNeft ProjectArshad ShakeelNo ratings yet

- Decision-making case analyzes market investment alternativesDocument5 pagesDecision-making case analyzes market investment alternativesNicolas AjiquichiNo ratings yet

- Secretary Certification For MetrobankDocument2 pagesSecretary Certification For MetrobankJImlan Sahipa Ismael67% (3)

- Hospitality Design Magazine 1Document8 pagesHospitality Design Magazine 1NatalinaNo ratings yet

- Organizational Structure INTESADocument1 pageOrganizational Structure INTESAJovanka KovacinaNo ratings yet

- CEO Road Rules1Document233 pagesCEO Road Rules1sammyyankee100% (1)

- Annual Report & Financial Statements 2017: Safari Lodges and Camps Hotels - ResortsDocument90 pagesAnnual Report & Financial Statements 2017: Safari Lodges and Camps Hotels - ResortsajwadkhanNo ratings yet

- IAS 37 Provisions Contingencies AccountingDocument2 pagesIAS 37 Provisions Contingencies AccountingLýHuyHoàng100% (1)