You might also like

- Global - Close To Peak USD LiquidityDocument7 pagesGlobal - Close To Peak USD LiquidityBLBVORTEXNo ratings yet

- Blackrockgold Presentation July-3Document26 pagesBlackrockgold Presentation July-3BLBVORTEXNo ratings yet

- Fs SP 500 Utilities SectorDocument6 pagesFs SP 500 Utilities SectorBLBVORTEXNo ratings yet

- DVAX Coporate Presentation Strong Buy...Document26 pagesDVAX Coporate Presentation Strong Buy...BLBVORTEXNo ratings yet

- Current Tanker RatesSept12Document3 pagesCurrent Tanker RatesSept12BLBVORTEXNo ratings yet

- KPMG China Pharmaceutical 201106Document62 pagesKPMG China Pharmaceutical 201106merc2No ratings yet

- BIS Working Papers 2Document35 pagesBIS Working Papers 2AdminAliNo ratings yet

- Ziopharm Slides To Accompany Q3 2019 Call 110719 FinalDocument13 pagesZiopharm Slides To Accompany Q3 2019 Call 110719 FinalBLBVORTEXNo ratings yet

- Sarepta JPM 2019 FinalDocument26 pagesSarepta JPM 2019 FinalBLBVORTEXNo ratings yet

- Oil Strategy - The Conviction ListDocument23 pagesOil Strategy - The Conviction ListBLBVORTEXNo ratings yet

- GloomBoomDoom Report Monetary TectonicsDocument4 pagesGloomBoomDoom Report Monetary TectonicsBLBVORTEXNo ratings yet

- Copper Mountain August 2014 Corp PresDocument29 pagesCopper Mountain August 2014 Corp PresBLBVORTEXNo ratings yet

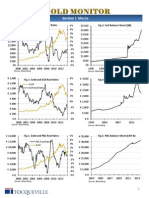

- Tocqueville Gold Monitor 4Q 2013Document11 pagesTocqueville Gold Monitor 4Q 2013Gold Silver WorldsNo ratings yet

- CIMB Navigating Thailand 2015 Dec 2014 PDFDocument212 pagesCIMB Navigating Thailand 2015 Dec 2014 PDFBLBVORTEXNo ratings yet

- BTG Petrobras January 2015Document7 pagesBTG Petrobras January 2015BLBVORTEXNo ratings yet

- CAPR ARM Investor DayDocument19 pagesCAPR ARM Investor DayBLBVORTEXNo ratings yet

- India Agriculture Inputs Seeds of Prosperity 26-02-14!15!05Document87 pagesIndia Agriculture Inputs Seeds of Prosperity 26-02-14!15!05BLBVORTEX100% (1)

- Neuralstem+Corporate+Presentation+website October+2014Document32 pagesNeuralstem+Corporate+Presentation+website October+2014BLBVORTEXNo ratings yet

- IndiapharmaDocument151 pagesIndiapharmaBLBVORTEXNo ratings yet

- OEl Gas LatAmDocument76 pagesOEl Gas LatAmBLBVORTEXNo ratings yet

- Sucden Financial Quarterly Metals Report October 2013Document60 pagesSucden Financial Quarterly Metals Report October 2013BLBVORTEXNo ratings yet

- Commodities Update - CIBC - Dec 2Document8 pagesCommodities Update - CIBC - Dec 2BLBVORTEXNo ratings yet

- Greater China Smartphone Sector 130904Document52 pagesGreater China Smartphone Sector 130904BLBVORTEXNo ratings yet

- CLSA Greed Fear 1 August 2013Document13 pagesCLSA Greed Fear 1 August 2013BLBVORTEXNo ratings yet

- Occ Asional Paper Series: China'S Economic Growth and RebalancingDocument56 pagesOcc Asional Paper Series: China'S Economic Growth and RebalancingRupojit RoyNo ratings yet

- UBS Research Focus, Sustainable Investing, July 2013.Document40 pagesUBS Research Focus, Sustainable Investing, July 2013.Glenn ViklundNo ratings yet

- VIPS 2Q13 Post Earnings PresentationDocument28 pagesVIPS 2Q13 Post Earnings PresentationBLBVORTEXNo ratings yet

- Philips Securities 2013 China Macroeconomic Semiannual Report 130726Document5 pagesPhilips Securities 2013 China Macroeconomic Semiannual Report 130726BLBVORTEXNo ratings yet

- Asia Pacific Equities Malaysia May 8th 2013Document7 pagesAsia Pacific Equities Malaysia May 8th 2013BLBVORTEXNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- ABC of ETFDocument24 pagesABC of ETFAJITAV SILUNo ratings yet

- Stock Market EfficiencyDocument31 pagesStock Market EfficiencySathish Kumar100% (1)

- A Study On Investors Preference of Commodity Markets With Special Reference To Share KhanDocument98 pagesA Study On Investors Preference of Commodity Markets With Special Reference To Share KhanAnu Joseph100% (1)

- Praj Industries LTD - Q1FY24 Result Update - 28072023 - 28-07-2023 - 11Document8 pagesPraj Industries LTD - Q1FY24 Result Update - 28072023 - 28-07-2023 - 11samraatjadhavNo ratings yet

- Gulaq Gear 6 - For HDFCDocument1 pageGulaq Gear 6 - For HDFCriddhi SalviNo ratings yet

- FinQuiz - CFA Level 3, June, 2017 - Study PlanDocument3 pagesFinQuiz - CFA Level 3, June, 2017 - Study PlanTaha OwaisNo ratings yet

- Report On Insurance CompaniesDocument50 pagesReport On Insurance CompaniesAli Hossain Akhtar100% (1)

- Foreign Direct InvestmentDocument12 pagesForeign Direct InvestmentRomeo RobinNo ratings yet

- Portfolio SelectionDocument6 pagesPortfolio SelectionAssfaw KebedeNo ratings yet

- Financial MarkatingDocument22 pagesFinancial Markatingvishu shindeNo ratings yet

- Japanese Candlestick Charting TechniquesDocument45 pagesJapanese Candlestick Charting TechniquesSau Gio SauNo ratings yet

- Reversal Patterns: Part 1Document16 pagesReversal Patterns: Part 1Oxford Capital Strategies LtdNo ratings yet

- INDIAN STOCK EXCHANGES: A BRIEF HISTORYDocument26 pagesINDIAN STOCK EXCHANGES: A BRIEF HISTORYChandrika DasNo ratings yet

- CVDocument323 pagesCVArlei EvaristoNo ratings yet

- Internal Control Affecting Liabilities and EquityDocument21 pagesInternal Control Affecting Liabilities and EquityClark Regin SimbulanNo ratings yet

- Provincial Cooperative and Enterprise Development OfficeDocument4 pagesProvincial Cooperative and Enterprise Development OfficeRoel Jr Pinaroc DolaypanNo ratings yet

- Adjusting hurdle rates for divisional riskDocument11 pagesAdjusting hurdle rates for divisional riskkrish lopezNo ratings yet

- Smile Lecture7Document18 pagesSmile Lecture7jefarnoNo ratings yet

- July 2014 Maglan Tearsheet Template (Long)Document2 pagesJuly 2014 Maglan Tearsheet Template (Long)ValueWalk100% (1)

- Delisting of SharesDocument19 pagesDelisting of SharesVasaviKaparthiNo ratings yet

- 2017 FRM Study GuideDocument24 pages2017 FRM Study GuideDuc AnhNo ratings yet

- Who Cares Wins 2005 Conference Report: Investing For Long-Term Value (October 2005)Document32 pagesWho Cares Wins 2005 Conference Report: Investing For Long-Term Value (October 2005)IFC SustainabilityNo ratings yet

- Imperial Finance Summer CourseDocument5 pagesImperial Finance Summer CourseMatthewNo ratings yet

- Salco7 12Document3 pagesSalco7 12Einstein WilliamsNo ratings yet

- Our Strategy LHN Ar16Document44 pagesOur Strategy LHN Ar16Bilal El YoussoufiNo ratings yet

- Operational Research Assignment............ (Ca Final Cost and Or)Document87 pagesOperational Research Assignment............ (Ca Final Cost and Or)Pravinn_Mahajan80% (5)

- Bulk and Block DifferenceDocument4 pagesBulk and Block DifferenceRituNo ratings yet

- Portfolio trading actions trackerDocument4 pagesPortfolio trading actions trackerJaalam AikenNo ratings yet

- Analyzing Cash Flow StatementsDocument3 pagesAnalyzing Cash Flow StatementsBJNo ratings yet