You might also like

- 127 Scra 9 (GR 119761) Commisioner vs. CADocument23 pages127 Scra 9 (GR 119761) Commisioner vs. CARuel FernandezNo ratings yet

- Admin Law CasesDocument54 pagesAdmin Law CasesMarie CecileNo ratings yet

- CIR v. FortuneDocument5 pagesCIR v. FortuneFay GurreaNo ratings yet

- Supreme Court Upholds CTA Decision Canceling Tax Assessment on Fortune TobaccoDocument40 pagesSupreme Court Upholds CTA Decision Canceling Tax Assessment on Fortune Tobaccomfdcabangon4009No ratings yet

- Tax CIR v. CTA and Fortune TobaccoDocument8 pagesTax CIR v. CTA and Fortune TobaccoClaire RoxasNo ratings yet

- CIR Vs CA 1996Document11 pagesCIR Vs CA 1996Janette SumagaysayNo ratings yet

- Court Affirms CTA Ruling on Cigarette Tax ClassificationDocument7 pagesCourt Affirms CTA Ruling on Cigarette Tax ClassificationClaudine Christine A. VicenteNo ratings yet

- CIR vs. CA - Fortune Tobacco Corp., G.R. No. 119761, August 29, 1996Document29 pagesCIR vs. CA - Fortune Tobacco Corp., G.R. No. 119761, August 29, 1996Jellie Grace CañeteNo ratings yet

- CIR Vs Fortune TobaccoDocument27 pagesCIR Vs Fortune TobaccoPoPo MillanNo ratings yet

- CIR Vs CA and Fortune Tobacco CorpDocument8 pagesCIR Vs CA and Fortune Tobacco CorpPrincess Ruksan Lawi SucorNo ratings yet

- Commissioner OF Internal REVENUE, Petitioner, vs. HON. Court of Appeals, Hon. Court of Tax Appeals and Fortune Tobacco Corporation, RespondentsDocument8 pagesCommissioner OF Internal REVENUE, Petitioner, vs. HON. Court of Appeals, Hon. Court of Tax Appeals and Fortune Tobacco Corporation, Respondentsecinue guirreisaNo ratings yet

- Administrative LawDocument30 pagesAdministrative LawJulieNo ratings yet

- Remedies Week 1 CasesDocument320 pagesRemedies Week 1 CasesA GrafiloNo ratings yet

- 3.2 Commissioner V CADocument8 pages3.2 Commissioner V CAJayNo ratings yet

- 261 SCRA 236 Commissioner of Internal Revenue Vs CA 1996Document31 pages261 SCRA 236 Commissioner of Internal Revenue Vs CA 1996Panda CatNo ratings yet

- Admin Law 3Document128 pagesAdmin Law 3rheyneNo ratings yet

- 261 SCRA 236 Commissioner of Internal Revenue Vs CA 1996Document31 pages261 SCRA 236 Commissioner of Internal Revenue Vs CA 1996Samiha TorrecampoNo ratings yet

- CIR V CA, 301 SCRA 152Document21 pagesCIR V CA, 301 SCRA 152Marge OstanNo ratings yet

- Commissioner Vs CA DigestDocument2 pagesCommissioner Vs CA DigestKaye TolentinoNo ratings yet

- 9 CIR vs. HON. COURT OF APPEALS, HON. COURT OF TAX APPEALS and FORTUNE TOBACCO CORPORATIONDocument2 pages9 CIR vs. HON. COURT OF APPEALS, HON. COURT OF TAX APPEALS and FORTUNE TOBACCO CORPORATIONkrizzledelapenaNo ratings yet

- Commissioner of Internal Revenue vs. CADocument2 pagesCommissioner of Internal Revenue vs. CAKristine JoyNo ratings yet

- Administrative LawDocument2 pagesAdministrative LawAmbra Kaye AriolaNo ratings yet

- ACFrOgAsT0vmVoKoA6mQH4l - Yp GHUEdQTcdUSOiyoINiO61Tn8 g6OhStpSeXShXabwLHuQhnVD7xluiMcbEn7Nk Wk4N - o56SPcAoepCIvpnkM7OdbkI3qxptC2fUDocument2 pagesACFrOgAsT0vmVoKoA6mQH4l - Yp GHUEdQTcdUSOiyoINiO61Tn8 g6OhStpSeXShXabwLHuQhnVD7xluiMcbEn7Nk Wk4N - o56SPcAoepCIvpnkM7OdbkI3qxptC2fUChristina AureNo ratings yet

- Tax 2nd WeekDocument12 pagesTax 2nd WeekLester BalagotNo ratings yet

- Commissioner of Internal Revenue V CaDocument3 pagesCommissioner of Internal Revenue V CaJimenez LorenzNo ratings yet

- Commissioner of Internal Revenue v. Court of AppealsDocument2 pagesCommissioner of Internal Revenue v. Court of AppealsLance Lagman100% (1)

- BIR Authority to Increase Tax Rates via Circular ChallengedDocument1 pageBIR Authority to Increase Tax Rates via Circular ChallengedEbbe DyNo ratings yet

- Chapter IV Excise Tax on Tobacco ProductsDocument45 pagesChapter IV Excise Tax on Tobacco ProductsZhee BillarinaNo ratings yet

- Commissioner of Customs VDocument16 pagesCommissioner of Customs VJefferson NunezaNo ratings yet

- The Case of 125346Document2 pagesThe Case of 125346markuslagan06No ratings yet

- La Suerte Cigar Vs CADocument24 pagesLa Suerte Cigar Vs CAHenry LNo ratings yet

- British American Tobacco v. Camacho, 562 SCRA 511 (2008)Document26 pagesBritish American Tobacco v. Camacho, 562 SCRA 511 (2008)Christiaan CastilloNo ratings yet

- 6 Eastern Telecom vs. ICC Case DigestDocument3 pages6 Eastern Telecom vs. ICC Case DigestJaja GkNo ratings yet

- Supreme Court Rules on VAT Rate Hike DelegationDocument16 pagesSupreme Court Rules on VAT Rate Hike DelegationEdward Kenneth KungNo ratings yet

- British American Tobacco vs. CamachoDocument1 pageBritish American Tobacco vs. CamachoRaquel DoqueniaNo ratings yet

- Topic-Powers of CirDocument169 pagesTopic-Powers of CirLGU PadadaNo ratings yet

- 2016-10688 Requirements For Submission of User FeesDocument10 pages2016-10688 Requirements For Submission of User FeesBarrySteinNo ratings yet

- CIR v. FortuneDocument2 pagesCIR v. FortunedelayinggratificationNo ratings yet

- 3.1 Commissioner V CA, Lucio TanDocument41 pages3.1 Commissioner V CA, Lucio TanJayNo ratings yet

- TAXATION CASESDocument23 pagesTAXATION CASESchiclets777100% (2)

- C Irv CT A and Fortune TobaccoDocument2 pagesC Irv CT A and Fortune TobaccoErika AlidioNo ratings yet

- Constitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL ExclusiveDocument34 pagesConstitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL ExclusiveEmerson NunezNo ratings yet

- DRAFT CONTRACT - SugarIC45Document15 pagesDRAFT CONTRACT - SugarIC45Ricardo Flores CampolloNo ratings yet

- Far East Bank Appeals Tax Refund DenialDocument54 pagesFar East Bank Appeals Tax Refund DenialDaryll Phoebe EbreoNo ratings yet

- La Suerte v. CaDocument2 pagesLa Suerte v. CaLuna BaciNo ratings yet

- CIR V Puregold 760 SCRA 96Document12 pagesCIR V Puregold 760 SCRA 96Karen Joy MasapolNo ratings yet

- Case 8Document6 pagesCase 8CMariaNo ratings yet

- The question of sufficiency of petitioner’s evidence to support its claim for tax refundDocument8 pagesThe question of sufficiency of petitioner’s evidence to support its claim for tax refundGraile Dela CruzNo ratings yet

- CIR v. Hon. CA, CTA and Fortune Tobacco CorpDocument2 pagesCIR v. Hon. CA, CTA and Fortune Tobacco CorpEdvangelineManaloRodriguezNo ratings yet

- BTC vs. Camacho, G.R. No. 163583 (2008)Document26 pagesBTC vs. Camacho, G.R. No. 163583 (2008)Aaron James PuasoNo ratings yet

- Case DigestDocument65 pagesCase DigestFord OsipNo ratings yet

- Tax Cases 2Document146 pagesTax Cases 2Sylver JanNo ratings yet

- Jalandoni & Jamir For Petitioner. Officer of The Solicitor General For RespondentsDocument2 pagesJalandoni & Jamir For Petitioner. Officer of The Solicitor General For RespondentsCarmel LouiseNo ratings yet

- Rational Basis Test Upholds Tax Classification FreezeDocument6 pagesRational Basis Test Upholds Tax Classification FreezeAntonio Rebosa100% (1)

- Philippines Vice Control Laws SummaryDocument20 pagesPhilippines Vice Control Laws SummarymyndleNo ratings yet

- Petitioner vs. vs. Respondents Clarence J. Villanueva The Government Corporate CounselDocument6 pagesPetitioner vs. vs. Respondents Clarence J. Villanueva The Government Corporate CounselLucio GeorgioNo ratings yet

- Alliance Tobacco Corp. Inc. v. PhilippineDocument6 pagesAlliance Tobacco Corp. Inc. v. PhilippineShiela PilarNo ratings yet

- How to Exercise Statutory Powers Properly: Cayman Islands Administrative LawFrom EverandHow to Exercise Statutory Powers Properly: Cayman Islands Administrative LawNo ratings yet

- PD 442 Labor Code Article 95. Right To Service Incentive LeaveDocument6 pagesPD 442 Labor Code Article 95. Right To Service Incentive LeaveMenchie Ann Sabandal SalinasNo ratings yet

- Affidavit of Loss-Official ReceiptDocument1 pageAffidavit of Loss-Official ReceiptMenchie Ann Sabandal Salinas100% (1)

- SRRV Information 2.0Document4 pagesSRRV Information 2.0Menchie Ann Sabandal SalinasNo ratings yet

- Revised PRA Remittance Instruction Form 1Document1 pageRevised PRA Remittance Instruction Form 1Menchie Ann Sabandal SalinasNo ratings yet

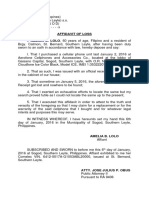

- Affidavit of Loss BCCI PassbookDocument1 pageAffidavit of Loss BCCI PassbookMenchie Ann Sabandal SalinasNo ratings yet

- Affidavit of Loss - OR OnlyDocument1 pageAffidavit of Loss - OR OnlyMenchie Ann Sabandal SalinasNo ratings yet

- San Roque Elementary School Weekly Home Learning Plan Grade 5Document1 pageSan Roque Elementary School Weekly Home Learning Plan Grade 5Menchie Ann Sabandal SalinasNo ratings yet

- Primers by Atty. OcjDocument33 pagesPrimers by Atty. OcjMenchie Ann Sabandal SalinasNo ratings yet

- CONSOLIDATED PUBLIC ATTORNEY%u2019S OFFICE LEGAL FORMS v1 - 0Document196 pagesCONSOLIDATED PUBLIC ATTORNEY%u2019S OFFICE LEGAL FORMS v1 - 0ErrolJohnFaminianoFopalanNo ratings yet

- Affidavit of Loss-Driver's LicenseDocument1 pageAffidavit of Loss-Driver's LicenseMenchie Ann Sabandal Salinas100% (1)

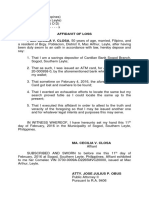

- Affidavit of Loss-ATMDocument1 pageAffidavit of Loss-ATMMenchie Ann Sabandal SalinasNo ratings yet

- Special Power of Attorney for Real EstateDocument2 pagesSpecial Power of Attorney for Real EstateMenchie Ann Sabandal Salinas100% (1)

- DEED OF SALE OF MOTOR VEHICLE-templateDocument2 pagesDEED OF SALE OF MOTOR VEHICLE-templateIvy Mallari QuintoNo ratings yet

- Affidavit of Loss - PassportDocument1 pageAffidavit of Loss - PassportMenchie Ann Sabandal SalinasNo ratings yet

- Affidavit of Loss-Driver' LicenseDocument1 pageAffidavit of Loss-Driver' LicenseMenchie Ann Sabandal SalinasNo ratings yet

- Affidavit of Loss-Health CardDocument1 pageAffidavit of Loss-Health CardMenchie Ann Sabandal SalinasNo ratings yet

- 0619-E Jan 2018 Rev Final PDFDocument1 page0619-E Jan 2018 Rev Final PDFMebelyn NavarraNo ratings yet

- Affidavit of Lost Official Receipt for Cellphone PurchaseDocument1 pageAffidavit of Lost Official Receipt for Cellphone PurchaseMenchie Ann Sabandal Salinas50% (2)

- Deed of Donation FormsDocument5 pagesDeed of Donation FormsJecky Delos Reyes100% (1)

- Form 1600Document4 pagesForm 1600KialicBetito50% (2)

- Affidavit For Request Transfer of BIR TinDocument1 pageAffidavit For Request Transfer of BIR TinMenchie Ann Sabandal SalinasNo ratings yet

- Dante Arana-Authorization LetterDocument1 pageDante Arana-Authorization LetterMenchie Ann Sabandal SalinasNo ratings yet

- Affidavit of Undertaking - Case of Other Light ThreatsDocument1 pageAffidavit of Undertaking - Case of Other Light ThreatsMenchie Ann Sabandal Salinas100% (1)

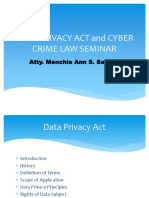

- Data Privacy Act and Cyber Crime Law Seminar: Atty. Menchie Ann S. SalinasDocument2 pagesData Privacy Act and Cyber Crime Law Seminar: Atty. Menchie Ann S. SalinasMenchie Ann Sabandal SalinasNo ratings yet

- Form 19 Indemnity Agreement Ver 2015.0Document2 pagesForm 19 Indemnity Agreement Ver 2015.0Menchie Ann Sabandal SalinasNo ratings yet

- Manual On PCC Chapter 9Document33 pagesManual On PCC Chapter 9Abraham JunioNo ratings yet

- Maintaining Affidavit IntegrityDocument6 pagesMaintaining Affidavit Integritydoctorfingertips8529No ratings yet

- CONSOLIDATED PUBLIC ATTORNEY%u2019S OFFICE LEGAL FORMS v1 - 0Document196 pagesCONSOLIDATED PUBLIC ATTORNEY%u2019S OFFICE LEGAL FORMS v1 - 0ErrolJohnFaminianoFopalanNo ratings yet

- Sample Format of Judicial Affidavit (English)Document6 pagesSample Format of Judicial Affidavit (English)Samantha BugayNo ratings yet

- Affidavit: Attorney For PlaintiffDocument1 pageAffidavit: Attorney For PlaintiffMenchie Ann Sabandal SalinasNo ratings yet

- Fundamental Provisions of Decree under CPCDocument22 pagesFundamental Provisions of Decree under CPCaniket sachanNo ratings yet

- Assignments and Delegations: Chapter19: Third-Party Rights To ContractsDocument13 pagesAssignments and Delegations: Chapter19: Third-Party Rights To ContractsAyako BrightNo ratings yet

- Minnesota Judicial Training Update: "Judicial Landmines" 20 Common Mistakes Every Judge Should AvoidDocument6 pagesMinnesota Judicial Training Update: "Judicial Landmines" 20 Common Mistakes Every Judge Should AvoidNhu Mai NguyenNo ratings yet

- SCRA Reyes v. MauricioDocument12 pagesSCRA Reyes v. Mauriciogoma21No ratings yet

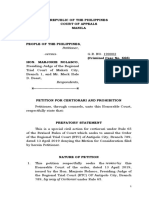

- Petition For Certiorari - Prosecution (Petitioner)Document9 pagesPetition For Certiorari - Prosecution (Petitioner)Andrew LastrolloNo ratings yet

- Jose Tan Chong Vs Secretary of Labor - September 16, 1947Document8 pagesJose Tan Chong Vs Secretary of Labor - September 16, 1947Lourd CellNo ratings yet

- Osmena Vs OsmenaDocument3 pagesOsmena Vs OsmenakimuchosNo ratings yet

- Case Note R. (Corner House)Document3 pagesCase Note R. (Corner House)Mark ChanNo ratings yet

- PD 957 JurisprudenceDocument28 pagesPD 957 JurisprudenceJay Ryan Sy BaylonNo ratings yet

- Tunis Gulic Campbell - Sufferings of The Rev. T. G. Campbell and His Family, in Georgia (1877)Document36 pagesTunis Gulic Campbell - Sufferings of The Rev. T. G. Campbell and His Family, in Georgia (1877)chyoungNo ratings yet

- Chua Vs San DiegoDocument25 pagesChua Vs San DiegoCarlo Vincent BalicasNo ratings yet

- Blank Mooting and Advocacy Skeleton ArgumentDocument2 pagesBlank Mooting and Advocacy Skeleton ArgumentChevanev Andrei CharlesNo ratings yet

- Meryll Lynch V CaDocument7 pagesMeryll Lynch V CaGabe BedanaNo ratings yet

- April 4, 2013 Mount Ayr Record-NewsDocument14 pagesApril 4, 2013 Mount Ayr Record-NewsMountAyrRecordNews0% (1)

- Farouk Abukar Vs People of The PhilippinesDocument39 pagesFarouk Abukar Vs People of The Philippineskristel jane caldozaNo ratings yet

- Taxation 1 Cases in Full TextDocument403 pagesTaxation 1 Cases in Full TextDominic M. CerbitoNo ratings yet

- 09 Manila Golf & Country Club v. IAC (1994)Document4 pages09 Manila Golf & Country Club v. IAC (1994)Zan BillonesNo ratings yet

- Florida Fish and Wildlife Conservation Comm'n v. Daws, No. 1D16-4839 (Fla. Dist. Ct. App. Apr. 10, 2018)Document27 pagesFlorida Fish and Wildlife Conservation Comm'n v. Daws, No. 1D16-4839 (Fla. Dist. Ct. App. Apr. 10, 2018)RHTNo ratings yet

- Filipinas Colleges Inc V TimbangDocument2 pagesFilipinas Colleges Inc V TimbangKR ReborosoNo ratings yet

- LocGov Cases 55-75 Plus Additional SobejanaDocument224 pagesLocGov Cases 55-75 Plus Additional SobejanaCarla MapaloNo ratings yet

- Class Xi Polsc WRKSHTDocument3 pagesClass Xi Polsc WRKSHTKanupriya AgnihotriNo ratings yet

- Compromises: ART. 2028-2041, NEW CIVIL CODEDocument98 pagesCompromises: ART. 2028-2041, NEW CIVIL CODEJul A.No ratings yet

- Dinap 070Document6 pagesDinap 070Chris BuckNo ratings yet

- 07-15-10 Issue of The San Mateo Daily JournalDocument26 pages07-15-10 Issue of The San Mateo Daily JournalSan Mateo Daily JournalNo ratings yet

- Dbsec2 3Document173 pagesDbsec2 3Juan Luis ValleNo ratings yet

- The Jere Beasley Report, Jun. 2007Document52 pagesThe Jere Beasley Report, Jun. 2007Beasley AllenNo ratings yet

- Coffin v. Atlantic Power Corp., 2015 ONSC 3686Document43 pagesCoffin v. Atlantic Power Corp., 2015 ONSC 3686Drew HasselbackNo ratings yet

- Aguinaldo v. AquinoDocument5 pagesAguinaldo v. AquinoAnonymous ScuLSFTNo ratings yet

- United States ConstitutionDocument20 pagesUnited States ConstitutionMuayad HussainNo ratings yet

- In Re Victorio D LanuevoDocument54 pagesIn Re Victorio D LanuevoChristine Karen BumanlagNo ratings yet