You might also like

- Kenanga Today-230321 (Kenanga)Document5 pagesKenanga Today-230321 (Kenanga)hl lowNo ratings yet

- Stock Market Reports For The Week (9th - 13th May '11)Document6 pagesStock Market Reports For The Week (9th - 13th May '11)Dasher_No_1No ratings yet

- Sapa Mentari 181023 07.39.23Document6 pagesSapa Mentari 181023 07.39.23Diense ZhangNo ratings yet

- Pi Daily Strategy 24112023 SumDocument7 pagesPi Daily Strategy 24112023 SumPateera Chananti PhoomwanitNo ratings yet

- Trusts - November 4 2019Document24 pagesTrusts - November 4 2019Lisle Daverin BlythNo ratings yet

- Sapa Mentari 121023Document6 pagesSapa Mentari 121023Diense ZhangNo ratings yet

- Kenanga Today - 230322 (Kenanga)Document5 pagesKenanga Today - 230322 (Kenanga)hl lowNo ratings yet

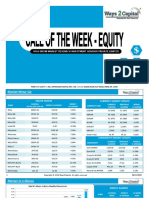

- Equity Research Report 13 November 2018 Ways2CapitalDocument17 pagesEquity Research Report 13 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Daily Mutual Fund Perfomance Per 06 September 2022Document1 pageDaily Mutual Fund Perfomance Per 06 September 2022Luna Fitria KusumaNo ratings yet

- Kenanga Today 240116 KenangaDocument6 pagesKenanga Today 240116 KenangaChee TonyNo ratings yet

- Sectors That'll Perform Considering All The Macro-Economic FactorsDocument11 pagesSectors That'll Perform Considering All The Macro-Economic FactorsADITYA RANJANNo ratings yet

- Kenyan Brokerage & Investment Banking Financial Results 2009Document83 pagesKenyan Brokerage & Investment Banking Financial Results 2009moneyedkenyaNo ratings yet

- India's Top Performing Mutual Funds TablesDocument3 pagesIndia's Top Performing Mutual Funds TablespbsoodNo ratings yet

- Daily 07 March 2024Document5 pagesDaily 07 March 2024enockmartha01No ratings yet

- Major Pharma Companies Performance OverviewDocument28 pagesMajor Pharma Companies Performance OverviewADNo ratings yet

- Equity Report 6 To 10 NovDocument6 pagesEquity Report 6 To 10 NovzoidresearchNo ratings yet

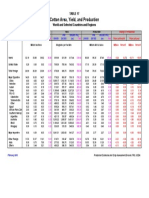

- Cotton YieldDocument1 pageCotton YieldGan Gan ChanNo ratings yet

- Equity Research Report 27 November 2018 Ways2CapitalDocument17 pagesEquity Research Report 27 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- Healthcare WorkingDocument13 pagesHealthcare Workingsunway.senai2No ratings yet

- Sapa Mentari 120923Document6 pagesSapa Mentari 120923Peter AndreasNo ratings yet

- The Standard - Business Daily Stocks Review (June 4, 2015)Document1 pageThe Standard - Business Daily Stocks Review (June 4, 2015)Manila Standard TodayNo ratings yet

- Data AnalysisDocument13 pagesData AnalysisAytenfisu AyuNo ratings yet

- Equity Reports For The Week (25th - 29th April '11)Document6 pagesEquity Reports For The Week (25th - 29th April '11)Dasher_No_1No ratings yet

- Sapa Mentari 261023Document6 pagesSapa Mentari 261023Diense ZhangNo ratings yet

- NSE market report August 2020Document1 pageNSE market report August 2020Vaite JamesNo ratings yet

- Markets and Commodity Figures: 24 July 2017Document4 pagesMarkets and Commodity Figures: 24 July 2017Tiso Blackstar GroupNo ratings yet

- Equity Research Report 06 November 2018 Ways2CapitalDocument17 pagesEquity Research Report 06 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- BetaDocument1 pageBetaalirazajokarNo ratings yet

- Statistical Annex WCR 2022Document30 pagesStatistical Annex WCR 2022Lorena PérezNo ratings yet

- Table Rate PF JULY 2020 Debt Cons BMDocument1 pageTable Rate PF JULY 2020 Debt Cons BMwaliqutubNo ratings yet

- Africa Investor - July 25 2017Document4 pagesAfrica Investor - July 25 2017Tiso Blackstar GroupNo ratings yet

- Stock Market Reports For The Week (16th - 20th May '11)Document6 pagesStock Market Reports For The Week (16th - 20th May '11)Dasher_No_1No ratings yet

- Sapa Mentari 140923Document6 pagesSapa Mentari 140923Reindy Katon BagaskaraNo ratings yet

- Global Macro Indicators - 29 Oct 19Document7 pagesGlobal Macro Indicators - 29 Oct 19Ram AhujaNo ratings yet

- Africa InvestorDocument4 pagesAfrica InvestorTiso Blackstar GroupNo ratings yet

- Analisis Sensitivitas Sensitivity AnalysisDocument26 pagesAnalisis Sensitivitas Sensitivity AnalysisardiNo ratings yet

- Top 1000 World Banks SGwebDocument2 pagesTop 1000 World Banks SGwebobee1234No ratings yet

- Stock Market Reports For The Week (21st - 25th March - 2011)Document6 pagesStock Market Reports For The Week (21st - 25th March - 2011)Dasher_No_1No ratings yet

- Equity Reports For The Week (2nd - 6th May '11)Document6 pagesEquity Reports For The Week (2nd - 6th May '11)Dasher_No_1No ratings yet

- FundPerformance UpdateDocument1 pageFundPerformance UpdateAzwan YusoffNo ratings yet

- Africa Investor - April 24 2017Document4 pagesAfrica Investor - April 24 2017Tiso Blackstar GroupNo ratings yet

- Coca-Cola Co Financials at a Glance (2008-2017Document6 pagesCoca-Cola Co Financials at a Glance (2008-2017SibghaNo ratings yet

- Team Arthaniti - K J Somaiya Institute of ManagementDocument22 pagesTeam Arthaniti - K J Somaiya Institute of Managementpratyay gangulyNo ratings yet

- Daily Trade Journal - 05.03Document7 pagesDaily Trade Journal - 05.03ran2013No ratings yet

- Zakat Expenditure & Real Output Oic Conference 2009Document26 pagesZakat Expenditure & Real Output Oic Conference 2009GonzQluaNo ratings yet

- Annual Stock Price and Return Data For Six StocksDocument5 pagesAnnual Stock Price and Return Data For Six Stocksmirza azeemNo ratings yet

- AfricaInvestor - June 26 2017Document4 pagesAfricaInvestor - June 26 2017Tiso Blackstar GroupNo ratings yet

- CompetitorsDocument2 pagesCompetitorsBhavani RaoNo ratings yet

- Get Personal Financing Rates as Low as 2.67% from Bank IslamDocument1 pageGet Personal Financing Rates as Low as 2.67% from Bank IslamMr FarukNo ratings yet

- Africa Investor - May 4 2018Document4 pagesAfrica Investor - May 4 2018Tiso Blackstar GroupNo ratings yet

- Variance Covariance Matrix in ExcelDocument25 pagesVariance Covariance Matrix in Excelkashmira0% (1)

- Weekly Report - Xxi - May 23 To 27, 2011Document3 pagesWeekly Report - Xxi - May 23 To 27, 2011JC CalaycayNo ratings yet

- Equity Research Report 20 November 2018 Ways2CapitalDocument17 pagesEquity Research Report 20 November 2018 Ways2CapitalWays2CapitalNo ratings yet

- List Arab Countries 439jDocument2 pagesList Arab Countries 439jChinelonma AnaetohNo ratings yet

- TATA MOTORS LTD KEY FINANCIALS & RATIOSDocument10 pagesTATA MOTORS LTD KEY FINANCIALS & RATIOSAtharv AgrawalNo ratings yet

- National Stock ExchangeDocument8 pagesNational Stock ExchangeCA Manoj GuptaNo ratings yet

- Sample IAS 29 COS ComputationDocument29 pagesSample IAS 29 COS ComputationShingirai CynthiaNo ratings yet

- Entrepreneurial Mindset PDFDocument6 pagesEntrepreneurial Mindset PDFkkhrie767% (3)

- Waumini by LawsDocument31 pagesWaumini by LawsxprettyNo ratings yet

- BACKGROUND AND DEFINITION SECTIONDocument2 pagesBACKGROUND AND DEFINITION SECTIONxprettyNo ratings yet

- Barclays Bank of Kenya IOCDocument6 pagesBarclays Bank of Kenya IOCxprettyNo ratings yet

- The Akikuyu of British East AfricaDocument626 pagesThe Akikuyu of British East Africaxpretty100% (2)

- DR Ouko FactfileDocument61 pagesDR Ouko FactfilexprettyNo ratings yet

- Barclays Bank of Kenya IOCDocument6 pagesBarclays Bank of Kenya IOCxprettyNo ratings yet

- Gospel Bearers, Gender BarriersDocument12 pagesGospel Bearers, Gender BarriersxprettyNo ratings yet

- National Bank of Kenya Financial Results 30 September 2010Document1 pageNational Bank of Kenya Financial Results 30 September 2010xprettyNo ratings yet

- Gospel Bearers, Gender BarriersDocument12 pagesGospel Bearers, Gender BarriersxprettyNo ratings yet

- List of Kenyan Violence Perpetrators 2008Document54 pagesList of Kenyan Violence Perpetrators 2008Maskani Ya TaifaNo ratings yet

- Final ProjectDocument5 pagesFinal ProjectAkshayNo ratings yet

- International Law Subjects Case Rules MOA-AD UnconstitutionalDocument9 pagesInternational Law Subjects Case Rules MOA-AD UnconstitutionalMarie FayeNo ratings yet

- B215 AC08 Mochi Kochi 6th Presentation 19 June 2009Document46 pagesB215 AC08 Mochi Kochi 6th Presentation 19 June 2009tohqinzhiNo ratings yet

- Cambodia Policing SystemDocument31 pagesCambodia Policing SystemAverie Ann MamarilNo ratings yet

- Blacks and The Seminole War PDFDocument25 pagesBlacks and The Seminole War PDFcommshackNo ratings yet

- JMNLUA Call For PapersDocument3 pagesJMNLUA Call For PapersashikhadileepNo ratings yet

- Fundamentals of Indian Legal SystemDocument30 pagesFundamentals of Indian Legal SystemvaderNo ratings yet

- OTC107401 OptiX NG WDM Optical Layer Grooming ISSUE1.04Document61 pagesOTC107401 OptiX NG WDM Optical Layer Grooming ISSUE1.04Claudio SaezNo ratings yet

- Affidavit landholding CalapanDocument3 pagesAffidavit landholding CalapanNathaniel CamachoNo ratings yet

- FIAML Regulations 2018Document34 pagesFIAML Regulations 2018Bhoumika LucknauthNo ratings yet

- Lesson 1 Copy BusiLawDocument25 pagesLesson 1 Copy BusiLawpawiiikaaaanNo ratings yet

- Amendment of PleadingDocument21 pagesAmendment of PleadingRvi MahayNo ratings yet

- Citizen's Response To The Ejipura Demolitions - Comments On The Change - Org PetitionDocument49 pagesCitizen's Response To The Ejipura Demolitions - Comments On The Change - Org PetitionewsejipuraNo ratings yet

- 33 Dale Stricland Vs Ernst & Young 8 1 18 G.R. No. 193782Document3 pages33 Dale Stricland Vs Ernst & Young 8 1 18 G.R. No. 193782RubenNo ratings yet

- Freezing of subcooled water and entropy changeDocument3 pagesFreezing of subcooled water and entropy changeAchmad WidiyatmokoNo ratings yet

- E VisaDocument2 pagesE VisaPrabha KaranNo ratings yet

- Public Private Partnership Model For Affordable Housing Provision in NigeriaDocument14 pagesPublic Private Partnership Model For Affordable Housing Provision in Nigeriawidya nugrahaNo ratings yet

- Mathcad CustomerServiceGuideDocument13 pagesMathcad CustomerServiceGuidenonfacedorkNo ratings yet

- Noting SkillsDocument53 pagesNoting Skillsjao npgajwelNo ratings yet

- Tripura Public Service CommissionDocument4 pagesTripura Public Service CommissionMintu DebbarmaNo ratings yet

- The Hmong People's Sacrifice for US Freedom in the Secret War in LaosDocument3 pagesThe Hmong People's Sacrifice for US Freedom in the Secret War in Laosbabyboy1972No ratings yet

- QUAL7427613SYN Cost of Quality PlaybookDocument58 pagesQUAL7427613SYN Cost of Quality Playbookranga.ramanNo ratings yet

- Patterns of AllophonyDocument6 pagesPatterns of AllophonyPeter ClarkNo ratings yet

- Audit ProceduresDocument5 pagesAudit Procedureskenoly123No ratings yet

- Cut Nyak Dien Biography English Language VersionDocument4 pagesCut Nyak Dien Biography English Language VersionWahyupuji Astuti100% (1)

- Workers Participation Case IDocument3 pagesWorkers Participation Case IAlka Jain100% (1)

- ECtHR - Hassan X United KingdomDocument2 pagesECtHR - Hassan X United KingdomanavzanattaNo ratings yet

- Clinical Course Appellant Final MemoDocument21 pagesClinical Course Appellant Final MemoKhushboo SharmaNo ratings yet

- Cogta Report Version 14Document70 pagesCogta Report Version 14VukileNo ratings yet

- Agenda 21Document2 pagesAgenda 21Hal Shurtleff100% (1)