You might also like

- Cust Feed FormDocument5 pagesCust Feed FormVarun AmritwarNo ratings yet

- Rodger PDFDocument1 pageRodger PDFA TUNo ratings yet

- What Is Administrative Model of Curriculum?Document9 pagesWhat Is Administrative Model of Curriculum?Varun AmritwarNo ratings yet

- NileshDocument6 pagesNileshVarun AmritwarNo ratings yet

- UploadedFile 130770920993579162Document9 pagesUploadedFile 130770920993579162Varun AmritwarNo ratings yet

- Form 231Document7 pagesForm 231Varun AmritwarNo ratings yet

- UploadedFile 130770920993579162Document9 pagesUploadedFile 130770920993579162Varun AmritwarNo ratings yet

- There Are Many Colleges That Provides Many Foundation CourseDocument2 pagesThere Are Many Colleges That Provides Many Foundation CourseVarun AmritwarNo ratings yet

- Chandra Shekhar Deputy Director General: Bureau of Indian Standards New Delhi IndiaDocument27 pagesChandra Shekhar Deputy Director General: Bureau of Indian Standards New Delhi IndiasameeryashuNo ratings yet

- Compulsory EnglishDocument7 pagesCompulsory EnglishVarun AmritwarNo ratings yet

- Education Qualification ResumeDocument1 pageEducation Qualification ResumeVarun AmritwarNo ratings yet

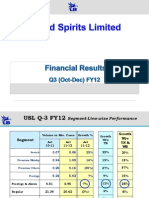

- Usl Q3 Fy12Document11 pagesUsl Q3 Fy12Varun AmritwarNo ratings yet

- Rural Market FinalDocument7 pagesRural Market FinalVarun AmritwarNo ratings yet

- Non Formal EducationDocument13 pagesNon Formal Educationkdatta86No ratings yet

- Rural Market FinalDocument7 pagesRural Market FinalVarun AmritwarNo ratings yet

- Rama SesDocument2 pagesRama SesVarun AmritwarNo ratings yet

- UBHL Annual Report 2011Document89 pagesUBHL Annual Report 2011Varun AmritwarNo ratings yet

- Diageo (DEO) Stock Analysis and Recommendation HOLDDocument31 pagesDiageo (DEO) Stock Analysis and Recommendation HOLDVarun AmritwarNo ratings yet

- Calgary An Over View - New Destination: Eographic Ocation OF Algary CityDocument4 pagesCalgary An Over View - New Destination: Eographic Ocation OF Algary CityVarun AmritwarNo ratings yet

- Summertrainingreport 121128042459 Phpapp01Document40 pagesSummertrainingreport 121128042459 Phpapp01adihindNo ratings yet

- Brand Solutions From: India's Pioneer and Stickiest Bollywood PortalDocument36 pagesBrand Solutions From: India's Pioneer and Stickiest Bollywood PortalVarun AmritwarNo ratings yet

- Ek 2007 ArDocument215 pagesEk 2007 ArVarun AmritwarNo ratings yet

- Calgary An Over View - New Destination: Eographic Ocation OF Algary CityDocument4 pagesCalgary An Over View - New Destination: Eographic Ocation OF Algary CityVarun AmritwarNo ratings yet

- TradeDocument1 pageTradeVarun AmritwarNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hello CanadaDocument4 pagesHello Canada10ashvikaaNo ratings yet

- Service Capability Presentation - MXDMDocument16 pagesService Capability Presentation - MXDMAlwin SamuelNo ratings yet

- Small PPP SCPDocument22 pagesSmall PPP SCPPattasan UNo ratings yet

- Day 2 - Discussion On M&A TransactionsDocument31 pagesDay 2 - Discussion On M&A TransactionsMAHANTESH GNo ratings yet

- Cindy and Jack Have Always Practiced Good Financial Habits inDocument1 pageCindy and Jack Have Always Practiced Good Financial Habits inAmit PandeyNo ratings yet

- GUCCI - Case Only110910Document39 pagesGUCCI - Case Only110910sabastien_10dec5663No ratings yet

- Audit Procedures and Risk ResponseDocument7 pagesAudit Procedures and Risk ResponseJwyneth Royce DenolanNo ratings yet

- Makati Comprehensive Land Use Plan 2013-2023 (CLUP)Document81 pagesMakati Comprehensive Land Use Plan 2013-2023 (CLUP)Godofredo Sanchez73% (11)

- Yahoo! Presentation To Stockholders: June 2008Document32 pagesYahoo! Presentation To Stockholders: June 2008erickschonfeld100% (5)

- Practice Standard For Project Risk Management by PMIDocument128 pagesPractice Standard For Project Risk Management by PMIMJ MagdyNo ratings yet

- About Us PropelisDocument5 pagesAbout Us PropelismaverickmuglikarNo ratings yet

- GORR Enterprises seeks 15% IT cost reduction through outsourcing partnershipDocument9 pagesGORR Enterprises seeks 15% IT cost reduction through outsourcing partnershipShivendra Pal SinghNo ratings yet

- University of Mumbai: (Summer)Document1 pageUniversity of Mumbai: (Summer)Rishu TripathiNo ratings yet

- Organizational Structures That Accelerate InnovationDocument4 pagesOrganizational Structures That Accelerate InnovationPaul SunNo ratings yet

- Accounting, Anatomy, Anthropology and Archaeology paper codesDocument288 pagesAccounting, Anatomy, Anthropology and Archaeology paper codesmanesh1740% (1)

- Multiple Choice Questions: Analyzing Operating ActivitiesDocument22 pagesMultiple Choice Questions: Analyzing Operating ActivitiesAnh LýNo ratings yet

- Activities To Promote EntrepreneurshipDocument12 pagesActivities To Promote EntrepreneurshipRichell PayosNo ratings yet

- K1. Using The Adjusted Trial Balance Prepared in P...Document6 pagesK1. Using The Adjusted Trial Balance Prepared in P...M Younis ShujraNo ratings yet

- DIH 1011 AdministratorGuide enDocument114 pagesDIH 1011 AdministratorGuide enfedNo ratings yet

- Case Elon Musk's Twitter Deal Valuation and Financing of The Leveraged Buyout 2023-1Document15 pagesCase Elon Musk's Twitter Deal Valuation and Financing of The Leveraged Buyout 2023-1Daniel Ali Padilla VerdeNo ratings yet

- Account Sales ReportDocument12 pagesAccount Sales Reportsamuel debebeNo ratings yet

- Branch Banking SystemDocument16 pagesBranch Banking SystemPrathyusha ReddyNo ratings yet

- Auditing in CIS Environment - Topic 1 - Developing and Implementing A Risk-Based IT Audit StrategyDocument35 pagesAuditing in CIS Environment - Topic 1 - Developing and Implementing A Risk-Based IT Audit StrategyLuisitoNo ratings yet

- Modern Service Management For Azure v1.1Document45 pagesModern Service Management For Azure v1.1Ines MariaNo ratings yet

- Datasheet Workday AboutDocument3 pagesDatasheet Workday Aboutsantosh kumarNo ratings yet

- Fundamentals of Financial Management Concise 8Th Edition PDF Full ChapterDocument41 pagesFundamentals of Financial Management Concise 8Th Edition PDF Full Chaptersheryl.bates344100% (26)

- Customer SatisfactionDocument4 pagesCustomer SatisfactionrolandNo ratings yet

- Capital Market Instruments Are Basically Either Equity (Stock) Securities or Debt (Bond)Document2 pagesCapital Market Instruments Are Basically Either Equity (Stock) Securities or Debt (Bond)maryaniNo ratings yet

- Bop Final PDFDocument19 pagesBop Final PDFshashi singhNo ratings yet

- Supply Chain Management CourseDocument2 pagesSupply Chain Management CoursemadhiNo ratings yet