You might also like

- PC01 Budget For July, Aug, Sep'2021Document45 pagesPC01 Budget For July, Aug, Sep'2021Ashish BhartiNo ratings yet

- Global ChangeDocument62 pagesGlobal ChangeAshish BhartiNo ratings yet

- 3.zero Cost 1,2,3,4 Mrts - Patna May 21Document62 pages3.zero Cost 1,2,3,4 Mrts - Patna May 21Ashish BhartiNo ratings yet

- To Patna: Delhi Metro Rail Corporation Limited NCC Company LimitedDocument1 pageTo Patna: Delhi Metro Rail Corporation Limited NCC Company LimitedAshish BhartiNo ratings yet

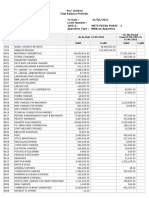

- Expenses As On 31.05.2021Document2 pagesExpenses As On 31.05.2021Ashish BhartiNo ratings yet

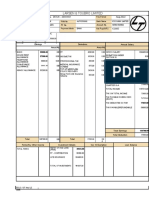

- Ra Bill Summary Mrts PatnaDocument2 pagesRa Bill Summary Mrts PatnaAshish BhartiNo ratings yet

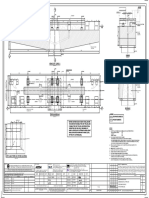

- Pile Cap Coordinates and DetailsDocument1 pagePile Cap Coordinates and DetailsAshish BhartiNo ratings yet

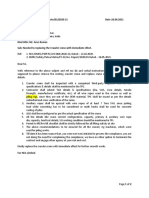

- Office Note For IB InfraDocument2 pagesOffice Note For IB InfraAshish BhartiNo ratings yet

- Mom 01.07.2021Document4 pagesMom 01.07.2021Ashish BhartiNo ratings yet

- To Patna: Delhi Metro Rail Corporation Limited NCC Company LimitedDocument1 pageTo Patna: Delhi Metro Rail Corporation Limited NCC Company LimitedAshish BhartiNo ratings yet

- DESIGN QA ASSURANCE DRAWINGDocument1 pageDESIGN QA ASSURANCE DRAWINGAshish BhartiNo ratings yet

- DESIGN QA ASSURANCE DRAWINGDocument1 pageDESIGN QA ASSURANCE DRAWINGAshish BhartiNo ratings yet

- Mom 01.07.2021Document4 pagesMom 01.07.2021Ashish BhartiNo ratings yet

- Global Change 1Document12 pagesGlobal Change 1Ashish BhartiNo ratings yet

- 11.VIE-PC01-STN-BHT-LSE-4007 (R2) L SECTION-Layout1Document1 page11.VIE-PC01-STN-BHT-LSE-4007 (R2) L SECTION-Layout1Ashish BhartiNo ratings yet

- 5.VIE-PC01-STN-BHT-CRS-4001 (R2) SECTION A-Layout1Document1 page5.VIE-PC01-STN-BHT-CRS-4001 (R2) SECTION A-Layout1Ashish BhartiNo ratings yet

- Khemni Chak to Zero Mile Station PlanDocument1 pageKhemni Chak to Zero Mile Station PlanAshish BhartiNo ratings yet

- Vie-Pc01-Stn-Bht-Cp-2001 (R2) Concourse LVL - Plan-Sh1Document1 pageVie-Pc01-Stn-Bht-Cp-2001 (R2) Concourse LVL - Plan-Sh1Ashish BhartiNo ratings yet

- Bridge design cross-sectionDocument1 pageBridge design cross-sectionAshish BhartiNo ratings yet

- Vie Pc01 STN DWG MP Ppa 01109 0Document1 pageVie Pc01 STN DWG MP Ppa 01109 0Ashish BhartiNo ratings yet

- Vie Pc01 STN DWG MP Sub 01151 0Document1 pageVie Pc01 STN DWG MP Sub 01151 0Ashish BhartiNo ratings yet

- 8.VIE-PC01-STN-BHT-CRS-4004 (R2) SECTION D-Layout1Document1 page8.VIE-PC01-STN-BHT-CRS-4004 (R2) SECTION D-Layout1Ashish BhartiNo ratings yet

- 9 .VIE-PC01-STN-BHT-CRS-4005 (R1) SECTION E-Layout1Document1 page9 .VIE-PC01-STN-BHT-CRS-4005 (R1) SECTION E-Layout1Ashish BhartiNo ratings yet

- Vie Pc01 STN DWG MP Sub 01101 0Document1 pageVie Pc01 STN DWG MP Sub 01101 0Ashish BhartiNo ratings yet

- Vie Pc01 STN DWG MP Ppa 01108 0Document1 pageVie Pc01 STN DWG MP Ppa 01108 0Ashish BhartiNo ratings yet

- 6.VIE-PC01-STN-BHT-CRS-4002 (R2) SECTION B-Layout1Document1 page6.VIE-PC01-STN-BHT-CRS-4002 (R2) SECTION B-Layout1Ashish BhartiNo ratings yet

- Vie Pc01 STN DWG MP FRP 01105 0Document1 pageVie Pc01 STN DWG MP FRP 01105 0Ashish BhartiNo ratings yet

- Vie Pc01 STN DWG MP Ppa 01107 0Document1 pageVie Pc01 STN DWG MP Ppa 01107 0Ashish BhartiNo ratings yet

- Directions to zero mile station from Khemni ChakDocument1 pageDirections to zero mile station from Khemni ChakAshish BhartiNo ratings yet

- 1.vie-Pc01-Stn-Bht-Fp-1001 (R1) Foundation LVL Plan-1001Document1 page1.vie-Pc01-Stn-Bht-Fp-1001 (R1) Foundation LVL Plan-1001Ashish BhartiNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Ultimate DIY BIR Tax Compliance Guide For Freelancers - November 2020 Version - 5 PDFDocument56 pagesThe Ultimate DIY BIR Tax Compliance Guide For Freelancers - November 2020 Version - 5 PDFKathrina BangayanNo ratings yet

- Accounting Information Systems Chapter 5 Discussion QuestionsDocument36 pagesAccounting Information Systems Chapter 5 Discussion QuestionspnharyonoNo ratings yet

- Project On Marketing Strategy of Asian PaintsDocument52 pagesProject On Marketing Strategy of Asian Paintsneenadmba100% (7)

- National Income - Definitions - Lovish KakkarDocument2 pagesNational Income - Definitions - Lovish KakkarAjuni ShahNo ratings yet

- Pre-construction project phases and processDocument1 pagePre-construction project phases and processGamini KodikaraNo ratings yet

- Local Media9055451308065624461Document73 pagesLocal Media9055451308065624461DigiTime Trading ShopNo ratings yet

- Retail Industry Terminology and IT TrendsDocument30 pagesRetail Industry Terminology and IT TrendsksnangethNo ratings yet

- Coca Cola ScriptDocument4 pagesCoca Cola ScriptMohammadIbrahimNo ratings yet

- 12 Points) : A B: Over Co de Ex Out Down Re Ultra UnderDocument2 pages12 Points) : A B: Over Co de Ex Out Down Re Ultra UnderRobert CalcanNo ratings yet

- Demolition Planning PDFDocument12 pagesDemolition Planning PDFimanbilly67% (3)

- Problems On Hire Purchase and LeasingDocument5 pagesProblems On Hire Purchase and Leasingprashanth mvNo ratings yet

- C300 Rim Vents: Tank AccessoriesDocument2 pagesC300 Rim Vents: Tank AccessoriesAs'adNo ratings yet

- Reliance Fresh ProjectDocument55 pagesReliance Fresh ProjectHaridra ShandilyaNo ratings yet

- PTV PresentationDocument80 pagesPTV PresentationAfshan SattiNo ratings yet

- SEBI Tightens Compliances and Disclosures For Listed Entities - Amends LODR RegulationsDocument16 pagesSEBI Tightens Compliances and Disclosures For Listed Entities - Amends LODR RegulationsELP LawNo ratings yet

- AFS SolutionsDocument19 pagesAFS SolutionsRolivhuwaNo ratings yet

- XII - Bahasa InggrisDocument12 pagesXII - Bahasa InggrisBosgas GadingNo ratings yet

- Assignment: DR Shazia RehmanDocument10 pagesAssignment: DR Shazia Rehmanumbreen100% (1)

- Cold Storage RFP DocsDocument26 pagesCold Storage RFP DocsHaripriya BNo ratings yet

- Draft Invoice - Zuba CafeDocument1 pageDraft Invoice - Zuba Cafechandanprakash30No ratings yet

- August 2022Document1 pageAugust 2022amitdesai92No ratings yet

- ENT300 - Business Opportunity (UiTM)Document10 pagesENT300 - Business Opportunity (UiTM)asta yuno100% (1)

- Rent AggreementDocument5 pagesRent AggreementUtkarsh KhandelwalNo ratings yet

- HPA 14 Assignemnt Due November 16thDocument5 pagesHPA 14 Assignemnt Due November 16thcNo ratings yet

- Multinational Business Finance 14th Edition Eiteman Test BankDocument24 pagesMultinational Business Finance 14th Edition Eiteman Test BankJamesAndersongoki100% (26)

- Exercises 1 To 10Document11 pagesExercises 1 To 10Nicolas KuiperNo ratings yet

- The 9 Concepts of Corporate GovernanceDocument15 pagesThe 9 Concepts of Corporate GovernanceChan Tsu Chong100% (5)

- Incorporating Social Aspects in Sustainable Supply Chains - Trends and Future DirectionsDocument35 pagesIncorporating Social Aspects in Sustainable Supply Chains - Trends and Future DirectionsAnaNo ratings yet

- Ahmad 2007Document19 pagesAhmad 2007Vesna RodicNo ratings yet

- Malunggay WineDocument13 pagesMalunggay WineMika PatocNo ratings yet