You might also like

- BP Peak Oil Demand and Long Run Oil PricesDocument20 pagesBP Peak Oil Demand and Long Run Oil PricesKokil JainNo ratings yet

- Energy Outlook 2014Document6 pagesEnergy Outlook 2014Esdras DemoroNo ratings yet

- OG MarketDocument276 pagesOG MarketoptisearchNo ratings yet

- Adjustment in The Oil Market Structural Cyclical or BothDocument23 pagesAdjustment in The Oil Market Structural Cyclical or BothjaehyukNo ratings yet

- Appendix Peak Oil & Australian EconomyDocument17 pagesAppendix Peak Oil & Australian Economykirubha_karan2000No ratings yet

- Iv. Oil Price Developments: Drivers, Economic Consequences and Policy ResponsesDocument29 pagesIv. Oil Price Developments: Drivers, Economic Consequences and Policy Responsesdonghao66No ratings yet

- Understanding Shocks of Oil Prices: IJASCSE Vol 1 Issue 1 2012Document7 pagesUnderstanding Shocks of Oil Prices: IJASCSE Vol 1 Issue 1 2012IJASCSENo ratings yet

- OPEC+ Production Cut Impact on Oil Prices & MarketDocument6 pagesOPEC+ Production Cut Impact on Oil Prices & MarketRG MoPNGNo ratings yet

- Oil downstream outlook to 2035: Product demand trends and implications for refining capacityDocument98 pagesOil downstream outlook to 2035: Product demand trends and implications for refining capacitygirishrajsNo ratings yet

- Meeting 2 Oil and Gas TodayDocument4 pagesMeeting 2 Oil and Gas TodayzllsNo ratings yet

- Oil ScarcityDocument2 pagesOil ScarcityAngel ZainabNo ratings yet

- ADL BaseOilDocument4 pagesADL BaseOilhazmijemiNo ratings yet

- 02pa MK 3 5 PDFDocument11 pages02pa MK 3 5 PDFMarcelo Varejão CasarinNo ratings yet

- Dissertation Oil PricesDocument4 pagesDissertation Oil PricesDoMyCollegePaperForMeColumbia100% (1)

- Financing The World Petroleum Industry A Talk by John D. Emerson Chase Bank, New YorkDocument24 pagesFinancing The World Petroleum Industry A Talk by John D. Emerson Chase Bank, New YorkIbrahim SalahudinNo ratings yet

- R.Lakshmi Anvitha (1226213102) : Green TechnologiesDocument8 pagesR.Lakshmi Anvitha (1226213102) : Green TechnologiesTejeesh Chandra PonnagantiNo ratings yet

- Sprott On OilDocument10 pagesSprott On OilMariusz Skonieczny100% (1)

- Ecbwp1855 en PDFDocument34 pagesEcbwp1855 en PDFAmrNo ratings yet

- Declining Oil Rev NigeriaDocument12 pagesDeclining Oil Rev NigeriaAltay KalpakNo ratings yet

- Macro Factors Key Oil & Gas PricesDocument9 pagesMacro Factors Key Oil & Gas Prices10manbearpig01No ratings yet

- WOO Boxes World Economy Oil PricesDocument3 pagesWOO Boxes World Economy Oil PricesمسعودNo ratings yet

- ExxonMobil Analysis ReportDocument18 pagesExxonMobil Analysis Reportaaldrak100% (2)

- Shale Oil and EffectsDocument20 pagesShale Oil and EffectsDag AlpNo ratings yet

- The Oil Market 2030Document12 pagesThe Oil Market 2030Arjun GuglaniNo ratings yet

- UOP Hydroprocessing Innovations Supplement TechDocument0 pagesUOP Hydroprocessing Innovations Supplement Techasrahaman9100% (1)

- Research Paper Oil PricesDocument5 pagesResearch Paper Oil Pricesfvfr9cg8100% (1)

- Oil Prices Term PaperDocument5 pagesOil Prices Term Papereeyjzkwgf100% (1)

- World Energy Outlook: Executive SummaryDocument10 pagesWorld Energy Outlook: Executive SummaryJean Noel Stephano TencaramadonNo ratings yet

- IndiaDocument11 pagesIndiaMd Riz ZamaNo ratings yet

- Research Paper - Oil Crisis in The 21ST CenturyDocument6 pagesResearch Paper - Oil Crisis in The 21ST CenturyAdil VasudevaNo ratings yet

- Impact of Oil Price Shocks on Nigeria's MacroeconomyDocument11 pagesImpact of Oil Price Shocks on Nigeria's MacroeconomyDiamante GomezNo ratings yet

- SPE-191766-MS Assessment of Petroleum Sensitive Countries Economic Reforms in Reaction To Fluctuating Oil PricesDocument13 pagesSPE-191766-MS Assessment of Petroleum Sensitive Countries Economic Reforms in Reaction To Fluctuating Oil PricesGabriel SNo ratings yet

- Risk of Majors Underinvesting in Oil and Gas Is RealDocument7 pagesRisk of Majors Underinvesting in Oil and Gas Is RealNguyễn Khánh Tùng K58No ratings yet

- Covid19 - Submission - AishaCinintya - Liverpool John Moores UniversityDocument10 pagesCovid19 - Submission - AishaCinintya - Liverpool John Moores UniversityCindy Cinintya Aisha CinintyaNo ratings yet

- Oil Price DissertationDocument7 pagesOil Price DissertationDoMyPaperForMeUK100% (1)

- The Shift in Global Crude Oil Market Structure: A Model-Based Analysis of The Period 2013-2017Document39 pagesThe Shift in Global Crude Oil Market Structure: A Model-Based Analysis of The Period 2013-2017The Panda EntertainerNo ratings yet

- 2016 CJC Econs PrelimDocument34 pages2016 CJC Econs PrelimDavid LimNo ratings yet

- West African Monetary Agency (WAMA)Document63 pagesWest African Monetary Agency (WAMA)bimpiziNo ratings yet

- Thesis About Oil Price HikeDocument8 pagesThesis About Oil Price Hikepamelacalusonewark100% (1)

- Rise and fall of black gold: Reasons and impact on global economyDocument5 pagesRise and fall of black gold: Reasons and impact on global economyPhalguni AnejaNo ratings yet

- Qatar Issue DiscussionDocument25 pagesQatar Issue DiscussionAwais BhattiNo ratings yet

- Is The Oil Industry Able To Support A World That Consumes 105 Million Barrels of Oil Per Day in 2025? - Oil & Gas Science and Technology (Hacquard, 2019)Document11 pagesIs The Oil Industry Able To Support A World That Consumes 105 Million Barrels of Oil Per Day in 2025? - Oil & Gas Science and Technology (Hacquard, 2019)CliffhangerNo ratings yet

- Aaaaaaaaaaaaaaaa A Aaa A Aaaaaaaaaaaa Aa A Aa A Aa Aaa A A A ADocument3 pagesAaaaaaaaaaaaaaaa A Aaa A Aaaaaaaaaaaa Aa A Aa A Aa Aaa A A A AM Kashif RazaNo ratings yet

- Energy Transition and PetrostateDocument5 pagesEnergy Transition and PetrostateDanielNo ratings yet

- Effects of Higher Oil PricesDocument7 pagesEffects of Higher Oil PricesLulav BarwaryNo ratings yet

- Order 137543098Document9 pagesOrder 137543098PETER KAMOTHONo ratings yet

- 2020 Oil, Gas, and Chemical Industry OutlookDocument16 pages2020 Oil, Gas, and Chemical Industry OutlookmapstonegardensNo ratings yet

- Task 2 - ImplementationDocument6 pagesTask 2 - ImplementationIndianagrofarmsNo ratings yet

- Gasoline Prices PrimerDocument17 pagesGasoline Prices PrimerEnergy Tomorrow50% (2)

- Fossil Fuel Supply Paper Analyzes Role of TechnologyDocument12 pagesFossil Fuel Supply Paper Analyzes Role of TechnologyAhmad Kurnia Paramasatya100% (1)

- Academic Research Essay On Oil Prices: Prakhar GuptaDocument13 pagesAcademic Research Essay On Oil Prices: Prakhar GuptaPrakhar GuptaNo ratings yet

- Translate Buk EkaDocument6 pagesTranslate Buk EkadelviNo ratings yet

- Case SummaryDocument6 pagesCase SummaryMohamed IbrahimNo ratings yet

- Petroleum Economics Assignemnt No.1Document3 pagesPetroleum Economics Assignemnt No.1Saad FaheemNo ratings yet

- WeekFiveAssignment FranciscoRiverosDocument3 pagesWeekFiveAssignment FranciscoRiverosfmriverNo ratings yet

- Why Deflation Is Good News For EuropeDocument2 pagesWhy Deflation Is Good News For EuropeRun ZhongNo ratings yet

- Determining Fuel Prices: The Cost of CrudeDocument2 pagesDetermining Fuel Prices: The Cost of CrudeSharania Udhaya KumarNo ratings yet

- New Situation and Challenges Involving World's Downstream Oil SectorDocument3 pagesNew Situation and Challenges Involving World's Downstream Oil SectorHadiBiesNo ratings yet

- Foundations of Energy Risk Management: An Overview of the Energy Sector and Its Physical and Financial MarketsFrom EverandFoundations of Energy Risk Management: An Overview of the Energy Sector and Its Physical and Financial MarketsNo ratings yet

- Energy Myths and Realities: Bringing Science to the Energy Policy DebateFrom EverandEnergy Myths and Realities: Bringing Science to the Energy Policy DebateRating: 4 out of 5 stars4/5 (4)

- DBD 2016 Stock Selection JAN 2016Document4 pagesDBD 2016 Stock Selection JAN 2016Bruno Dias da CostaNo ratings yet

- ETF Portfolio Details - Saxo Bank - Balanced Portfolio Description 2013Document8 pagesETF Portfolio Details - Saxo Bank - Balanced Portfolio Description 2013Bruno Dias da CostaNo ratings yet

- Euronext ETF Brochure 2015Document2 pagesEuronext ETF Brochure 2015Bruno Dias da CostaNo ratings yet

- Concept of FX - Exposure & Margin RequirementDocument1 pageConcept of FX - Exposure & Margin RequirementBruno Dias da CostaNo ratings yet

- Oil Price Outlook (Jun10)Document14 pagesOil Price Outlook (Jun10)hasantonmoyNo ratings yet

- Gs Usd Break Out ?Document11 pagesGs Usd Break Out ?Bruno Dias da CostaNo ratings yet

- GREECE: Who Will Bail Out Insolvent Greek Banks? DBD Strategy 27.01.2015Document6 pagesGREECE: Who Will Bail Out Insolvent Greek Banks? DBD Strategy 27.01.2015Bruno Dias da CostaNo ratings yet

- Adjusting in The Euro Area: The Case of Portugal (Trinity College Dublin April 11th, 2013)Document48 pagesAdjusting in The Euro Area: The Case of Portugal (Trinity College Dublin April 11th, 2013)Bruno Dias da CostaNo ratings yet

- Consul To Rio Do Invest Id or - Bruno Costa - 17.9Document1 pageConsul To Rio Do Invest Id or - Bruno Costa - 17.9Bruno Dias da CostaNo ratings yet

- World Scale BasicDocument2 pagesWorld Scale BasicD.Muruganand100% (1)

- Davey Brothers Watch Co.: The Case For LearningDocument4 pagesDavey Brothers Watch Co.: The Case For Learningyashashree barhateNo ratings yet

- Argus DeWitt PolymersDocument9 pagesArgus DeWitt Polymersdrmohamed120No ratings yet

- IELTS MONEY VocabularyDocument4 pagesIELTS MONEY VocabularyVera ErastovaNo ratings yet

- H2 Econs SyllabusDocument13 pagesH2 Econs SyllabusJoel OngNo ratings yet

- Product ModificationDocument2 pagesProduct ModificationkocherlakotapavanNo ratings yet

- DEBERTINDocument427 pagesDEBERTINRizza Cabbuag100% (3)

- 17.dwitya - Aip-Prisma Assestment TestDocument8 pages17.dwitya - Aip-Prisma Assestment TestvytheNo ratings yet

- OTOP Goes Global - AnalysisDocument28 pagesOTOP Goes Global - AnalysisTu Binh ChauNo ratings yet

- Initial Public Offering (IPO)Document15 pagesInitial Public Offering (IPO)ackyriotsxNo ratings yet

- Internal and External Factors Affecting Foreign Market Management EssayDocument10 pagesInternal and External Factors Affecting Foreign Market Management EssaySanjeev Thakur100% (1)

- PAS 16 Property Plant and EquipmentDocument22 pagesPAS 16 Property Plant and EquipmentPatawaran, Janelle S.No ratings yet

- KFC Case Study by MR OtakuDocument36 pagesKFC Case Study by MR OtakuSajan Razzak Akon100% (1)

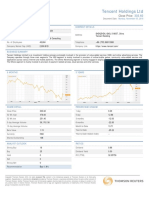

- Tencent Holdings LTD: Close PriceDocument2 pagesTencent Holdings LTD: Close PricetrungNo ratings yet

- ME Problem Set-7Document6 pagesME Problem Set-7Akshay UtkarshNo ratings yet

- The Textile and Apparel Industry in IndiaDocument12 pagesThe Textile and Apparel Industry in IndiaAmbika sharmaNo ratings yet

- Unit 3. Accounting For Merchandising BusinessesDocument9 pagesUnit 3. Accounting For Merchandising BusinessesAkkamaNo ratings yet

- Cost of Carry ModelDocument12 pagesCost of Carry Modeljyo23No ratings yet

- Homework Chapter Two: Overview of Process EconomicsDocument22 pagesHomework Chapter Two: Overview of Process EconomicsMateo Vanegas100% (1)

- ECO401 Economics 10 Midterm Solved Papers Subjective and Objective in For Exam Preparation Spring 2013Document0 pagesECO401 Economics 10 Midterm Solved Papers Subjective and Objective in For Exam Preparation Spring 2013Muhammad Ayub100% (1)

- Exercises On Stock ValuationDocument3 pagesExercises On Stock ValuationFatin FathihahNo ratings yet

- Quotation - ABS 2020-21 - E203 - Mr. K Ramesh ReddyDocument1 pageQuotation - ABS 2020-21 - E203 - Mr. K Ramesh ReddyairblisssolutionsNo ratings yet

- Midterm Exam-Ch 1-3 and CH 19-25 (Weight 20%) - Attempt ReviewDocument16 pagesMidterm Exam-Ch 1-3 and CH 19-25 (Weight 20%) - Attempt ReviewDipen ShahNo ratings yet

- Back of The Envelope - MathTestDocument6 pagesBack of The Envelope - MathTestDan KimNo ratings yet

- Midterm - Special ExamDocument2 pagesMidterm - Special ExamDhanica C. MabignayNo ratings yet

- Clatapult Quant TestDocument7 pagesClatapult Quant TestnabarunNo ratings yet

- Marketing Planning and Management Final AssessmentDocument36 pagesMarketing Planning and Management Final AssessmentCooper Luskan0% (1)

- Inventory Management, Just-in-Time, and Simplified Costing MethodsDocument43 pagesInventory Management, Just-in-Time, and Simplified Costing MethodsKarissa Rizka LNo ratings yet

- Maggi Brand's Successful Comeback in IndiaDocument35 pagesMaggi Brand's Successful Comeback in IndiaRakesh VishwakarmaNo ratings yet

- DI WORKSHOP: C2C MENTORS Mumbai | Pune | Online 9022342214Document4 pagesDI WORKSHOP: C2C MENTORS Mumbai | Pune | Online 9022342214Aravinth RameshNo ratings yet