You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Meet The Money 2011® Jan Freitag, STR: US Lodging Industry - What Lies Ahead?Document28 pagesMeet The Money 2011® Jan Freitag, STR: US Lodging Industry - What Lies Ahead?JefferMangelsNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

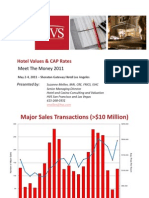

- Suzanne Mellen, HVS: Hotel Values and Cap RatesDocument29 pagesSuzanne Mellen, HVS: Hotel Values and Cap RatesJefferMangelsNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Daniel Lesser, U.S. Lodging Industry Analysis, September 2016Document7 pagesDaniel Lesser, U.S. Lodging Industry Analysis, September 2016JefferMangelsNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- General Introduction To Assignment For Benefit of CreditorsDocument9 pagesGeneral Introduction To Assignment For Benefit of CreditorsJefferMangelsNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Art Adler, Jones Lang LaSalle Hotels: Global Capital MarketsDocument17 pagesArt Adler, Jones Lang LaSalle Hotels: Global Capital MarketsJefferMangelsNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Richard Green, USC Lusk Center: Economy and OutlookDocument13 pagesRichard Green, USC Lusk Center: Economy and OutlookJefferMangelsNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Commercial Finance Roundtable: A Creditor's Plan - A Way Out of The Morass of A Single Asset Real Estate Bankruptcy CaseDocument2 pagesCommercial Finance Roundtable: A Creditor's Plan - A Way Out of The Morass of A Single Asset Real Estate Bankruptcy CaseJefferMangelsNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Meet The Money 2011® Mark Woodworth, PKF: Expensive OilDocument28 pagesMeet The Money 2011® Mark Woodworth, PKF: Expensive OilJefferMangelsNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Suzanne Mellen, HVS: Hotel Value & CAP RatesDocument29 pagesSuzanne Mellen, HVS: Hotel Value & CAP RatesJefferMangelsNo ratings yet

- U.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research AnalyticsDocument66 pagesU.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research Analyticsal11823No ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Benoit Gateau CuminDocument11 pagesBenoit Gateau Cuminal11823No ratings yet

- Illuminating The Dark Side of The BankDocument44 pagesIlluminating The Dark Side of The BankJefferMangelsNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- MTM Westergom PMDocument13 pagesMTM Westergom PMJefferMangelsNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- U.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research AnalyticsDocument66 pagesU.S. Lodging Industry - Is There Light at The End of The Tunnel? by Greg Hartmann From Smith Travel Research Analyticsal11823No ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- PKF Forecasts by Mark Woodworth, PKF Consulting at Meet The Money 2010Document49 pagesPKF Forecasts by Mark Woodworth, PKF Consulting at Meet The Money 2010al11823No ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Loeb Meet The Money Presentation 5-4-2010Document35 pagesLoeb Meet The Money Presentation 5-4-2010JefferMangelsNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Receiverships 101Document41 pagesReceiverships 101JefferMangelsNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Receivership 201Document1 pageReceivership 201JefferMangelsNo ratings yet

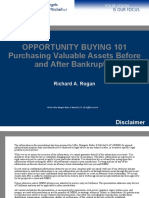

- Opportunity Buying 101 Purchasing Valuable Assets Before and After BankruptcyDocument28 pagesOpportunity Buying 101 Purchasing Valuable Assets Before and After BankruptcyJefferMangelsNo ratings yet

- Financing Companies in Chap 11: How To Do It, How To Profit From ItDocument18 pagesFinancing Companies in Chap 11: How To Do It, How To Profit From ItJefferMangelsNo ratings yet

- Loeb Meet The Money Presentation 5-4-2010Document35 pagesLoeb Meet The Money Presentation 5-4-2010JefferMangelsNo ratings yet

- What To Send CounselDocument1 pageWhat To Send CounselJefferMangelsNo ratings yet

- RAR Property Sciences WebinarDocument23 pagesRAR Property Sciences WebinarJefferMangelsNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Receiverships 101Document41 pagesReceiverships 101JefferMangelsNo ratings yet

- Receiverships 101Document41 pagesReceiverships 101JefferMangelsNo ratings yet

- Financing Companies in Chap 11: How To Do It, How To Profit From ItDocument18 pagesFinancing Companies in Chap 11: How To Do It, How To Profit From ItJefferMangelsNo ratings yet

- Special Assets "Tricks of The Trade": San Francisco OfficeDocument14 pagesSpecial Assets "Tricks of The Trade": San Francisco OfficeJefferMangelsNo ratings yet

- Jurnal Kas Penerimaan dan PengeluaranDocument44 pagesJurnal Kas Penerimaan dan PengeluaranRosan DiniNo ratings yet

- Mock 1Document10 pagesMock 1Manan SharmaNo ratings yet

- Punyak SatishDocument1 pagePunyak Satish45Punyak SatishPGDM RMIIINo ratings yet

- Inventory ManagementDocument109 pagesInventory ManagementsreevardhanNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- MGT211 Lecture 07Document12 pagesMGT211 Lecture 07Abdul Hannan Sohail0% (1)

- IQRA UNIVERSITY (AIRPORT CAMPUS) ANALYSIS OF FINANCIAL STATEMENT ASSIGNMENTDocument4 pagesIQRA UNIVERSITY (AIRPORT CAMPUS) ANALYSIS OF FINANCIAL STATEMENT ASSIGNMENTafaq ahmedNo ratings yet

- Tutorial Letter 102/3/2018: Introductory Financial AccountingDocument84 pagesTutorial Letter 102/3/2018: Introductory Financial AccountingNgoni B MakakaNo ratings yet

- First Online Quiz - 3Document4 pagesFirst Online Quiz - 3정은주No ratings yet

- Compustat Global in WRDS The BasicsDocument27 pagesCompustat Global in WRDS The BasicsVaike ChrisNo ratings yet

- Cash and Accrual Discussion301302Document2 pagesCash and Accrual Discussion301302Gloria BeltranNo ratings yet

- FAR 4.2MC ReceivablesDocument8 pagesFAR 4.2MC ReceivableschristineNo ratings yet

- Carlo Corp acquisition of John Co assetsDocument7 pagesCarlo Corp acquisition of John Co assetsAlarich CatayocNo ratings yet

- Wilcon Depot Preliminary Prospectus Under 40 CharactersDocument165 pagesWilcon Depot Preliminary Prospectus Under 40 CharactersRalph SamsonNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Stock Valuation: Liuren WuDocument45 pagesStock Valuation: Liuren WuHay JirenyaaNo ratings yet

- Blaine Kitchenware Inc.Document13 pagesBlaine Kitchenware Inc.vishitj100% (4)

- 02-Stock Basics-Tutorial PDFDocument14 pages02-Stock Basics-Tutorial PDFbassmastahNo ratings yet

- Search Fund Primer '09Document92 pagesSearch Fund Primer '09Nikolay TsvetkovNo ratings yet

- Module 3 Chapter 15 DCF ModelDocument5 pagesModule 3 Chapter 15 DCF ModelAvinash GanesanNo ratings yet

- Advani Hotels AR2023Document227 pagesAdvani Hotels AR2023Sriram RanganathanNo ratings yet

- Annual Report FY'18Document190 pagesAnnual Report FY'18Mudit KediaNo ratings yet

- How To Use PE Ratio To Value A Stock - Moneycontrol PDFDocument2 pagesHow To Use PE Ratio To Value A Stock - Moneycontrol PDFEvelyn KeaneNo ratings yet

- Handout 3Document51 pagesHandout 3Jilian Kate Alpapara Bustamante100% (1)

- 7-Year Asset Class Real Return Forecasts : As of August 31, 2020Document1 page7-Year Asset Class Real Return Forecasts : As of August 31, 2020Stanley MunodawafaNo ratings yet

- Debt RestructuringDocument1 pageDebt RestructuringSherri BonquinNo ratings yet

- Concepts of Income, Gross Income, and Compensation IncomeDocument61 pagesConcepts of Income, Gross Income, and Compensation IncomeMeden Robrigado-LabogNo ratings yet

- MODFIN2 Calendar PDFDocument1 pageMODFIN2 Calendar PDFMich ClementeNo ratings yet

- Basis For Qualified OpinionDocument1 pageBasis For Qualified OpinionannNo ratings yet

- 1st Ass.Document5 pages1st Ass.Lorraine Millama Puray100% (1)

- GPID100552 Term SheetDocument125 pagesGPID100552 Term SheetShubham SinghNo ratings yet

- Impact of Dividend Policy on Stock PricesDocument11 pagesImpact of Dividend Policy on Stock PricesBayalkotee ReshamNo ratings yet