You might also like

- Chapter 23 PPEDocument5 pagesChapter 23 PPERose AysonNo ratings yet

- FAR.104 PPE Acquisition and Subsequent ExpendituresDocument7 pagesFAR.104 PPE Acquisition and Subsequent ExpendituresMarlon Jeff Concepcion Cariaga100% (2)

- 9.1 Equity Investments at Fair Value PDFDocument4 pages9.1 Equity Investments at Fair Value PDFJorufel PapasinNo ratings yet

- PPEDocument2 pagesPPEVince Pereda0% (1)

- Cup 1 - FARDocument8 pagesCup 1 - FARJeric Lagyaban AstrologioNo ratings yet

- FAR - RQ - Investment in AssociatesDocument2 pagesFAR - RQ - Investment in AssociatesKriane Kei50% (2)

- Handout For Mas Mastery Class 1Document11 pagesHandout For Mas Mastery Class 1Makoy BixenmanNo ratings yet

- Ppe Bio AssetDocument2 pagesPpe Bio AssetEvita Faith LeongNo ratings yet

- Far Eastern University Department of Accountancy & Internal Auditing Intermediate Accounting 1 Midterm Grading PeriodDocument8 pagesFar Eastern University Department of Accountancy & Internal Auditing Intermediate Accounting 1 Midterm Grading PeriodJOSCEL SYJONGTIANNo ratings yet

- Intermediate Accounting 1 - Cash and Cash Equivalent - Test BankDocument9 pagesIntermediate Accounting 1 - Cash and Cash Equivalent - Test BankKabayanNo ratings yet

- ReviewerDocument5 pagesReviewermaricielaNo ratings yet

- Business Law SurecpaDocument35 pagesBusiness Law SurecpaChessaAlenelLigutom100% (1)

- Intermacc Inventories and Bio Assets Postlec WaDocument2 pagesIntermacc Inventories and Bio Assets Postlec WaClarice Awa-aoNo ratings yet

- Aud Application 2 - Handout 8 Intangible (UST)Document4 pagesAud Application 2 - Handout 8 Intangible (UST)RNo ratings yet

- Chapter 8 OkDocument37 pagesChapter 8 OkMa. Alexandra Teddy Buen0% (1)

- Vat On Importation: Presumptive Input TaxDocument13 pagesVat On Importation: Presumptive Input TaxNerish PlazaNo ratings yet

- Test Bank Auditng ProbDocument11 pagesTest Bank Auditng ProbTinne PaculabaNo ratings yet

- Chapter 14 - Retail Inventory Method PDFDocument9 pagesChapter 14 - Retail Inventory Method PDFTurksNo ratings yet

- AP.105 Audit of InvestmentsDocument8 pagesAP.105 Audit of InvestmentsJonathan FestinNo ratings yet

- Semis Examination BDocument12 pagesSemis Examination BCHENG50% (2)

- PPE Acquisition EssentialsDocument3 pagesPPE Acquisition EssentialsRNo ratings yet

- NC Concept MapDocument3 pagesNC Concept MapMitch MindanaoNo ratings yet

- UAS-ACCT6130-cost Accounting-Latihan persiapan-PJJDocument4 pagesUAS-ACCT6130-cost Accounting-Latihan persiapan-PJJOlim BariziNo ratings yet

- Practical Accounting 1Document32 pagesPractical Accounting 1EdenA.Mata100% (9)

- Accounting Review and Tutorial Services in San Isidro, Nueva EcijaDocument8 pagesAccounting Review and Tutorial Services in San Isidro, Nueva EcijaEiuol Nhoj Arraeugse100% (3)

- Allapacan Company Bought 20Document18 pagesAllapacan Company Bought 20Carl Yry BitzNo ratings yet

- Far 09 Government GrantsDocument9 pagesFar 09 Government GrantsJoshua UmaliNo ratings yet

- PAS 36 Concept MapDocument1 pagePAS 36 Concept MapMicah RamaykaNo ratings yet

- Quiz - Ppe CostDocument2 pagesQuiz - Ppe CostAna Mae HernandezNo ratings yet

- Financial Accounting and Reporting: INVENTORIES (Part 1Document9 pagesFinancial Accounting and Reporting: INVENTORIES (Part 1DyenNo ratings yet

- Ch08 Property, Plant & EquipmentDocument6 pagesCh08 Property, Plant & EquipmentralphalonzoNo ratings yet

- Cost Accounting and CostManagementDocument35 pagesCost Accounting and CostManagementLiza Magat MatadlingNo ratings yet

- Module 3 Quiz On Investment PropertiesDocument5 pagesModule 3 Quiz On Investment PropertiesLoven Boado100% (1)

- Auditing Problems Since 1977Document7 pagesAuditing Problems Since 1977Io AyaNo ratings yet

- Chapter 4 Accounts ReceivableDocument12 pagesChapter 4 Accounts Receivableweddiemae villariza50% (2)

- Financial Accounting Review Problem 1Document16 pagesFinancial Accounting Review Problem 1YukiNo ratings yet

- Reviewer & Answers (Inventories)Document5 pagesReviewer & Answers (Inventories)Kimboy Elizalde Panaguiton100% (3)

- Intermediate Accounting 1 Departmental Exam MidtermsDocument6 pagesIntermediate Accounting 1 Departmental Exam MidtermsCharles AtimNo ratings yet

- ACt1104 Final Quiz No. 1wit AnsDocument7 pagesACt1104 Final Quiz No. 1wit AnsDyenNo ratings yet

- Cfas Finals Quiz 1 A4 Set C With Answers PDFDocument4 pagesCfas Finals Quiz 1 A4 Set C With Answers PDFIts meh SushiNo ratings yet

- 4.0 Standard Costing 2018Document15 pages4.0 Standard Costing 2018Christian Geronimo100% (1)

- Government Accounting - PPEDocument4 pagesGovernment Accounting - PPEEliyah JhonsonNo ratings yet

- 4 InventoriesDocument5 pages4 InventoriesandreamrieNo ratings yet

- Depletion: Valix, C. T. Et Al. Intermediate GIC Enterprises & Co. IncDocument21 pagesDepletion: Valix, C. T. Et Al. Intermediate GIC Enterprises & Co. IncJoris YapNo ratings yet

- PPE Accounting PrinciplesDocument6 pagesPPE Accounting Principlesmae cruzNo ratings yet

- Case Study 4Document4 pagesCase Study 4RoseanneNo ratings yet

- Audit of LiabilitiesDocument36 pagesAudit of Liabilitiesjaymark canaya0% (1)

- Property, Plant and Equipment: Recognition of PPEDocument6 pagesProperty, Plant and Equipment: Recognition of PPEbigbaekNo ratings yet

- Ppe RevaluationDocument6 pagesPpe RevaluationjonapdfsNo ratings yet

- PPE Criteria - LandDocument9 pagesPPE Criteria - LandHappyPurpleNo ratings yet

- Property Plant and Equipment, GovernmentDocument17 pagesProperty Plant and Equipment, GovernmentJomerNo ratings yet

- Blessed Me LordDocument168 pagesBlessed Me LordBoa HancockNo ratings yet

- Report in Accrev (Ppe)Document18 pagesReport in Accrev (Ppe)PaulineBiroselNo ratings yet

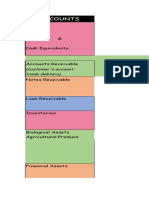

- Accounts: (Customer's Account, Trade Debtors)Document48 pagesAccounts: (Customer's Account, Trade Debtors)RaphaelleNo ratings yet

- 805 CC101 AFM DD 2 Valuation of Tangible F.assetsDocument32 pages805 CC101 AFM DD 2 Valuation of Tangible F.assetsArchana N VyasNo ratings yet

- Ia 2 - Ppe SheDocument22 pagesIa 2 - Ppe SheAlisonNo ratings yet

- Classifying and Accounting for Government GrantsDocument2 pagesClassifying and Accounting for Government GrantsCatherine Joy MoralesNo ratings yet

- Ia 2 Ppe She 1Document22 pagesIa 2 Ppe She 1AlisonNo ratings yet

- Property Plant and EquipmentDocument5 pagesProperty Plant and EquipmentSinead ErelahNo ratings yet

- PAS 16 Property, Plant and EquipmentDocument4 pagesPAS 16 Property, Plant and Equipmentpanda 1No ratings yet

- Reviewer in PPEDocument16 pagesReviewer in PPEDewi Leigh Ann Mangubat50% (2)

- ValuesDocument27 pagesValuesDewi Leigh Ann MangubatNo ratings yet

- Reviewer in PPEDocument16 pagesReviewer in PPEDewi Leigh Ann Mangubat50% (2)

- SYD Method of DepreciationDocument1 pageSYD Method of DepreciationDewi Leigh Ann MangubatNo ratings yet

- No. 6 QuestionDocument1 pageNo. 6 QuestionDewi Leigh Ann MangubatNo ratings yet

- AfsDocument6 pagesAfsDewi Leigh Ann MangubatNo ratings yet

- No. 8 QuestionDocument1 pageNo. 8 QuestionDewi Leigh Ann MangubatNo ratings yet

- No. 5 QuestionDocument1 pageNo. 5 QuestionDewi Leigh Ann MangubatNo ratings yet

- 3 Notes To Income StatementDocument8 pages3 Notes To Income StatementDewi Leigh Ann MangubatNo ratings yet

- An Introduction To Bank Debenture Trading Programs EducDocument28 pagesAn Introduction To Bank Debenture Trading Programs EducLuis Alberto CamusNo ratings yet

- RA 8291 GSIS ActDocument19 pagesRA 8291 GSIS ActAicing Namingit-VelascoNo ratings yet

- Interest RatesDocument38 pagesInterest RatesLealyn CuestaNo ratings yet

- The Wealthy Mindset E BookDocument31 pagesThe Wealthy Mindset E BookDiana RuizNo ratings yet

- Pecora FinalReportDocument402 pagesPecora FinalReportAdelino MartinsNo ratings yet

- Module 5: Evaluating A Single ProjectDocument50 pagesModule 5: Evaluating A Single Project우마이라UmairahNo ratings yet

- Agencies JPMDocument18 pagesAgencies JPMbonefish212No ratings yet

- Topic 52 Quantifying Volatility in VaR Models - Answers PDFDocument41 pagesTopic 52 Quantifying Volatility in VaR Models - Answers PDFSoumava PalNo ratings yet

- Working Capital ManagementDocument41 pagesWorking Capital ManagementsadfiziaNo ratings yet

- Cincinnati 2021 Annual Financial ReportDocument317 pagesCincinnati 2021 Annual Financial ReportAlicia Brown100% (1)

- Understanding Sukuk: An Islamic Alternative to Conventional BondsDocument4 pagesUnderstanding Sukuk: An Islamic Alternative to Conventional BondsOwais KhakwaniNo ratings yet

- Arbitrage PDFDocument60 pagesArbitrage PDFdan4everNo ratings yet

- Notes NismDocument182 pagesNotes NismMCQ NISMNo ratings yet

- Ecos Plastics CompanyDocument2 pagesEcos Plastics CompanyRAJUNo ratings yet

- 5 - Capital Investment Appraisal (Part-2)Document10 pages5 - Capital Investment Appraisal (Part-2)Fahim HussainNo ratings yet

- BookkeepingDocument20 pagesBookkeepingzhanel bekenovaNo ratings yet

- Islamic Capital Markets: The Role of Sukuk: Executive SummaryDocument4 pagesIslamic Capital Markets: The Role of Sukuk: Executive SummaryiisjafferNo ratings yet

- Capital MarketDocument10 pagesCapital MarketEduar GranadaNo ratings yet

- Rescheduling DebtDocument50 pagesRescheduling DebtMBA...KID100% (4)

- MUTUAL FUNDS INTRODocument11 pagesMUTUAL FUNDS INTROGopal GurjarNo ratings yet

- PURPOSE CLAUSE (Investment Corporation)Document2 pagesPURPOSE CLAUSE (Investment Corporation)Glae AdrianoNo ratings yet

- Assefa W OredeDocument76 pagesAssefa W Oredesamibelay1234No ratings yet

- Financial Management Course OutlineDocument9 pagesFinancial Management Course OutlinebiggykhairNo ratings yet

- Financial - Glossary MerrylDocument345 pagesFinancial - Glossary MerrylTC CarlosNo ratings yet

- Interest Rate Swap ThesisDocument5 pagesInterest Rate Swap Thesisdwham6h1100% (2)

- Practical Accounting 1 Comprehensive ExamsDocument3 pagesPractical Accounting 1 Comprehensive ExamsCris Tarrazona CasipleNo ratings yet

- William Ackman - Everything You Need To Know About Finance and Investing in Under An HourDocument16 pagesWilliam Ackman - Everything You Need To Know About Finance and Investing in Under An HourAnonymous kFK83ev100% (1)

- 02-02 - IfRS 17 Insurance Contracts - Illustrative Example On The Variable Fee Approach - TEG 17-02-23Document41 pages02-02 - IfRS 17 Insurance Contracts - Illustrative Example On The Variable Fee Approach - TEG 17-02-23marhadiNo ratings yet

- TEST 5 PreparationDocument8 pagesTEST 5 PreparationAna GloriaNo ratings yet

- Indian Financial System Dba1749Document193 pagesIndian Financial System Dba1749Santhosh GeorgeNo ratings yet