You might also like

- Ocean Carriers Case StudyDocument7 pagesOcean Carriers Case Studyaida100% (1)

- Ocean Carriers Case Study ReportDocument3 pagesOcean Carriers Case Study ReportUsama Farooq0% (1)

- Ocean Carriers Capesize Ship Project AnalysisDocument10 pagesOcean Carriers Capesize Ship Project AnalysisScottMeltonNo ratings yet

- OC Group evaluates new capsize shipDocument5 pagesOC Group evaluates new capsize shipGeorge Kolbaia80% (5)

- Ocean Carriers 2020 - A5Document10 pagesOcean Carriers 2020 - A5Mohith ChowdharyNo ratings yet

- Final Ocean Carriers Case ReportDocument7 pagesFinal Ocean Carriers Case ReportStefanoAquilinoNo ratings yet

- Ocean CarriersDocument7 pagesOcean CarriersAvinash ChoudharyNo ratings yet

- Ocean Carriers Case StudyDocument5 pagesOcean Carriers Case StudyJennifer Johnson71% (17)

- Ocean Carriers Reports - Final Case SolutionDocument9 pagesOcean Carriers Reports - Final Case SolutionNadia VirkNo ratings yet

- Ocean CarriersDocument3 pagesOcean CarrierswoheduoleyetuNo ratings yet

- Ocean Carriers Case StudyDocument7 pagesOcean Carriers Case StudyaidaNo ratings yet

- Ocean Carries HBS Case StudyDocument4 pagesOcean Carries HBS Case StudyRatul EsrarNo ratings yet

- Ocean Carriers Capsize Vessel Investment AnalysisDocument5 pagesOcean Carriers Capsize Vessel Investment AnalysisflwgearNo ratings yet

- OceanCarriers KenDocument24 pagesOceanCarriers KensaaaruuuNo ratings yet

- Overview of Ocean Carriers CaseDocument2 pagesOverview of Ocean Carriers CaseIrakli SaliaNo ratings yet

- Lecture Note 6 (Case Ocean Carrier)Document25 pagesLecture Note 6 (Case Ocean Carrier)Jing Zhou100% (1)

- Case 1 Ocean CarrierDocument15 pagesCase 1 Ocean CarrierAngeline WangNo ratings yet

- Case Study Ocean CarriersDocument5 pagesCase Study Ocean Carriersmetzor100% (4)

- Ocean Carriers FinalDocument4 pagesOcean Carriers FinalBilal AsifNo ratings yet

- Ocean Carrier CaseDocument17 pagesOcean Carrier CasechiaweesengNo ratings yet

- Ocean CarriersDocument17 pagesOcean CarriersMridula Hari33% (3)

- Ocean CarriersDocument26 pagesOcean Carriersclassmate0% (1)

- Ocean Carriers - Final SheetDocument2 pagesOcean Carriers - Final SheetandroidDownloadOnly100% (2)

- Ocean CarriersDocument3 pagesOcean CarriersHarita KuppaNo ratings yet

- Ocean Carriers MemoDocument2 pagesOcean Carriers MemoAnkush SaraffNo ratings yet

- 25 Years Use Tax ScenarioDocument14 pages25 Years Use Tax ScenarioToshalina Nayak50% (4)

- Ocean Carriers ExerciseDocument13 pagesOcean Carriers ExercisesafderNo ratings yet

- Ocean - Carriers Revised 2011Document7 pagesOcean - Carriers Revised 2011Prashant MishraNo ratings yet

- Ocean Carriers Assignment 1: Should Ms Linn purchase the $39M capsizeDocument6 pagesOcean Carriers Assignment 1: Should Ms Linn purchase the $39M capsizeJayzie LiNo ratings yet

- Lex Service PLCDocument3 pagesLex Service PLCMinu RoyNo ratings yet

- Sampa Video Financial Projections and AssumptionsDocument10 pagesSampa Video Financial Projections and AssumptionskanabaramitNo ratings yet

- Corporate Valuation: Group - 2Document6 pagesCorporate Valuation: Group - 2RiturajPaulNo ratings yet

- AirThread Valuation MethodsDocument21 pagesAirThread Valuation MethodsSon NguyenNo ratings yet

- Flash Memory, Inc.Document2 pagesFlash Memory, Inc.Stella Zukhbaia0% (5)

- ClarksonDocument2 pagesClarksonYang Pu100% (3)

- Midland Energy Case StudyDocument5 pagesMidland Energy Case StudyLokesh GopalakrishnanNo ratings yet

- Midland Energy Resources WACC20052006Average$11.4B/$18.3B = $13.2B/$21.4B = $14.6B/$24.2B =62.3%61.7%60.3%61.5Document13 pagesMidland Energy Resources WACC20052006Average$11.4B/$18.3B = $13.2B/$21.4B = $14.6B/$24.2B =62.3%61.7%60.3%61.5killer dramaNo ratings yet

- Midland Energy Resources (Final)Document4 pagesMidland Energy Resources (Final)satherbd21100% (3)

- Economy Shipping Co Case SolutionDocument7 pagesEconomy Shipping Co Case SolutionPaco Colín100% (2)

- UK Gilts CalculationsDocument10 pagesUK Gilts CalculationsAditee100% (1)

- Midland Energy Case StudyDocument5 pagesMidland Energy Case Studyrun2win645100% (7)

- Calaveras VineyardsDocument12 pagesCalaveras Vineyardsapi-250891173100% (4)

- Airthread ValuationDocument19 pagesAirthread Valuation45ss28No ratings yet

- AirThread ValuationDocument6 pagesAirThread ValuationShilpi Jain0% (6)

- Ameritrade Case SolutionDocument34 pagesAmeritrade Case SolutionAbhishek GargNo ratings yet

- MW Petroleum Corporation (A)Document6 pagesMW Petroleum Corporation (A)AnandNo ratings yet

- Economy Shipping Case AnswersDocument72 pagesEconomy Shipping Case Answersreduay67% (3)

- Ocean CarriersDocument2 pagesOcean CarriersRini RafiNo ratings yet

- AnalysisDocument2 pagesAnalysisZhieh LorNo ratings yet

- Ocean Carriers Case: Executive SummaryDocument5 pagesOcean Carriers Case: Executive SummarykokoNo ratings yet

- Group18 OceanCarrierDocument2 pagesGroup18 OceanCarrierSAHILNo ratings yet

- Case Study: Ocean Carriers Inc.: Members Team: TitanicDocument9 pagesCase Study: Ocean Carriers Inc.: Members Team: TitanicAnkitNo ratings yet

- Ocean Carriers Project EvaluationDocument5 pagesOcean Carriers Project Evaluationsaaaruuu0% (1)

- Ocean Carrier Investment AnalysisDocument8 pagesOcean Carrier Investment AnalysisStefanoNo ratings yet

- Ocean Carriers Project AnalysisDocument11 pagesOcean Carriers Project AnalysisSameer KumarNo ratings yet

- Second-Hand Vs New Building - The Better OptionDocument5 pagesSecond-Hand Vs New Building - The Better OptionNikos Noulezas100% (2)

- OCBC Asia Credit - Offshore Marine Sector - Many Moving Parts (11 Mar 2015) PDFDocument14 pagesOCBC Asia Credit - Offshore Marine Sector - Many Moving Parts (11 Mar 2015) PDFInvest StockNo ratings yet

- Capesized BrainsDocument7 pagesCapesized Brainsreluca11No ratings yet

- Rating Methodology For Shipping CompaniesDocument7 pagesRating Methodology For Shipping CompaniesprasadcshettyNo ratings yet

- BIMBSec - Oil Gas News Flash 20120709Document3 pagesBIMBSec - Oil Gas News Flash 20120709Bimb SecNo ratings yet

- TT06 - QuesDocument3 pagesTT06 - QuesLe Tuong MinhNo ratings yet

- FAR Test BankDocument17 pagesFAR Test BankMa. Efrelyn A. BagayNo ratings yet

- External Sources of Finance Long TermDocument2 pagesExternal Sources of Finance Long Termabrar mahir SahilNo ratings yet

- Assignment #2Document3 pagesAssignment #2Chad OngNo ratings yet

- Financing Disbursement Master Roll: B0685 Malapatan RegularDocument18 pagesFinancing Disbursement Master Roll: B0685 Malapatan RegularAsa Ph MalapatanNo ratings yet

- Final Askari ReportDocument110 pagesFinal Askari ReportjindjaanNo ratings yet

- Financial Statements: Statement of Profit or Loss and Other Comprehensive Income DR CRDocument8 pagesFinancial Statements: Statement of Profit or Loss and Other Comprehensive Income DR CRTawanda Tatenda HerbertNo ratings yet

- Targeting Presentation Nov' 07Document15 pagesTargeting Presentation Nov' 07Shashank SahuNo ratings yet

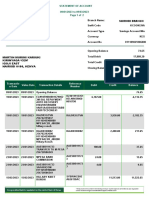

- Martin Murimi KariukiDocument2 pagesMartin Murimi KariukiKameneja LeeNo ratings yet

- Pas 21-The Effects of Changes in Foreign Exchange RatesDocument3 pagesPas 21-The Effects of Changes in Foreign Exchange RatesAryan LeeNo ratings yet

- Ratio Analysis Of: Bata Shoe Company (BD) LTDDocument19 pagesRatio Analysis Of: Bata Shoe Company (BD) LTDMonjur HasanNo ratings yet

- Accountancy For Lawyers - Practice QuestionsDocument3 pagesAccountancy For Lawyers - Practice QuestionsNantege ProssielyNo ratings yet

- Debt Limit Letter To Congress 20210928Document2 pagesDebt Limit Letter To Congress 20210928ZerohedgeNo ratings yet

- Receivable Financing: Pledge, Assignment and FactoringDocument35 pagesReceivable Financing: Pledge, Assignment and FactoringMARY GRACE VARGASNo ratings yet

- ACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamDocument41 pagesACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamNathalie Faye TajaNo ratings yet

- BDB Annual Report 2021 - Part - 4Document111 pagesBDB Annual Report 2021 - Part - 42023149467No ratings yet

- Finance areas interconnectionDocument3 pagesFinance areas interconnectionCASTOR, Vincent PaulNo ratings yet

- Final Accounts Without AdjustmentsDocument22 pagesFinal Accounts Without AdjustmentsFaizan MisbahuddinNo ratings yet

- Pledging of ReceivablesDocument2 pagesPledging of ReceivablesPrince Alexis GarciaNo ratings yet

- Applied Auditing Solution Manual Nginaescala AsuncionDocument166 pagesApplied Auditing Solution Manual Nginaescala AsuncionQuenn NavalNo ratings yet

- Functions and Effects of Money in an EconomyDocument71 pagesFunctions and Effects of Money in an Economysweet haniaNo ratings yet

- Fabm 1 LeapDocument4 pagesFabm 1 Leapanna paulaNo ratings yet

- CH 3 - Lap Konsolidasi PengantarDocument45 pagesCH 3 - Lap Konsolidasi PengantarJulia Pratiwi ParhusipNo ratings yet

- Agricultural Business ManagementDocument5 pagesAgricultural Business ManagementAreicra NutNo ratings yet

- Pakistan Stock Exchange Limited: Internet Trading Subscribers ListDocument3 pagesPakistan Stock Exchange Limited: Internet Trading Subscribers ListMuhammad AhmedNo ratings yet

- ECS1601 Chapter 16 Narrated Slides Foreign Sector Exchange RatesDocument31 pagesECS1601 Chapter 16 Narrated Slides Foreign Sector Exchange RatesConnor Van der MerweNo ratings yet

- Gainesboro Machine Tools Corporation: Other Cases in Which Dividend Policy Is An Important IssueDocument22 pagesGainesboro Machine Tools Corporation: Other Cases in Which Dividend Policy Is An Important IssueUshnaNo ratings yet

- American Economic Association The American Economic ReviewDocument9 pagesAmerican Economic Association The American Economic ReviewWazzupWorldNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument9 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceN.prem kumarNo ratings yet

- Equity YyyDocument33 pagesEquity YyyJude SantosNo ratings yet