You might also like

- Employee Motivation QuestionnaireDocument2 pagesEmployee Motivation QuestionnaireShams S89% (9)

- Employee Motivation QuestionnaireDocument2 pagesEmployee Motivation QuestionnaireShams S89% (9)

- Guide To Producing A Fashion Show, 3rd EditionDocument39 pagesGuide To Producing A Fashion Show, 3rd EditionChris Laurence Balintona100% (1)

- Horlicks ProjectDocument56 pagesHorlicks ProjectShams S82% (34)

- Employee MotivationDocument78 pagesEmployee MotivationShams SNo ratings yet

- Noor Mohamed - Working Capital Management-Full ReportDocument94 pagesNoor Mohamed - Working Capital Management-Full ReportananthakumarNo ratings yet

- 2024 Becker CPA Financial (FAR) NotesDocument51 pages2024 Becker CPA Financial (FAR) NotescraigsappletreeNo ratings yet

- Training Need AssessmentDocument90 pagesTraining Need AssessmentShams S100% (1)

- Non Fund Based Activities of BankDocument53 pagesNon Fund Based Activities of BankAKSHAT MAHENDRANo ratings yet

- A Questionnaire On Quality of Work Life Name: Designation: AgeDocument3 pagesA Questionnaire On Quality of Work Life Name: Designation: AgeShams SNo ratings yet

- Management-of-Working-Capital-Notes SAUDocument104 pagesManagement-of-Working-Capital-Notes SAUSaurav MedhiNo ratings yet

- A Study On Overall Financial Performance AnalysisDocument104 pagesA Study On Overall Financial Performance Analysisaarasu007100% (2)

- Capital Budgeting or Capital ExpenditureDocument18 pagesCapital Budgeting or Capital ExpenditurePooja VaidyaNo ratings yet

- Summary of Chapter 9 Budget Preparation - Erlinda Katlanis 1081002089Document9 pagesSummary of Chapter 9 Budget Preparation - Erlinda Katlanis 1081002089Linda Katlanis100% (1)

- Financial Performance Analysis of RAIDCODocument92 pagesFinancial Performance Analysis of RAIDCOATHIRA RNo ratings yet

- Working Capital Management of JK BankDocument98 pagesWorking Capital Management of JK BankAkifaijaz100% (1)

- Lenovo Cust Satisfaction ProjDocument58 pagesLenovo Cust Satisfaction ProjShams S71% (7)

- Working Capital Management and Its Impact On Profitability Evidence From Food Complex Manufacturing Firms in Addis AbabaDocument19 pagesWorking Capital Management and Its Impact On Profitability Evidence From Food Complex Manufacturing Firms in Addis AbabaJASH MATHEWNo ratings yet

- Working Capital Management ProjectDocument45 pagesWorking Capital Management ProjectBarkhaNo ratings yet

- Research Paper On Working CapitalDocument7 pagesResearch Paper On Working CapitalRujuta ShahNo ratings yet

- Optimize Working Capital ManagementDocument8 pagesOptimize Working Capital ManagementAnnapurna VinjamuriNo ratings yet

- Chaitanya Chemicals - Capital Structure - 2018Document82 pagesChaitanya Chemicals - Capital Structure - 2018maheshfbNo ratings yet

- Working Capital ManagementDocument78 pagesWorking Capital ManagementDrj Maz50% (2)

- Working Capital Project ReportDocument87 pagesWorking Capital Project ReportPranay Raju RallabandiNo ratings yet

- Dimensions of Working Capital ManagementDocument22 pagesDimensions of Working Capital ManagementRamana Rao V GuthikondaNo ratings yet

- Prime Bank LTD Ratio AnalysisDocument30 pagesPrime Bank LTD Ratio Analysisrafey201No ratings yet

- Financial Performence of KesoramDocument97 pagesFinancial Performence of KesoramBasinepalli Sathish ReddyNo ratings yet

- Working Capital TheoryDocument24 pagesWorking Capital TheoryDivya SharmaNo ratings yet

- Banking & FinanceDocument15 pagesBanking & FinanceRiya ThakkarNo ratings yet

- Askari Bank Ratio AnalysisDocument32 pagesAskari Bank Ratio Analysis✬ SHANZA MALIK ✬No ratings yet

- Working CapitalDocument40 pagesWorking CapitalSupriya RajmaneNo ratings yet

- Working Capital ManagementDocument60 pagesWorking Capital ManagementyadNo ratings yet

- A Study of Capital Structure ManagementDocument94 pagesA Study of Capital Structure ManagementBijaya DhakalNo ratings yet

- Mba Project ReportDocument15 pagesMba Project ReportPreet GillNo ratings yet

- WORKING CAPITAL MANAGEMENTDocument70 pagesWORKING CAPITAL MANAGEMENTAnand SudarshanNo ratings yet

- A Study On "Portfolio Management"Document74 pagesA Study On "Portfolio Management"balki123No ratings yet

- Funds Flow Statement LancoDocument86 pagesFunds Flow Statement Lancothella deva prasadNo ratings yet

- Impact of Working Capital Management On The Profitability of The Food and Personal Care Products Companies Listed in Karachi Stock Exchange (Finance)Document41 pagesImpact of Working Capital Management On The Profitability of The Food and Personal Care Products Companies Listed in Karachi Stock Exchange (Finance)Muhammad Nawaz Khan Abbasi100% (1)

- "Working Capital of Management": A Project Report ONDocument31 pages"Working Capital of Management": A Project Report ONRohit BhorNo ratings yet

- REPORT On Venture CapitalDocument54 pagesREPORT On Venture Capitalakshay mouryaNo ratings yet

- Project On Working Capital ManagementDocument59 pagesProject On Working Capital ManagementMotasim ParkarNo ratings yet

- Project Report on Working Capital ManagementDocument35 pagesProject Report on Working Capital Managementomprakash shindeNo ratings yet

- Project ReportDocument57 pagesProject ReportPAWAR0015No ratings yet

- Assets Andliability Management at Icici Bank-1Document73 pagesAssets Andliability Management at Icici Bank-1akshuNo ratings yet

- Comparative Study On Working Capital Management. at Bhilai Steel by Anil SinghDocument86 pagesComparative Study On Working Capital Management. at Bhilai Steel by Anil Singhsattu_luvNo ratings yet

- A Study On Cash Mangement at Dabur India PVT LTDDocument25 pagesA Study On Cash Mangement at Dabur India PVT LTDSanthu SaravananNo ratings yet

- Merger & Acquisition PROJECTDocument49 pagesMerger & Acquisition PROJECTYUSUF DABONo ratings yet

- Risk Return Analysis Analysis of Banking and FMCG StocksDocument93 pagesRisk Return Analysis Analysis of Banking and FMCG StocksbhagathnagarNo ratings yet

- Capital Structure of Banking Companies in IndiaDocument21 pagesCapital Structure of Banking Companies in IndiaAbhishek Soni43% (7)

- Working Capital ManagementDocument78 pagesWorking Capital ManagementPriya GowdaNo ratings yet

- HDFC Bank CAMELS AnalysisDocument15 pagesHDFC Bank CAMELS Analysisprasanthgeni22No ratings yet

- Employee Job Satisfaction at Ellaquai Dehati BankDocument64 pagesEmployee Job Satisfaction at Ellaquai Dehati BankSwyam DuggalNo ratings yet

- Critical Review of Working Capital ManagementDocument99 pagesCritical Review of Working Capital ManagementSTAR PRINTINGNo ratings yet

- IFRS Standards OverviewDocument12 pagesIFRS Standards OverviewJeneef JoshuaNo ratings yet

- A Project Report On Financing SsiDocument70 pagesA Project Report On Financing SsihirwanithakurNo ratings yet

- Working Capital MGTDocument61 pagesWorking Capital MGTDinesh Kumar100% (1)

- Akash 123Document44 pagesAkash 123praveshNo ratings yet

- Mergers and Acquisitions in Indian Banking SectorDocument68 pagesMergers and Acquisitions in Indian Banking SectorPooja gawaiNo ratings yet

- Comparing Working Capital Management of Chemical and Medicine CompaniesDocument17 pagesComparing Working Capital Management of Chemical and Medicine CompaniesEmi KhanNo ratings yet

- Working Capital Management of SectrixDocument50 pagesWorking Capital Management of SectrixsectrixNo ratings yet

- 3.2 Components of Working CapitalDocument24 pages3.2 Components of Working CapitalShahid Shaikh100% (1)

- Working Capital OriginalDocument53 pagesWorking Capital Originalaurorashiva1100% (1)

- Review of Literature PriyaDocument3 pagesReview of Literature Priyadeepusrajan75% (4)

- Project Report ON Working Capital Management IN Bharti Airtel LTDDocument84 pagesProject Report ON Working Capital Management IN Bharti Airtel LTDRam LalNo ratings yet

- Cash Conversion CycleDocument18 pagesCash Conversion CycleRashidul HasanNo ratings yet

- Fsa - IciciDocument85 pagesFsa - IciciMOHAMMED KHAYYUMNo ratings yet

- Project Report Accounting & Finance Under The University of Calcutta)Document49 pagesProject Report Accounting & Finance Under The University of Calcutta)Rakesh SahNo ratings yet

- The Four Walls: Live Like the Wind, Free, Without HindrancesFrom EverandThe Four Walls: Live Like the Wind, Free, Without HindrancesRating: 5 out of 5 stars5/5 (1)

- Pepsi Project ReportDocument74 pagesPepsi Project ReportShams SNo ratings yet

- Data Analysis QWLDocument40 pagesData Analysis QWLShams SNo ratings yet

- DerivativesDocument75 pagesDerivativesDowlathAhmedNo ratings yet

- Samsung Galaxy Brand ImageDocument63 pagesSamsung Galaxy Brand ImageShams SNo ratings yet

- Questionnaire OlayDocument1 pageQuestionnaire OlayShams S100% (1)

- Hero Satisfaction ProjDocument59 pagesHero Satisfaction ProjShams S100% (2)

- Ratio AnalysisDocument64 pagesRatio AnalysisShams SNo ratings yet

- Mouryaa Inn ProfileDocument9 pagesMouryaa Inn ProfileShams SNo ratings yet

- Recruitment QuestionnaireDocument2 pagesRecruitment QuestionnaireShams SNo ratings yet

- Loans and AdvancesDocument64 pagesLoans and AdvancesShams SNo ratings yet

- Types of LoansDocument5 pagesTypes of LoansShams SNo ratings yet

- Advance Spoken EnglishDocument1 pageAdvance Spoken EnglishShams SNo ratings yet

- Factors Influencing Deposit Mobilisation in Rural AreasDocument2 pagesFactors Influencing Deposit Mobilisation in Rural AreasShams SNo ratings yet

- Nokia Cust Rela MGMTDocument71 pagesNokia Cust Rela MGMTShams SNo ratings yet

- Andhra Pragathi Grameena BankDocument1 pageAndhra Pragathi Grameena BankShams SNo ratings yet

- Tata Gluco PlusDocument9 pagesTata Gluco PlusShams S100% (1)

- Cust Satisfaction ArielDocument32 pagesCust Satisfaction ArielShams SNo ratings yet

- Honda Activa MileageDocument7 pagesHonda Activa MileageShams SNo ratings yet

- Findings and SuggestionsDocument2 pagesFindings and SuggestionsShams SNo ratings yet

- LG LED TVs ProjDocument62 pagesLG LED TVs ProjShams S100% (1)

- Hero Satisfaction ProjDocument59 pagesHero Satisfaction ProjShams S100% (2)

- Cust Satisfaction ArielDocument32 pagesCust Satisfaction ArielShams SNo ratings yet

- Customer Satisfaction Towards Nokia MobilesDocument49 pagesCustomer Satisfaction Towards Nokia MobilesShams S100% (1)

- FY 2022 April 20 2022 Comptroller LetterDocument18 pagesFY 2022 April 20 2022 Comptroller LetterHelen BennettNo ratings yet

- Government Budgeting and Accounting ClassificationDocument4 pagesGovernment Budgeting and Accounting ClassificationAndini OleyNo ratings yet

- Components of Government BudgetDocument7 pagesComponents of Government BudgetAditi MahaleNo ratings yet

- Chapter 3 FinmanDocument11 pagesChapter 3 FinmanJullia BelgicaNo ratings yet

- Financial Statement Analysis of SonyDocument13 pagesFinancial Statement Analysis of SonyJOHN VL FANAINo ratings yet

- Chapter-3: Restructuring & Responsibility Matrix in BSNLDocument13 pagesChapter-3: Restructuring & Responsibility Matrix in BSNLsfdwhjNo ratings yet

- O/W: Mayne To Reward The Willing: Mayne Pharma Group (MYX)Document8 pagesO/W: Mayne To Reward The Willing: Mayne Pharma Group (MYX)Muhammad ImranNo ratings yet

- Manual on New Government Accounting System for LGUsDocument107 pagesManual on New Government Accounting System for LGUsJhopel Casagnap Eman100% (1)

- Feedback:: Financial StatementsDocument9 pagesFeedback:: Financial StatementsMlndsamoraNo ratings yet

- FINANCE CYCLE - Chart of Accounts: Within The Chart of Accounts, You Will Find That The Accounts Are Typically Listed inDocument5 pagesFINANCE CYCLE - Chart of Accounts: Within The Chart of Accounts, You Will Find That The Accounts Are Typically Listed inQueen ValleNo ratings yet

- A Study On Financial Products Provided by My Money MantraDocument18 pagesA Study On Financial Products Provided by My Money Mantrasivagami100% (1)

- A1119166710 24805 14 2019 RatioAnalysisDocument96 pagesA1119166710 24805 14 2019 RatioAnalysisAshish kumar ThapaNo ratings yet

- Chapter - 1-Accounting For InventoriesDocument40 pagesChapter - 1-Accounting For InventoriesWonde BiruNo ratings yet

- ACTIVITY 8 - Intermediate AccountingDocument2 pagesACTIVITY 8 - Intermediate AccountingMicky BernalNo ratings yet

- A Study of Performance Evaluation OF Top 6 Indian BanksDocument12 pagesA Study of Performance Evaluation OF Top 6 Indian BanksKeval PatelNo ratings yet

- Lesson 4 Financial Ratio AnalysisDocument22 pagesLesson 4 Financial Ratio AnalysisLyza Jayne OliquianoNo ratings yet

- Project Report On Vimal Oils and Foods Ltd.Document62 pagesProject Report On Vimal Oils and Foods Ltd.yash0% (2)

- NDNE Retailer Guidelines For Uploading 121011Document17 pagesNDNE Retailer Guidelines For Uploading 121011Raghavendra K GowdaNo ratings yet

- Corporate Finance Week 5 Slide SolutionsDocument3 pagesCorporate Finance Week 5 Slide SolutionsKate BNo ratings yet

- ch01 PDFDocument59 pagesch01 PDFsaad bin saadaqatNo ratings yet

- A Critical Review in Constructal Theory PDFDocument12 pagesA Critical Review in Constructal Theory PDFRui GalvaniNo ratings yet

- China Wire Cable Market ReportDocument10 pagesChina Wire Cable Market ReportAllChinaReports.comNo ratings yet

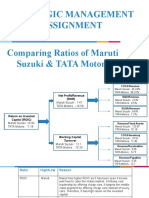

- Strategic Management Assignment Comparing Ratios of Maruti Suzuki & TATA MotorsDocument4 pagesStrategic Management Assignment Comparing Ratios of Maruti Suzuki & TATA MotorsNamanNo ratings yet

- 14 A Study On Financial Performance of Ponlait, PuducherryDocument69 pages14 A Study On Financial Performance of Ponlait, PuducherrySaravanan Sankari40% (5)

- LRWC Press Statement: Leisure and Resorts World CorporationDocument3 pagesLRWC Press Statement: Leisure and Resorts World CorporationJun GomezNo ratings yet

- f2 Financial Accounting April 2016Document20 pagesf2 Financial Accounting April 2016Edson Jorge MandlateNo ratings yet

- Ch1 4e - Acc in Action 2021Document50 pagesCh1 4e - Acc in Action 2021K59 Vu Thi Thu HienNo ratings yet