You might also like

- Tax Policy Presentation QuidelinesDocument3 pagesTax Policy Presentation Quidelinesdchristensen5No ratings yet

- AuditingDocument35 pagesAuditingbabaabbyNo ratings yet

- Tax Reform Act of 2014 DraftDocument1,184 pagesTax Reform Act of 2014 Draftdchristensen5No ratings yet

- Auditing Seminar: Advanced CourseDocument8 pagesAuditing Seminar: Advanced Coursedchristensen5No ratings yet

- Arya Glover SunderDocument6 pagesArya Glover Sunderdchristensen5No ratings yet

- ACCT 816 Syllabus Summer 2015Document1 pageACCT 816 Syllabus Summer 2015dchristensen5No ratings yet

- Six Flags 2012 Annual Report FinalDocument150 pagesSix Flags 2012 Annual Report Finaldchristensen5No ratings yet

- A Review and Integration of Empirical Research On Materiality: Two Decades LaterDocument36 pagesA Review and Integration of Empirical Research On Materiality: Two Decades Laterdchristensen5No ratings yet

- Away Game Expense InvoicesDocument2 pagesAway Game Expense Invoicesdchristensen5No ratings yet

- Carson Et Al. (WP, 2012)Document124 pagesCarson Et Al. (WP, 2012)dchristensen5No ratings yet

- QC 00010Document32 pagesQC 00010dchristensen5No ratings yet

- Student Handouts - Fraud CaseDocument30 pagesStudent Handouts - Fraud Casedchristensen5No ratings yet

- Auditing Seminar: Advanced CourseDocument8 pagesAuditing Seminar: Advanced Coursedchristensen5No ratings yet

- Ethridge Et Al. (JBER, 2007)Document8 pagesEthridge Et Al. (JBER, 2007)dchristensen5No ratings yet

- Auditor Going-Concern Opinion Shifts Market ValuationDocument26 pagesAuditor Going-Concern Opinion Shifts Market Valuationdchristensen5No ratings yet

- Game Schedule May - September: Date Opponent LocationDocument1 pageGame Schedule May - September: Date Opponent Locationdchristensen5No ratings yet

- TM Allocation - Darden 2014Document5 pagesTM Allocation - Darden 2014dchristensen5No ratings yet

- Visa StatementsDocument1 pageVisa Statementsdchristensen5No ratings yet

- The Economics of Ethics: A New Perspective On Agency TheoryDocument11 pagesThe Economics of Ethics: A New Perspective On Agency Theorydchristensen5No ratings yet

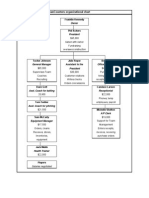

- Handout 1. Tallahassee Beancounters Organizational Chart: OwnerDocument1 pageHandout 1. Tallahassee Beancounters Organizational Chart: Ownerdchristensen5No ratings yet

- Equipement Purchase Orders, Invoices, and Receiving SlipsDocument1 pageEquipement Purchase Orders, Invoices, and Receiving Slipsdchristensen5No ratings yet

- Problem 1 - CH 11Document1 pageProblem 1 - CH 11dchristensen5No ratings yet

- Chart of accounts handoutDocument1 pageChart of accounts handoutdchristensen5No ratings yet

- Student Handout 4. General Journal EntriesDocument5 pagesStudent Handout 4. General Journal Entriesdchristensen5No ratings yet

- Construction Invoices Received by TBCDocument4 pagesConstruction Invoices Received by TBCdchristensen5No ratings yet

- ConcessionsDocument1 pageConcessionsdchristensen5No ratings yet

- 01 - Problems Solutions - 12EDocument30 pages01 - Problems Solutions - 12Edchristensen5No ratings yet

- Chapter 1 ChartDocument1 pageChapter 1 Chartdchristensen5No ratings yet

- 01SV Intro To Animal ProductsDocument16 pages01SV Intro To Animal Productsdchristensen5No ratings yet

- FINA 463 Exam PrepDocument4 pagesFINA 463 Exam Prepdchristensen5No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Mega PostDocument5 pagesMega PostandreyfgNo ratings yet

- MBA Research Report on Scope of E-MarketingDocument109 pagesMBA Research Report on Scope of E-Marketingaryanboxer78667% (3)

- COA Circular 2004-014, Solana CovenantDocument2 pagesCOA Circular 2004-014, Solana CovenantStBernard15100% (1)

- Contoh Soalan RAE Dan Jawapan 2-1Document5 pagesContoh Soalan RAE Dan Jawapan 2-1Norakmal Hisyam AkmalNo ratings yet

- Sample Exam - AssuranceDocument57 pagesSample Exam - AssuranceHương MaiNo ratings yet

- Marketing Research-Amway India LTDDocument53 pagesMarketing Research-Amway India LTDSunny Chauhan25% (4)

- Remedies For Breach of Directors' DutiesDocument1 pageRemedies For Breach of Directors' DutiesIZZAH ZAHIN100% (2)

- Information Request For Audit Quotation 20210702Document3 pagesInformation Request For Audit Quotation 20210702Htet Htet AungNo ratings yet

- Select Butter Supplier for Amul Based on DescriptionsDocument1 pageSelect Butter Supplier for Amul Based on Descriptionsneer2898No ratings yet

- Asik Das CVDocument2 pagesAsik Das CVAsik DasNo ratings yet

- Righthaven Copyright Infringement Complaint Against Silver Matrix, LLC, Et Al.Document19 pagesRighthaven Copyright Infringement Complaint Against Silver Matrix, LLC, Et Al.www.righthavenlawsuits.comNo ratings yet

- LO305 Basic Data For Process ManufacturingDocument425 pagesLO305 Basic Data For Process Manufacturingchandra9000100% (1)

- Red Hat JBoss Enterprise Application Platform-7.1-Introduction To JBoss EAP-es-ESDocument12 pagesRed Hat JBoss Enterprise Application Platform-7.1-Introduction To JBoss EAP-es-ESYesidRaadRomeroNo ratings yet

- BBSG4103 Marketing Management Strategy Assignment 1Document4 pagesBBSG4103 Marketing Management Strategy Assignment 1Calistus Eugene FernandoNo ratings yet

- BenchmarkingDocument12 pagesBenchmarkingapi-385350449No ratings yet

- Sell Side M&aDocument21 pagesSell Side M&aVishan Sharma100% (1)

- 4654 1-2012Document7 pages4654 1-2012Parashuram Chauhan0% (3)

- Digital Marketing Scope and Career OpportunitiesDocument15 pagesDigital Marketing Scope and Career Opportunitiesarunmittal1985No ratings yet

- Fixed Asset Accounting - AccountingToolsDocument3 pagesFixed Asset Accounting - AccountingToolsPankaj Gautam0% (2)

- Cease and Desist DemandDocument2 pagesCease and Desist Demandmasonw223No ratings yet

- Marketing Mix Physical Evidence: Ashiq T.E (PA1105) Manish Pillai (PA1120) Rohit Sharma (PA1129)Document13 pagesMarketing Mix Physical Evidence: Ashiq T.E (PA1105) Manish Pillai (PA1120) Rohit Sharma (PA1129)Roshni RajNo ratings yet

- CH 10 Case BinalDocument3 pagesCH 10 Case BinalJordanRamosManurung100% (2)

- Acctg 14 - Midterm ExamDocument4 pagesAcctg 14 - Midterm ExamNANNo ratings yet

- IBM Netezza 1000: High-Performance Business Intelligence and Advanced Analytics For The EnterpriseDocument6 pagesIBM Netezza 1000: High-Performance Business Intelligence and Advanced Analytics For The EnterpriseArpan GuptaNo ratings yet

- Nokia - Flexi OutdoorCase - Quick Installation Guide PDFDocument10 pagesNokia - Flexi OutdoorCase - Quick Installation Guide PDFRalaivao Solofohery Dieu-donnéNo ratings yet

- Comparison of Patents, Trademarks, Copyrights, Andtrade SecretsDocument1 pageComparison of Patents, Trademarks, Copyrights, Andtrade Secretsozy05No ratings yet

- P1 - Financial Accounting April 07Document23 pagesP1 - Financial Accounting April 07IrfanNo ratings yet

- Mahindra Mahindra Annual Report 2018 19 PDFDocument392 pagesMahindra Mahindra Annual Report 2018 19 PDFMUHAMMED RABIHNo ratings yet

- Uk Consulting FirmsDocument36 pagesUk Consulting FirmsAlina TeodorescuNo ratings yet

- Curriculum VitaeDocument2 pagesCurriculum VitaetaliyabooksNo ratings yet