You might also like

- United States District Court Southern District of Ohio Western DivisionDocument14 pagesUnited States District Court Southern District of Ohio Western DivisionJamesNo ratings yet

- Foreign Policy Containment Final EssayDocument6 pagesForeign Policy Containment Final EssayAndrea WisniewskiNo ratings yet

- Repatriation of ProfitDocument3 pagesRepatriation of ProfitUmang KatochNo ratings yet

- Monetary Authority of SingaporeDocument29 pagesMonetary Authority of Singaporerahulchoudhury32No ratings yet

- World Bank Report 2007Document197 pagesWorld Bank Report 2007GlennKesslerWPNo ratings yet

- Regulating Philippine Stevedoring Companies as Public UtilitiesDocument6 pagesRegulating Philippine Stevedoring Companies as Public Utilitiesmarie janNo ratings yet

- Prevent Money Laundering with Correspondent Banking ComplianceDocument6 pagesPrevent Money Laundering with Correspondent Banking CompliancePradeep YadavNo ratings yet

- The Fraud Exception in Bank GuaranteesDocument86 pagesThe Fraud Exception in Bank Guaranteestiendung0390No ratings yet

- Receivers Second Interim Report Regading Status of ReceivershipDocument26 pagesReceivers Second Interim Report Regading Status of ReceivershipcburnellNo ratings yet

- Important Guidelines On Guarantees and Co-AcceptancesDocument16 pagesImportant Guidelines On Guarantees and Co-AcceptancesMd Jahirul Islam RaselNo ratings yet

- Manjoorsa, Krith Mounir, C. Block B ANCHETA v. GUERSEY-DALAYGON GR NO. 139868 (Rule 77)Document1 pageManjoorsa, Krith Mounir, C. Block B ANCHETA v. GUERSEY-DALAYGON GR NO. 139868 (Rule 77)KeithMounirNo ratings yet

- Lee v. RepublicDocument12 pagesLee v. RepublicPrincess MadaniNo ratings yet

- OFAC Blocked Property GuidanceDocument3 pagesOFAC Blocked Property GuidanceRonald WederfoortNo ratings yet

- Court rules expired license invalidates car insurance claimDocument2 pagesCourt rules expired license invalidates car insurance claimHuzzain PangcogaNo ratings yet

- Source of Funds ComplianceDocument2 pagesSource of Funds ComplianceAnonymous MddQJywVNo ratings yet

- Declaration of Finances 2015 HULTDocument4 pagesDeclaration of Finances 2015 HULTChristofel MauriNo ratings yet

- Asset Recovery Offices (Aros) : Jill Thomas Specialist Europol Criminal Assets BureauDocument23 pagesAsset Recovery Offices (Aros) : Jill Thomas Specialist Europol Criminal Assets BureauMary Rose BaluranNo ratings yet

- Amendments to the Usury Law Increase Interest Rate CeilingsDocument4 pagesAmendments to the Usury Law Increase Interest Rate CeilingsJulian Paul CachoNo ratings yet

- Aml Policy StatementDocument3 pagesAml Policy StatementekowahyudiNo ratings yet

- Anti Money Laaundering Act of 2001 RA 9160 PDFDocument7 pagesAnti Money Laaundering Act of 2001 RA 9160 PDFErica MailigNo ratings yet

- Succession: New Civil Code of The PhilippinesDocument182 pagesSuccession: New Civil Code of The PhilippinesSherlock HolmesNo ratings yet

- UnionBank 2018 Annual Report Highlights Key DevelopmentsDocument295 pagesUnionBank 2018 Annual Report Highlights Key Developmentsnancy delos santosNo ratings yet

- New Central Bank ActDocument39 pagesNew Central Bank ActdollyccruzNo ratings yet

- Order Approving The Settlement and Release Agreement by and Between The Trustee and IBMDocument15 pagesOrder Approving The Settlement and Release Agreement by and Between The Trustee and IBMSCO vs. IBMNo ratings yet

- 196 Rosario Textile Vs Home Bankers, 462 SCRA 88 (2005)Document1 page196 Rosario Textile Vs Home Bankers, 462 SCRA 88 (2005)Alan GultiaNo ratings yet

- Letters of Credit Digest-Trust Receipts LawDocument3 pagesLetters of Credit Digest-Trust Receipts LawLeo Angelo LuyonNo ratings yet

- Interview Question Answer For KYC AML Profile 1677153332Document13 pagesInterview Question Answer For KYC AML Profile 1677153332shivali guptaNo ratings yet

- Pay Vs PalancaDocument2 pagesPay Vs PalancaGeorge AlmedaNo ratings yet

- Considerations For Those Seeking Removal From The OFAC SDN ListDocument1 pageConsiderations For Those Seeking Removal From The OFAC SDN ListErich FerrariNo ratings yet

- Suan Chian Vs Alcantara, Braganza V Villa-AbrilleDocument3 pagesSuan Chian Vs Alcantara, Braganza V Villa-AbrilleKole GervacioNo ratings yet

- Howey Test (Security Law)Document12 pagesHowey Test (Security Law)Samruddhi ShindeNo ratings yet

- Characteristics of SuccessionDocument36 pagesCharacteristics of Successionaisha20101954No ratings yet

- Guidance Paper On Combating Trade-Based Money LaunderingDocument27 pagesGuidance Paper On Combating Trade-Based Money LaunderingManchesterCF100% (1)

- Rule 120Document6 pagesRule 120Valjim PacatangNo ratings yet

- US Documents Resource Guides Guide To US AML Requirements 5thedition ProtivitiDocument474 pagesUS Documents Resource Guides Guide To US AML Requirements 5thedition ProtivitiDev KhemaniNo ratings yet

- Saudi Airlines Appeals Court Ruling on Flight Attendant's TerminationDocument4 pagesSaudi Airlines Appeals Court Ruling on Flight Attendant's Terminationrafaelturtle_ninjaNo ratings yet

- Regulation of trust receipts transactionsDocument5 pagesRegulation of trust receipts transactionsMyna Zosette MesiasNo ratings yet

- Different Types of Letter of CreditDocument2 pagesDifferent Types of Letter of CreditAnilesh TewariNo ratings yet

- FEATI BANK vs. COURT OF APPEALSDocument1 pageFEATI BANK vs. COURT OF APPEALSJan Mar Gigi GallegoNo ratings yet

- Legitimes V Intestacy TableDocument2 pagesLegitimes V Intestacy TableJames Francis VillanuevaNo ratings yet

- Money Laundering Report - FinalDocument49 pagesMoney Laundering Report - Finalkalyan9746960% (1)

- A Marriage LicenseDocument1 pageA Marriage LicenseElla QuiNo ratings yet

- Bank Not Liable for Non-Compliance with Letter of Credit TermsDocument4 pagesBank Not Liable for Non-Compliance with Letter of Credit TermsCleinJonTiuNo ratings yet

- History of Laws On Insolvency and FRIADocument244 pagesHistory of Laws On Insolvency and FRIAShieldon Vic Senajon PinoonNo ratings yet

- TCC Amla HandoutDocument4 pagesTCC Amla HandoutVince TarucNo ratings yet

- BDO PersonalLoanAKAppliFormDocument4 pagesBDO PersonalLoanAKAppliFormAirMan ManiagoNo ratings yet

- Amor-Catalan Vs CADocument1 pageAmor-Catalan Vs CAMama MiaNo ratings yet

- Affidavit of Insurance ClaimDocument1 pageAffidavit of Insurance Claimzee pNo ratings yet

- 'PH Bank Secrecy Laws Strictest in The World Along With LebanonDocument12 pages'PH Bank Secrecy Laws Strictest in The World Along With LebanonjealousmistressNo ratings yet

- Study of Foreign Exchange Remittances and Interbank DealingsDocument95 pagesStudy of Foreign Exchange Remittances and Interbank DealingsSachin KajaveNo ratings yet

- National Bank of Ethiopia - Directives No. SBB-46-2010 - Customer Due Diligence of BanksDocument10 pagesNational Bank of Ethiopia - Directives No. SBB-46-2010 - Customer Due Diligence of Banksarefayne wodajoNo ratings yet

- Loan Agreement Interest DisputeDocument100 pagesLoan Agreement Interest Dispute2CNo ratings yet

- Banco Filipino Savings and Mortgage Bank v. Monetary BoardDocument5 pagesBanco Filipino Savings and Mortgage Bank v. Monetary BoardElayne MarianoNo ratings yet

- Prisma Vs MenchavezDocument1 pagePrisma Vs Menchaveztaktak69No ratings yet

- 2631-3008 (Tab C Exs. 94 (G-O) (PUBLIC)Document378 pages2631-3008 (Tab C Exs. 94 (G-O) (PUBLIC)GriswoldNo ratings yet

- Registration of Foreign Adoption Decree UpheldDocument2 pagesRegistration of Foreign Adoption Decree Upheldmonica may ramosNo ratings yet

- Philippine Bank Ordered to Pay Dividend After Failed Wire TransferDocument1 pagePhilippine Bank Ordered to Pay Dividend After Failed Wire TransferJaysonNo ratings yet

- BSP Circular No. 706Document8 pagesBSP Circular No. 706Unis BautistaNo ratings yet

- Anti-Money Laundering Act (AMLA) : RA 9160 As Amended by 9194, 10167, 10365 and 10927Document39 pagesAnti-Money Laundering Act (AMLA) : RA 9160 As Amended by 9194, 10167, 10365 and 10927NHASSER PASANDALANNo ratings yet

- MODULE 4 AMLA ACA Yap NJTCDocument13 pagesMODULE 4 AMLA ACA Yap NJTCJames Daniel PalmaNo ratings yet

- 1st Batch Sales-CompilationDocument4 pages1st Batch Sales-CompilationNeiseria AilahNo ratings yet

- LGCDocument127 pagesLGCNeiseria AilahNo ratings yet

- 1st Batch Sales-CompilationDocument4 pages1st Batch Sales-CompilationNeiseria AilahNo ratings yet

- Last Consolidated Case For ElectDocument12 pagesLast Consolidated Case For ElectNeiseria AilahNo ratings yet

- Our Moral DutyDocument3 pagesOur Moral DutyNeiseria AilahNo ratings yet

- Reviwer Part 1Document3 pagesReviwer Part 1Neiseria AilahNo ratings yet

- Transmission Request FormDocument4 pagesTransmission Request FormVinayak SavanurNo ratings yet

- Bank Alfalah Limited: That Appear in Reliable Third-Party PublicationsDocument15 pagesBank Alfalah Limited: That Appear in Reliable Third-Party PublicationsChanchal KuriNo ratings yet

- WEEK 3 Jobs in Accounting PDFDocument2 pagesWEEK 3 Jobs in Accounting PDFdaniNo ratings yet

- Business Contacts OctoberDocument15 pagesBusiness Contacts OctoberDurban Chamber of Commerce and IndustryNo ratings yet

- Emerging Trends in Financial ServicesDocument2 pagesEmerging Trends in Financial ServicesAlok Ranjan100% (1)

- Accounting Sample QuestionsDocument6 pagesAccounting Sample QuestionsScholarsjunction.comNo ratings yet

- Internal Control in Micro FinanceDocument5 pagesInternal Control in Micro Financeroymehuli91% (11)

- A Beautiful Mind With A Big MouthDocument328 pagesA Beautiful Mind With A Big MouthAbdul ArifNo ratings yet

- Snapdeal 170329070435Document24 pagesSnapdeal 170329070435Sumon BeraNo ratings yet

- Coinbase UK and CB Payments User Agreement 14 March 2018 PDFDocument37 pagesCoinbase UK and CB Payments User Agreement 14 March 2018 PDFLiezel DahotoyNo ratings yet

- New Government Accounting SystemDocument65 pagesNew Government Accounting SystemRuel Villanueva100% (1)

- Gurvinder Brar - Text MiningDocument28 pagesGurvinder Brar - Text Miningxy053333No ratings yet

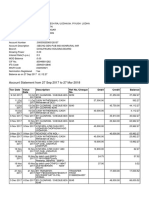

- Account statement details for Mr. Chandresh Raj LodhaDocument3 pagesAccount statement details for Mr. Chandresh Raj LodhaHemlata LodhaNo ratings yet

- QMS ProposalDocument22 pagesQMS Proposalflawlessy2kNo ratings yet

- Bacungan V CaDocument2 pagesBacungan V CaJoy Margaret Maniego RituaNo ratings yet

- An Introduction To Credibility TheoryDocument28 pagesAn Introduction To Credibility TheoryadauNo ratings yet

- In House Bank Suite5Document2 pagesIn House Bank Suite5ssahu1979No ratings yet

- Transaction History (Standard & Credit Card) Exported From Fastnet Business To OfxDocument11 pagesTransaction History (Standard & Credit Card) Exported From Fastnet Business To OfxchpradeepNo ratings yet

- An Elementary Explanation of MoneyDocument7 pagesAn Elementary Explanation of MoneyrooseveltkyleNo ratings yet

- Activate ISD BSNL PrepaidDocument2 pagesActivate ISD BSNL PrepaidJitesh AgarwalNo ratings yet

- NAFSCOB-Branch OperationsDocument379 pagesNAFSCOB-Branch OperationsAshoak VarmaNo ratings yet

- Kode BankDocument4 pagesKode BankMaha D NugrohoNo ratings yet

- Certificate of Existence Group and Ind AnnuityDocument1 pageCertificate of Existence Group and Ind AnnuityRajesh MukkavilliNo ratings yet

- Unit-1 Introduction To Indian Banking SystemDocument40 pagesUnit-1 Introduction To Indian Banking SystemKruti BhattNo ratings yet

- Universal Banking HDFCDocument16 pagesUniversal Banking HDFCrajesh bathulaNo ratings yet

- Payroll Direct DepositDocument1 pagePayroll Direct Depositumang parmarNo ratings yet

- Bailment Bond and Eft Over LetterDocument7 pagesBailment Bond and Eft Over LetterNikki Cofield100% (10)

- Problem 10 and 13Document2 pagesProblem 10 and 13jiiNo ratings yet

- Project On Bajaj AllianceDocument76 pagesProject On Bajaj Alliancekiran_mallana_gowda79% (19)

- IBPS Exam Details: Dates, Eligibility, Selection ProcessDocument3 pagesIBPS Exam Details: Dates, Eligibility, Selection ProcessNikhil KumarNo ratings yet