You might also like

- Derivaties CNDocument34 pagesDerivaties CNMarshNo ratings yet

- Module 2 - Forwards & FuturesDocument84 pagesModule 2 - Forwards & FuturesSanjay PatilNo ratings yet

- Determining Forward and Futures Prices (F0Document40 pagesDetermining Forward and Futures Prices (F0Aradhita BaruahNo ratings yet

- Forward Contract and HedgingDocument78 pagesForward Contract and HedgingAnvesha TyagiNo ratings yet

- Derivatives 2Document14 pagesDerivatives 2Omkar DeshmukhNo ratings yet

- Introduction To DerivativesDocument139 pagesIntroduction To Derivativesnivedita_h42404No ratings yet

- Before Commitment Commits You, Commit To The Commitment: Sundar B. N. Assistant Professor Coordinator ofDocument34 pagesBefore Commitment Commits You, Commit To The Commitment: Sundar B. N. Assistant Professor Coordinator ofH B SantoshNo ratings yet

- Example: Currency Forward ContractsDocument23 pagesExample: Currency Forward ContractsRenjul ParavurNo ratings yet

- Derivatives and Risk Management: What Does Forward Contract MeanDocument9 pagesDerivatives and Risk Management: What Does Forward Contract MeanMd Hafizul HaqueNo ratings yet

- Corporate Finance: Class Notes 14Document24 pagesCorporate Finance: Class Notes 14Sakshi VermaNo ratings yet

- Derivatives Chapter 2 (Introduction To Futures)Document45 pagesDerivatives Chapter 2 (Introduction To Futures)zaryNo ratings yet

- Project Report On Future, Option & SwapsDocument12 pagesProject Report On Future, Option & SwapsSiddharth RaiNo ratings yet

- FIN4003 - Lecture02 - Mechanisms - of - Futures 16 Mar 2018Document27 pagesFIN4003 - Lecture02 - Mechanisms - of - Futures 16 Mar 2018Who Am iNo ratings yet

- Project On Futures and OptionsDocument19 pagesProject On Futures and Optionsaanu1234No ratings yet

- CFA DerivativesTutorialAKBDocument57 pagesCFA DerivativesTutorialAKBsunboy moyoNo ratings yet

- Investment Banking - F-D 97Document139 pagesInvestment Banking - F-D 97Sameer Sawant100% (1)

- Derivatives and RMDocument35 pagesDerivatives and RMMichael WardNo ratings yet

- Chapter 33Document3 pagesChapter 33Mukul KadyanNo ratings yet

- $P Mayank Gautam 16117047Document62 pages$P Mayank Gautam 16117047Rachit SemaltyNo ratings yet

- Seminar On SFM - Ca Final: Archana Khetan B.A, CFA (ICFAI), MS Finance, 9930812721Document53 pagesSeminar On SFM - Ca Final: Archana Khetan B.A, CFA (ICFAI), MS Finance, 9930812721shankar k.c.No ratings yet

- Basics of Derivatives Prof. Naveen BhatiaDocument103 pagesBasics of Derivatives Prof. Naveen BhatiaJay ShahNo ratings yet

- CH 5Document20 pagesCH 522011663No ratings yet

- Ch2a - SolutionDocument31 pagesCh2a - SolutionJeevan TejaNo ratings yet

- Pravin Mandora Group TuitionsDocument4 pagesPravin Mandora Group TuitionsPravin MandoraNo ratings yet

- Fin4003 - Lecture04 - Determination - of - Forward - and - Futures - Prices 14 Sep 2019Document39 pagesFin4003 - Lecture04 - Determination - of - Forward - and - Futures - Prices 14 Sep 2019Who Am iNo ratings yet

- Forward and Futures ContractsDocument29 pagesForward and Futures ContractsMaulik ShahNo ratings yet

- Derivatives - Futures: Forward ContractsDocument5 pagesDerivatives - Futures: Forward ContractsNeeta LokhundeNo ratings yet

- Chapter 2 Forwards FuturesDocument24 pagesChapter 2 Forwards Futuresgovindpatel1990No ratings yet

- DRM 04Document58 pagesDRM 04Kannan MeiyurNo ratings yet

- Market For Currency FuturesDocument35 pagesMarket For Currency Futuresvidhya priyaNo ratings yet

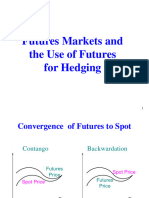

- Convergence of Future and Spot PricesDocument7 pagesConvergence of Future and Spot PricesIgnacio MaldonadoNo ratings yet

- B. Futures Contracts: Floor Brokers Who Operate On The Floor and Execute Orders For Others and For ThemselvesDocument5 pagesB. Futures Contracts: Floor Brokers Who Operate On The Floor and Execute Orders For Others and For ThemselvesNeeta LokhundeNo ratings yet

- Future ContractsDocument25 pagesFuture ContractsvishalalluriNo ratings yet

- Trading in Financial MarketsDocument42 pagesTrading in Financial MarketsthandiveNo ratings yet

- Futures Contract: From Wikipedia, The Free EncyclopediaDocument16 pagesFutures Contract: From Wikipedia, The Free Encyclopediaapi-3722617No ratings yet

- Futures Contract: Navigation SearchDocument16 pagesFutures Contract: Navigation SearchMayuresh ShirsatNo ratings yet

- Lesson 8 MBADocument27 pagesLesson 8 MBAsanjaya de silvaNo ratings yet

- Nuts and Bolts of DerivativesDocument63 pagesNuts and Bolts of DerivativesShivani GargNo ratings yet

- Currency Futures Trading GuideDocument18 pagesCurrency Futures Trading GuiderudraNo ratings yet

- 435x Lecture 2 Futures and Swaps VFinalDocument41 pages435x Lecture 2 Futures and Swaps VFinalMari Tafur BobadillaNo ratings yet

- 02 Lecture21Document29 pages02 Lecture21Ashi GargNo ratings yet

- Basic Intro 2. What Are Derivatives and Why Are They Used?Document8 pagesBasic Intro 2. What Are Derivatives and Why Are They Used?Dipti KambleNo ratings yet

- 2 Forwards & Futures PricingDocument60 pages2 Forwards & Futures PricingparthNo ratings yet

- Managing Financial Risk with DerivativesDocument17 pagesManaging Financial Risk with DerivativesbaboabNo ratings yet

- DerivativesDocument41 pagesDerivativesRajib MondalNo ratings yet

- Forward Futures GuideDocument34 pagesForward Futures GuideAnil SharmaNo ratings yet

- Interest-Rate Futures Contracts: Chapter SummaryDocument30 pagesInterest-Rate Futures Contracts: Chapter Summaryasdasd100% (1)

- Role of Financial Futures With Reference To Nse NiftyDocument58 pagesRole of Financial Futures With Reference To Nse NiftyWebsoft Tech-HydNo ratings yet

- Introduction To Derivatives: Prof. Sudhakar ReddyDocument44 pagesIntroduction To Derivatives: Prof. Sudhakar ReddyHariSharanPanjwaniNo ratings yet

- Futures and ForwardsDocument18 pagesFutures and ForwardsHimanshu PatidarNo ratings yet

- International DerivativesDocument56 pagesInternational DerivativesPradyumna SwainNo ratings yet

- Derivatives Analysis and Valuation: Learning OutcomesDocument62 pagesDerivatives Analysis and Valuation: Learning OutcomesAshutosh ModiNo ratings yet

- Derivatives Futures ReportDocument17 pagesDerivatives Futures ReportKhushi ShahNo ratings yet

- Forward Contracts: Eliminating Price Risk Through FuturesDocument49 pagesForward Contracts: Eliminating Price Risk Through FuturesPragya JainNo ratings yet

- Unit 1: Derivatives - FuturesDocument90 pagesUnit 1: Derivatives - Futuresseema mundaleNo ratings yet

- DerivativesDocument41 pagesDerivativesmugdha.ghag3921No ratings yet

- Chapter 6: Derivative Markets: Lecturer: Truong Thi Thuy Trang Email: Truongthithuytrang - Cs2@ftu - Edu.vnDocument79 pagesChapter 6: Derivative Markets: Lecturer: Truong Thi Thuy Trang Email: Truongthithuytrang - Cs2@ftu - Edu.vnHiếu Nhi TrịnhNo ratings yet

- Futures ContractsDocument45 pagesFutures ContractsRitika YachnaNo ratings yet

- Employee engagement analysis and key findingsDocument20 pagesEmployee engagement analysis and key findingsFranklin ArnoldNo ratings yet

- Ddi Measuringemployeeengagement WPDocument5 pagesDdi Measuringemployeeengagement WPSanjeev RanjanNo ratings yet

- Fast Track New TariffDocument5 pagesFast Track New TariffFranklin ArnoldNo ratings yet

- B2B Marketing: Many Businesses Are Wisely Turning Their Suppliers and Distributors Into Valued PartnersDocument27 pagesB2B Marketing: Many Businesses Are Wisely Turning Their Suppliers and Distributors Into Valued PartnersFranklin ArnoldNo ratings yet

- Bond Valuation and Yield MeasuresDocument28 pagesBond Valuation and Yield MeasuresFranklin ArnoldNo ratings yet

- Derivatives - OptionsDocument34 pagesDerivatives - OptionsFranklin ArnoldNo ratings yet

- Dealing With Competition: Rakesh Kumar Vijay Mohan Rao Kumarraja Daniel Joseph Ginu P Mathew SreejithDocument49 pagesDealing With Competition: Rakesh Kumar Vijay Mohan Rao Kumarraja Daniel Joseph Ginu P Mathew SreejithFranklin ArnoldNo ratings yet

- Klabin S.ADocument4 pagesKlabin S.AKlabin_RINo ratings yet

- Standard Due Diligence QuestionnaireDocument8 pagesStandard Due Diligence QuestionnairesharenNo ratings yet

- Lecture Note 02 - Bond Valuation and Yield MeasuresDocument75 pagesLecture Note 02 - Bond Valuation and Yield Measuresben tenNo ratings yet

- Single-Step Income Stmt. Multi-Step Income STMT.: Chapter 2 - Reading The Financial StatementsDocument23 pagesSingle-Step Income Stmt. Multi-Step Income STMT.: Chapter 2 - Reading The Financial StatementsJennaNo ratings yet

- Presentation On Kenyan Capital Gains TaxDocument21 pagesPresentation On Kenyan Capital Gains TaxWaboiNo ratings yet

- Mock Exam 1 - AnswersDocument15 pagesMock Exam 1 - AnswersKim QuyênNo ratings yet

- Project Report On Valuation of SharesDocument62 pagesProject Report On Valuation of Sharesvivek55% (11)

- Best Fibonacci Ratio and Shape Ratio For Winning Technical AnalysisDocument11 pagesBest Fibonacci Ratio and Shape Ratio For Winning Technical AnalysisYoungh SeoNo ratings yet

- Mergermarket PDFDocument5 pagesMergermarket PDFAnonymous Feglbx5No ratings yet

- HK-Listed Heng Fai Enterprises Sells Singapore Properties For S$53.9 Million (HK$328.8 Million) To SGX Catalist-Listed OELDocument2 pagesHK-Listed Heng Fai Enterprises Sells Singapore Properties For S$53.9 Million (HK$328.8 Million) To SGX Catalist-Listed OELWeR1 Consultants Pte LtdNo ratings yet

- BlackRock Midyear Investment Outlook 2014Document8 pagesBlackRock Midyear Investment Outlook 2014w24nyNo ratings yet

- Project ReportDocument54 pagesProject ReportRavi Inder SinghNo ratings yet

- Financial Derivatives CourseDocument2 pagesFinancial Derivatives CourseldlNo ratings yet

- 00 Syllabus 2024 Investments MS+readingsDocument5 pages00 Syllabus 2024 Investments MS+readingsxinluli1225No ratings yet

- Financial Derivatives 260214Document347 pagesFinancial Derivatives 260214Kavya M Bhat33% (3)

- Broker by City1Document4 pagesBroker by City1Deanna ReyesNo ratings yet

- Chapter 1Document14 pagesChapter 1RajatNo ratings yet

- Abraaj ARADocument98 pagesAbraaj ARASaamNarimanNo ratings yet

- Translate PPT AuditDocument21 pagesTranslate PPT AuditEndah DipoyantiNo ratings yet

- Nego CaseZ (Edited)Document14 pagesNego CaseZ (Edited)Marga ErumNo ratings yet

- Quiz 1 Sec01Document6 pagesQuiz 1 Sec01knight RiderNo ratings yet

- Leasing Standard IFRS 16Document6 pagesLeasing Standard IFRS 16Ani Nalitayui LifityaNo ratings yet

- Updates On Open Offer (Company Update)Document26 pagesUpdates On Open Offer (Company Update)Shyam SunderNo ratings yet

- Private Equity Secondaries China - PEI Magazine WhitepaperDocument2 pagesPrivate Equity Secondaries China - PEI Magazine WhitepaperpfuhrmanNo ratings yet

- Fundamentals of AccountingDocument56 pagesFundamentals of AccountingFiza IrfanNo ratings yet

- Capital MarketsDocument696 pagesCapital MarketsSaurabh VermaNo ratings yet

- Parliamentary Note - Raghuram RajanDocument17 pagesParliamentary Note - Raghuram RajanThe Wire100% (22)

- Gartley PatternDocument5 pagesGartley PatternOshawawookies100% (5)

- Chapter Two: The Financial Statement Auditing EnvironmentDocument34 pagesChapter Two: The Financial Statement Auditing EnvironmentKookies4No ratings yet

- Caltex v. COA - DigestDocument2 pagesCaltex v. COA - DigestChie Z. Villasanta71% (7)