You might also like

- The Affordable Care Act and New Yorkers: The Gift That Keeps On GivingDocument22 pagesThe Affordable Care Act and New Yorkers: The Gift That Keeps On GivingPublic Policy and Education Fund of NYNo ratings yet

- Health Care What Does It MeanDocument4 pagesHealth Care What Does It MeansjcgopnwNo ratings yet

- One Year Later OhDocument3 pagesOne Year Later OhProgressOhio251No ratings yet

- Payers & Providers Midwest Edition - Issue of June 5, 2012Document6 pagesPayers & Providers Midwest Edition - Issue of June 5, 2012PayersandProvidersNo ratings yet

- Hcentive Health Insurance Exchange PlatformDocument16 pagesHcentive Health Insurance Exchange PlatformalishanorthNo ratings yet

- Midwest Edition: Illinois Swings Machete at Safety NetDocument6 pagesMidwest Edition: Illinois Swings Machete at Safety NetPayersandProvidersNo ratings yet

- IDC Long Term Care 2.28.11Document3 pagesIDC Long Term Care 2.28.11Rich AzzopardiNo ratings yet

- Aca Powerpoint 12 3 13 RevisedDocument17 pagesAca Powerpoint 12 3 13 Revisedapi-242371940No ratings yet

- Healthy California Act AnalysisDocument8 pagesHealthy California Act AnalysisDylan MatthewsNo ratings yet

- California Edition: DMHC Orders Retroactive PaymentsDocument6 pagesCalifornia Edition: DMHC Orders Retroactive PaymentsPayersandProvidersNo ratings yet

- Understanding The ACA's Health Care ExchangesDocument10 pagesUnderstanding The ACA's Health Care ExchangesMarketingRCANo ratings yet

- Here'S Everything The Federal Government Has Done To Respond To The Coronavirus So FarDocument5 pagesHere'S Everything The Federal Government Has Done To Respond To The Coronavirus So FarCoral GuntherNo ratings yet

- CT5 Health Care Fact SheetDocument4 pagesCT5 Health Care Fact SheetAlfonso RobinsonNo ratings yet

- Midwest Edition: Michigan Debates Medicaid TaxDocument7 pagesMidwest Edition: Michigan Debates Medicaid TaxPayersandProvidersNo ratings yet

- Privatizing Medicaid in ColoradoDocument7 pagesPrivatizing Medicaid in ColoradoIndependence InstituteNo ratings yet

- Obama Care RolloutDocument18 pagesObama Care Rolloutmyrant2No ratings yet

- GOP Healthcare Policy Briefing: Repeal and ReplaceDocument19 pagesGOP Healthcare Policy Briefing: Repeal and ReplacePBS NewsHour100% (3)

- Actu CanadaDocument8 pagesActu CanadaJuasadf IesafNo ratings yet

- NIHOE PPT - Tribal Leaders Series IIDocument20 pagesNIHOE PPT - Tribal Leaders Series IINIHOE3No ratings yet

- Payers & Providers California Edition - Issue of May 3, 2012Document6 pagesPayers & Providers California Edition - Issue of May 3, 2012PayersandProvidersNo ratings yet

- Midwest Edition: Cost-Cutting Measures in MissouriDocument5 pagesMidwest Edition: Cost-Cutting Measures in MissouriPayersandProvidersNo ratings yet

- Current Events 3Document2 pagesCurrent Events 3api-101202183No ratings yet

- How Will U.S. Healthcare Reform Affect Medical Tourism Jonathan Edelheit, CEO Medical Tourism Association™Document31 pagesHow Will U.S. Healthcare Reform Affect Medical Tourism Jonathan Edelheit, CEO Medical Tourism Association™Patrick AdamsNo ratings yet

- Sebelius TestimonyDocument7 pagesSebelius TestimonyabbyrogersNo ratings yet

- Senate Hearing, 108TH Congress - Medicaid in Crisis: Could Long Term Care Partnerships Be Part of The Solution?Document88 pagesSenate Hearing, 108TH Congress - Medicaid in Crisis: Could Long Term Care Partnerships Be Part of The Solution?Scribd Government DocsNo ratings yet

- 10-30-09 Top 10 Reasons To Oppose Pelosi-CareDocument5 pages10-30-09 Top 10 Reasons To Oppose Pelosi-CareChris RowanNo ratings yet

- Massachusetts' Plan: A Failed Model For Health Care Reform: February 18, 2009Document19 pagesMassachusetts' Plan: A Failed Model For Health Care Reform: February 18, 2009raj2closeNo ratings yet

- ff321 0Document4 pagesff321 0Jennifer PeeblesNo ratings yet

- Executive Summary - Medicaid Expansion White PaperDocument29 pagesExecutive Summary - Medicaid Expansion White PaperCourier JournalNo ratings yet

- WeeklyDigest614 618fordistributionDocument5 pagesWeeklyDigest614 618fordistributionapi-27836025No ratings yet

- WWW Kline House Gov/issuesDocument1 pageWWW Kline House Gov/issuesapi-97559023No ratings yet

- New York Health Act PresentationDocument9 pagesNew York Health Act PresentationrooseveltislanderNo ratings yet

- California Edition: Providers Line Up Against InitiativeDocument7 pagesCalifornia Edition: Providers Line Up Against InitiativePayersandProvidersNo ratings yet

- Bernie Sanders' "Medicare For All" PlanDocument8 pagesBernie Sanders' "Medicare For All" PlanDylan Matthews100% (2)

- How To Appeal A Health Care Insurance Decision - OIC 2019Document62 pagesHow To Appeal A Health Care Insurance Decision - OIC 2019Jeff ReifmanNo ratings yet

- Dear Governor Feb 24Document3 pagesDear Governor Feb 24KFFHealthNewsNo ratings yet

- The Business of Health Care ReformDocument23 pagesThe Business of Health Care ReformnsmorgNo ratings yet

- Midwest Edition: Michigan Has A $1 Billion QuestionDocument5 pagesMidwest Edition: Michigan Has A $1 Billion QuestionPayersandProvidersNo ratings yet

- Thanksgiving Health Care HandoutDocument1 pageThanksgiving Health Care HandoutNathan BenefieldNo ratings yet

- 17 Benefits For Seniors at NYDocument24 pages17 Benefits For Seniors at NYAbu HudaNo ratings yet

- NYS DOB - Health Dept Budget 2018 HightlightsDocument13 pagesNYS DOB - Health Dept Budget 2018 Hightlightssrikrishna natesanNo ratings yet

- (Peter Ferrara) The Obamacare DisasterDocument78 pages(Peter Ferrara) The Obamacare DisasterYusuf KaripekNo ratings yet

- IN Healthcare FactsDocument2 pagesIN Healthcare FactskrisluidhardtNo ratings yet

- California Edition: Blue Cross Backs Off Some IncreasesDocument6 pagesCalifornia Edition: Blue Cross Backs Off Some IncreasesPayersandProvidersNo ratings yet

- SHARE Grantee Newsletter October 2009Document4 pagesSHARE Grantee Newsletter October 2009butle180No ratings yet

- In Healthcare Facts 2Document2 pagesIn Healthcare Facts 2krisluidhardtNo ratings yet

- Comparison of The 2008 Major Party PlatformsDocument5 pagesComparison of The 2008 Major Party Platformscmalone410No ratings yet

- ACA SummaryDocument9 pagesACA SummaryScottRobertLaneNo ratings yet

- An Overview of The White Paper " Caring For Our Future - Reforming Care and Support"Document4 pagesAn Overview of The White Paper " Caring For Our Future - Reforming Care and Support"My Care My HomeNo ratings yet

- Affordable Care Act Research PaperDocument4 pagesAffordable Care Act Research Papereffbd7j4100% (1)

- Summary of Graham-CassidyDocument12 pagesSummary of Graham-CassidyTPPFNo ratings yet

- 2010-04-02 - Health Care Reform ArticleDocument4 pages2010-04-02 - Health Care Reform ArticleTerry PetersonNo ratings yet

- VRRFDocument18 pagesVRRFDan NgugiNo ratings yet

- TCYH WomenDocument11 pagesTCYH WomenlocalonNo ratings yet

- Options To Finance Medicare For All: $500 BillionDocument6 pagesOptions To Finance Medicare For All: $500 BillionBradyNo ratings yet

- English 1103 Research PresentationDocument18 pagesEnglish 1103 Research PresentationZnaLeGrandNo ratings yet

- Covid-19 Resource PDFDocument5 pagesCovid-19 Resource PDFCat SalazarNo ratings yet

- New Solvency Advocate Walker 17Document4 pagesNew Solvency Advocate Walker 17saifbajwa9038No ratings yet

- Cornell ComplaintDocument41 pagesCornell Complaintjspector100% (1)

- Pennies For Charity 2018Document12 pagesPennies For Charity 2018ZacharyEJWilliamsNo ratings yet

- Joseph Ruggiero Employment AgreementDocument6 pagesJoseph Ruggiero Employment AgreementjspectorNo ratings yet

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocument8 pagesFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorNo ratings yet

- State Health CoverageDocument26 pagesState Health CoveragejspectorNo ratings yet

- IG LetterDocument3 pagesIG Letterjspector100% (1)

- Federal Budget Fiscal Year 2017 Web VersionDocument36 pagesFederal Budget Fiscal Year 2017 Web VersionjspectorNo ratings yet

- NYSCrimeReport2016 PrelimDocument14 pagesNYSCrimeReport2016 PrelimjspectorNo ratings yet

- Siena Poll March 27, 2017Document7 pagesSiena Poll March 27, 2017jspectorNo ratings yet

- Abo 2017 Annual ReportDocument65 pagesAbo 2017 Annual ReportrkarlinNo ratings yet

- 2017 08 18 Constitution OrderDocument27 pages2017 08 18 Constitution OrderjspectorNo ratings yet

- Class of 2022Document1 pageClass of 2022jspectorNo ratings yet

- SNY0517 Crosstabs 052417Document4 pagesSNY0517 Crosstabs 052417Nick ReismanNo ratings yet

- Inflation AllowablegrowthfactorsDocument1 pageInflation AllowablegrowthfactorsjspectorNo ratings yet

- Teacher Shortage Report 05232017 PDFDocument16 pagesTeacher Shortage Report 05232017 PDFjspectorNo ratings yet

- Oag Sed Letter Ice 2-27-17Document3 pagesOag Sed Letter Ice 2-27-17BethanyNo ratings yet

- Opiods 2017-04-20-By Numbers Brief No8Document17 pagesOpiods 2017-04-20-By Numbers Brief No8rkarlinNo ratings yet

- Hiffa Settlement Agreement ExecutedDocument5 pagesHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- p12 Budget Testimony 2-14-17Document31 pagesp12 Budget Testimony 2-14-17jspectorNo ratings yet

- Youth Cigarette and E-Cigs UseDocument1 pageYouth Cigarette and E-Cigs UsejspectorNo ratings yet

- 2017 School Bfast Report Online Version 3-7-17 0Document29 pages2017 School Bfast Report Online Version 3-7-17 0jspectorNo ratings yet

- 2016 Local Sales Tax CollectionsDocument4 pages2016 Local Sales Tax CollectionsjspectorNo ratings yet

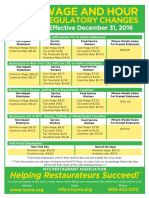

- Wage and Hour Regulatory Changes 2016Document2 pagesWage and Hour Regulatory Changes 2016jspectorNo ratings yet

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocument55 pages16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorNo ratings yet

- Schneiderman Voter Fraud Letter 022217Document2 pagesSchneiderman Voter Fraud Letter 022217Matthew HamiltonNo ratings yet

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Document4 pagesActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorNo ratings yet

- Darweesh Cities AmicusDocument32 pagesDarweesh Cities AmicusjspectorNo ratings yet

- Voting Report CardDocument1 pageVoting Report CardjspectorNo ratings yet

- Review of Executive Budget 2017Document102 pagesReview of Executive Budget 2017Nick ReismanNo ratings yet

- Pub Auth Num 2017Document54 pagesPub Auth Num 2017jspectorNo ratings yet

- United States v. Irwin Halper, 590 F.2d 422, 2d Cir. (1979)Document15 pagesUnited States v. Irwin Halper, 590 F.2d 422, 2d Cir. (1979)Scribd Government DocsNo ratings yet

- ..Document18 pages..keyurpatel1993No ratings yet

- 2023-06-01 St. Mary's County Times With 2023 GraduatesDocument48 pages2023-06-01 St. Mary's County Times With 2023 GraduatesSouthern Maryland OnlineNo ratings yet

- Training MateriaL RCM (Healthcare)Document66 pagesTraining MateriaL RCM (Healthcare)Naveen Babu100% (1)

- Medicare and Clinical Research StudiesDocument8 pagesMedicare and Clinical Research StudiesAbdullah TheNo ratings yet

- PractiX 1.43 Functionality and FixesDocument2 pagesPractiX 1.43 Functionality and FixesLuis Fernando Garcia SanchezNo ratings yet

- Coding ComplianceDocument26 pagesCoding ComplianceBently JohnsonNo ratings yet

- Budget Hospital and General Extras Plus Product SummaryDocument4 pagesBudget Hospital and General Extras Plus Product SummaryJames SandersNo ratings yet

- Student Health Policy: Eligibility and Enrollment For Student Health Plan CoverageDocument5 pagesStudent Health Policy: Eligibility and Enrollment For Student Health Plan CoverageErick Álvarez-SarabiaNo ratings yet

- Bio-Reference Laboratories Whistle-Blower ComplaintDocument11 pagesBio-Reference Laboratories Whistle-Blower ComplaintBRLIwhistleblower100% (1)

- Ebersole and Hess' Gerontological Nursing & Healthy AgingDocument451 pagesEbersole and Hess' Gerontological Nursing & Healthy AgingEunice Camero100% (1)

- Chapter 5 Residents RightsDocument79 pagesChapter 5 Residents Rightsrem1611No ratings yet

- Full Test Bank For Introduction To Health Care Finance and Accounting 1St Edition Carlene Harrison William P Harrison PDF Docx Full Chapter ChapterDocument36 pagesFull Test Bank For Introduction To Health Care Finance and Accounting 1St Edition Carlene Harrison William P Harrison PDF Docx Full Chapter Chaptercitiedcorneuleb4ket100% (8)

- February 2018 DWDocument76 pagesFebruary 2018 DWfasdfaNo ratings yet

- Secure Access 2015Document16 pagesSecure Access 2015api-288656991No ratings yet

- Montefiore Health System Q1 2020 Financial StatementsDocument25 pagesMontefiore Health System Q1 2020 Financial StatementsJonathan LaMantiaNo ratings yet

- University of The Free State Main Test 2 Marking Guide Public Law ASSESSOR: MR K B Motshabi Internal Moderator: DR C Vinti Time: 90 Minutes MarksDocument3 pagesUniversity of The Free State Main Test 2 Marking Guide Public Law ASSESSOR: MR K B Motshabi Internal Moderator: DR C Vinti Time: 90 Minutes Marksnomfundo ngidiNo ratings yet

- Nursing Assistant A Nursing Process Approach 11Th Edition Acello Solutions Manual Full Chapter PDFDocument67 pagesNursing Assistant A Nursing Process Approach 11Th Edition Acello Solutions Manual Full Chapter PDFhelgasophie7478k0100% (7)

- How to Retire with Virginia Retirement SystemDocument36 pagesHow to Retire with Virginia Retirement SystemRISHIKESH VAJPAYEENo ratings yet

- The Beacon - October 24, 2013Document14 pagesThe Beacon - October 24, 2013Catawba SecurityNo ratings yet

- Paradigm Shift EssayDocument10 pagesParadigm Shift Essayapi-456202876No ratings yet

- Dear Colleague LetterDocument3 pagesDear Colleague LetterAlexis LeonardNo ratings yet

- Notice: Scientific Misconduct Findings Administrative Actions: Grol, Jessica LeeDocument2 pagesNotice: Scientific Misconduct Findings Administrative Actions: Grol, Jessica LeeJustia.comNo ratings yet

- Medical Sociology 12th Edition Cockerham Test BankDocument10 pagesMedical Sociology 12th Edition Cockerham Test Banklilyadelaides4zo100% (29)

- Emporium City Mall Work Immersion ReportDocument26 pagesEmporium City Mall Work Immersion ReportJad LavillaNo ratings yet

- Assignment On Health InsuranceDocument34 pagesAssignment On Health InsuranceSamrah SiddiquiNo ratings yet

- Fundamentals of Project Planning and ManagementDocument119 pagesFundamentals of Project Planning and ManagementamendaNo ratings yet

- Motion To ClarifyDocument19 pagesMotion To Clarifymjeltsen100% (1)

- AHCM HealthSocialNeedsScreeningTool Rev 8 - 10 - 2021Document10 pagesAHCM HealthSocialNeedsScreeningTool Rev 8 - 10 - 2021submarinoaguadulceNo ratings yet

- Rga Healthcare Letter JulyDocument5 pagesRga Healthcare Letter Julyjthompson8793No ratings yet