You might also like

- New Yorkers in Need Poverty TrendsDocument44 pagesNew Yorkers in Need Poverty Trendsshughes080No ratings yet

- A Minimum Income Standard For The United Kingdom in 2021 0Document43 pagesA Minimum Income Standard For The United Kingdom in 2021 0Alex ButcherNo ratings yet

- Adams' People'S Plan:: Cash, Childcare & Housing Assistance-And A City That DeliversDocument3 pagesAdams' People'S Plan:: Cash, Childcare & Housing Assistance-And A City That DeliversEric Adams 2021No ratings yet

- SUPPORT ActDocument5 pagesSUPPORT ActMary Claire PattonNo ratings yet

- A Minimum Income Standard For The Uk in 2022Document53 pagesA Minimum Income Standard For The Uk in 2022cowbuttNo ratings yet

- Raising The Minimum WageDocument6 pagesRaising The Minimum WageJon CampbellNo ratings yet

- NYC Aid PlanDocument4 pagesNYC Aid PlanEric Adams 2021No ratings yet

- NYC Aid PlanDocument4 pagesNYC Aid PlanEric Adams 2021No ratings yet

- NYC Aid PlanDocument4 pagesNYC Aid PlanEric Adams 2021No ratings yet

- NYC Aid PlanDocument4 pagesNYC Aid PlanEric Adams 2021No ratings yet

- Ny Stimulus Talking Points FinalDocument5 pagesNy Stimulus Talking Points FinalCenter for Social InclusionNo ratings yet

- Hochul Housing Coalition Letter PrsDocument4 pagesHochul Housing Coalition Letter PrsNick ReismanNo ratings yet

- Universal Basic Income in India: A Policy AnalysisDocument3 pagesUniversal Basic Income in India: A Policy AnalysisARVIND MALLIKNo ratings yet

- Homeward DC Report FY 2021 2025Document61 pagesHomeward DC Report FY 2021 2025MariaNo ratings yet

- The Reader: Hundreds Rally For Affordable HousingDocument12 pagesThe Reader: Hundreds Rally For Affordable HousinganhdincNo ratings yet

- How financial inclusion reduces povertyDocument16 pagesHow financial inclusion reduces povertyKushagra AmritNo ratings yet

- "Examining The Administration's Failure To Prevent and End Medicaid Overpayments" Testimony Of: John Hagg Director of Medicaid AuditsDocument8 pages"Examining The Administration's Failure To Prevent and End Medicaid Overpayments" Testimony Of: John Hagg Director of Medicaid AuditsBeverly TranNo ratings yet

- The Reader: Finally Some Good News: HUD Announces 2010 Budget RequestDocument12 pagesThe Reader: Finally Some Good News: HUD Announces 2010 Budget RequestanhdincNo ratings yet

- 2020-21 Call LetterDocument2 pages2020-21 Call LetterNick ReismanNo ratings yet

- The Future of County Nursing Homes in New York State: August, 2013Document162 pagesThe Future of County Nursing Homes in New York State: August, 2013jspectorNo ratings yet

- Technology For Aging: 2021 Market OverviewDocument24 pagesTechnology For Aging: 2021 Market OverviewparsadNo ratings yet

- New York at A Crossroads: A Transformation Plan For A New New YorkDocument31 pagesNew York at A Crossroads: A Transformation Plan For A New New YorkwqwerNo ratings yet

- 2022 Personal Finance Statistics: 34% Feel Financially Healthy as Costs RiseDocument15 pages2022 Personal Finance Statistics: 34% Feel Financially Healthy as Costs RiseMasab AsifNo ratings yet

- Hud NewsDocument3 pagesHud Newsapi-142821947No ratings yet

- Household Debt ThesisDocument6 pagesHousehold Debt Thesismoz1selajuk2100% (2)

- Highlights of The Enacted Fy 2020-2021 New York State BudgetDocument4 pagesHighlights of The Enacted Fy 2020-2021 New York State BudgetNew York SenateNo ratings yet

- See Chapter 20 of 48 U.S. CodeDocument4 pagesSee Chapter 20 of 48 U.S. CodeMetro Puerto RicoNo ratings yet

- 2015 2016 FPI Briefing Book 1.0Document72 pages2015 2016 FPI Briefing Book 1.0Casey SeilerNo ratings yet

- Affordable Housing Position PaperDocument4 pagesAffordable Housing Position PaperDrew AstolfiNo ratings yet

- Fiscal Committees Taxes Kink Testimony 02.07.17 FinalDocument10 pagesFiscal Committees Taxes Kink Testimony 02.07.17 FinalMichael KinkNo ratings yet

- NextGeneration NYCHADocument117 pagesNextGeneration NYCHAMichael Gareth JohnsonNo ratings yet

- Order ID - 3619865Document9 pagesOrder ID - 3619865MosesNo ratings yet

- Newyork 2020 Agenda AttachmentDocument8 pagesNewyork 2020 Agenda AttachmentjspectorNo ratings yet

- Highlights of The Enacted Fy 2020-2021 New York State BudgetDocument4 pagesHighlights of The Enacted Fy 2020-2021 New York State BudgetNew York SenateNo ratings yet

- Grant Systemic PaperDocument7 pagesGrant Systemic Paperapi-733876438No ratings yet

- Affordable Financial Services and Credit For The Poor: The Foundation of Asset BuildingDocument17 pagesAffordable Financial Services and Credit For The Poor: The Foundation of Asset BuildingYahoo SeriousNo ratings yet

- One New York, Rising TogetherDocument75 pagesOne New York, Rising TogetherNew Yorkers for de BlasioNo ratings yet

- Fairness Fees PaperDocument8 pagesFairness Fees PaperRachel SilbersteinNo ratings yet

- Foreclosure 11211Document8 pagesForeclosure 11211Nick ReismanNo ratings yet

- ACORN Canada: Federal Peoples PlatformDocument6 pagesACORN Canada: Federal Peoples PlatformACORN_CanadaNo ratings yet

- Bill de Blasio - One New York Rising TogetherDocument75 pagesBill de Blasio - One New York Rising TogetherStefano AmbrosiniNo ratings yet

- EntitlementsDocument4 pagesEntitlementsRichard HortonNo ratings yet

- Data Update: Eviction Filings in NYC Since COVID-19Document12 pagesData Update: Eviction Filings in NYC Since COVID-19Roosevelt ColumbiaNo ratings yet

- Testimony of Christine C. Quinn, Speaker, New York City Council On The Governor's Executive Budget For State Fiscal Year 2011-2012Document4 pagesTestimony of Christine C. Quinn, Speaker, New York City Council On The Governor's Executive Budget For State Fiscal Year 2011-2012NYCCouncilNo ratings yet

- Facts and FiguresDocument14 pagesFacts and FiguresJude Ruel MoraldeNo ratings yet

- Plan C - Slow Growth and Public Service ReformDocument12 pagesPlan C - Slow Growth and Public Service ReformThe RSANo ratings yet

- The Price of Income Security in Older Age: Cost of A Universal Pension in 50 Low - and Middle-Income Countries.Document8 pagesThe Price of Income Security in Older Age: Cost of A Universal Pension in 50 Low - and Middle-Income Countries.HelpAge InternationalNo ratings yet

- Households in Connecticut That RentDocument4 pagesHouseholds in Connecticut That RentABoyd8No ratings yet

- Reverse Mortgage - The Emerging Financial Product - An EvaluationDocument8 pagesReverse Mortgage - The Emerging Financial Product - An EvaluationSahil WadhwaNo ratings yet

- Private Investors Can Help End Poverty. They Just Need To Think Small and LocalDocument6 pagesPrivate Investors Can Help End Poverty. They Just Need To Think Small and LocalGhaliNo ratings yet

- The Affordable Care Act and New Yorkers: The Gift That Keeps On GivingDocument22 pagesThe Affordable Care Act and New Yorkers: The Gift That Keeps On GivingPublic Policy and Education Fund of NYNo ratings yet

- Bond Standard 09Document4 pagesBond Standard 09Social IMPACT Research Center at Heartland Alliance for Human Needs and Human RightsNo ratings yet

- Int 0168-2010: Collecting and Reporting Data Related To Youth Aging Out of Foster CareDocument10 pagesInt 0168-2010: Collecting and Reporting Data Related To Youth Aging Out of Foster CareBill de BlasioNo ratings yet

- Self-Sufficiency in Dewitt County, IllinoisDocument4 pagesSelf-Sufficiency in Dewitt County, IllinoisSocial IMPACT Research Center at Heartland Alliance for Human Needs and Human RightsNo ratings yet

- Affordable Housing and Homelessness Package CSAC CWDA UCC 3.15.18Document5 pagesAffordable Housing and Homelessness Package CSAC CWDA UCC 3.15.18alishaNo ratings yet

- A Proud Progressive New York or A Declining Empire State?Document4 pagesA Proud Progressive New York or A Declining Empire State?Citizen Action of New YorkNo ratings yet

- Self-Sufficiency in Mcdonough County, IllinoisDocument4 pagesSelf-Sufficiency in Mcdonough County, IllinoisSocial IMPACT Research Center at Heartland Alliance for Human Needs and Human RightsNo ratings yet

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorNo ratings yet

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorNo ratings yet

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- State Health CoverageDocument26 pagesState Health CoveragejspectorNo ratings yet

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinNo ratings yet

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNo ratings yet

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorNo ratings yet

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsNo ratings yet

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorNo ratings yet

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorNo ratings yet

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorNo ratings yet

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyNo ratings yet

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinNo ratings yet

- Class of 2022Document1 pageClass of 2022jspectorNo ratings yet

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorNo ratings yet

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanNo ratings yet

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorNo ratings yet

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorNo ratings yet

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNo ratings yet

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonNo ratings yet

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorNo ratings yet

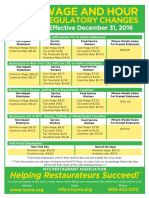

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorNo ratings yet

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNo ratings yet

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanNo ratings yet

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorNo ratings yet

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorNo ratings yet

- Voting Report CardDocument1 pageVoting Report CardjspectorNo ratings yet

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorNo ratings yet

- Construction in Saudi Arabia - Marketline - June 2022Document41 pagesConstruction in Saudi Arabia - Marketline - June 2022Chhaya DhawanNo ratings yet

- Artspace Preliminary Feasibility ReportDocument31 pagesArtspace Preliminary Feasibility ReportSarasotaObserverNo ratings yet

- Enterprise - Impact of Affordable Housing On Families and Communities PDFDocument20 pagesEnterprise - Impact of Affordable Housing On Families and Communities PDFCedric ZhouNo ratings yet

- Guidelines Social HousingDocument109 pagesGuidelines Social Housingtomi_penzesNo ratings yet

- The Hope Mill (Scituate, RI) - Slightly Updated (Sept. 2016)Document12 pagesThe Hope Mill (Scituate, RI) - Slightly Updated (Sept. 2016)Remington Veritas Praevalebit100% (3)

- ECON E-1700, Urban Policy Syllabus, Fall Term 2017 V2 CarrasDocument10 pagesECON E-1700, Urban Policy Syllabus, Fall Term 2017 V2 CarrasPrameet GuptaNo ratings yet

- SIADS 592 Affordable HousingDocument27 pagesSIADS 592 Affordable HousinggeorgethioNo ratings yet

- PerryUndem Research Communication Black American Survey ReportDocument67 pagesPerryUndem Research Communication Black American Survey ReportKERANewsNo ratings yet

- India Strategy (Housing Boom Ahead) 20170428Document156 pagesIndia Strategy (Housing Boom Ahead) 20170428Ronak JajooNo ratings yet

- PCH Media KitDocument9 pagesPCH Media KitSophie O'RourkeNo ratings yet

- The Sustainable Development Goals, Targets and Indicators: Philippine Statistics AuthorityDocument67 pagesThe Sustainable Development Goals, Targets and Indicators: Philippine Statistics AuthorityTiffanny Diane Agbayani RuedasNo ratings yet

- Construction in Ethiopia PDFDocument7 pagesConstruction in Ethiopia PDFMaekINo ratings yet

- 421-A: Affordable New York Page Sept. 2019Document5 pages421-A: Affordable New York Page Sept. 2019Norman OderNo ratings yet

- Assessing Residents' Level of Acceptance of Agropolitan Social Housing Development For The Greater Port Harcourt City, Rivers State, NigeriaDocument14 pagesAssessing Residents' Level of Acceptance of Agropolitan Social Housing Development For The Greater Port Harcourt City, Rivers State, NigeriaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- ToR Rental Markets in TanzaniaDocument11 pagesToR Rental Markets in TanzaniaAnonymous FnM14a0No ratings yet

- Homes For Our Old Age PDFDocument40 pagesHomes For Our Old Age PDFCJ OngNo ratings yet

- Community Land Trusts: A Radical or Reformist Response To The Housing Question Today?Document26 pagesCommunity Land Trusts: A Radical or Reformist Response To The Housing Question Today?AlanNo ratings yet

- The Way HomeDocument248 pagesThe Way Homethedoefund100% (1)

- Unfairbnb - How Online Rental Platforms Use The EU To Defeat Cities' Affordable Housing MeasuresDocument28 pagesUnfairbnb - How Online Rental Platforms Use The EU To Defeat Cities' Affordable Housing MeasuresTatiana100% (1)

- Real Estate Sector - FinalDocument73 pagesReal Estate Sector - FinalHarshit GargNo ratings yet

- The Economic Impact of Livable Communities: Indiana Association For Community Economic DevelopmentDocument50 pagesThe Economic Impact of Livable Communities: Indiana Association For Community Economic Developmentgovindaraj sNo ratings yet

- Planyc 2011 Planyc Full Report PDFDocument202 pagesPlanyc 2011 Planyc Full Report PDFramon perezNo ratings yet

- EMIS Insights - India Real Estate Sector Report 2020-2024Document104 pagesEMIS Insights - India Real Estate Sector Report 2020-2024tushar2308No ratings yet

- Housing Our Future - LISC Cincinnati Report May 2020 (12283)Document28 pagesHousing Our Future - LISC Cincinnati Report May 2020 (12283)WVXU NewsNo ratings yet

- City Limits Magazine, April 1998 IssueDocument40 pagesCity Limits Magazine, April 1998 IssueCity Limits (New York)No ratings yet

- Dissertation On Affordable Urban HousingDocument76 pagesDissertation On Affordable Urban HousingANSHIKA SINGH100% (2)

- Group6 Deetey SalonDocument17 pagesGroup6 Deetey SalonRachel Jane TanNo ratings yet

- State System of Higher Education Funding RequestDocument10 pagesState System of Higher Education Funding RequestPennLiveNo ratings yet

- Implementation Plan - Kigali Master Plan 2050Document130 pagesImplementation Plan - Kigali Master Plan 2050Lego EdrisaNo ratings yet

- 9.chapter 06 PDFDocument18 pages9.chapter 06 PDFIshrahaNo ratings yet