You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Mary Anne Malubay MacavintaDocument1 pageMary Anne Malubay MacavintaMARY ANNE M. SAN JOSENo ratings yet

- Firestone Vs CADocument2 pagesFirestone Vs CAHoward TuanquiNo ratings yet

- Mrunal Handout Complied PDFDocument290 pagesMrunal Handout Complied PDFhirdyanshuNo ratings yet

- ABC's Cash and Cash Equivalents on December 31, 2019Document5 pagesABC's Cash and Cash Equivalents on December 31, 2019Clariz Angelika EscocioNo ratings yet

- Statement of Axis Account No:917010039768564 For The Period (From: 12-01-2020 To: 12-08-2020)Document5 pagesStatement of Axis Account No:917010039768564 For The Period (From: 12-01-2020 To: 12-08-2020)Dr. DUSHYANTH N DNo ratings yet

- Automated Teller MachineDocument20 pagesAutomated Teller MachineRathna Kumar SelvarajNo ratings yet

- Business Model of A Bank Through Business Canvas ModelDocument3 pagesBusiness Model of A Bank Through Business Canvas ModelAyush Jaiswal50% (2)

- 79.02 - Trinidad and Tobago Central Bank ActDocument80 pages79.02 - Trinidad and Tobago Central Bank ActOilmanGHNo ratings yet

- 11 Quiz 1 (Trade)Document2 pages11 Quiz 1 (Trade)Melanie PermijoNo ratings yet

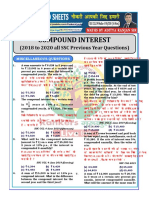

- Compound Interest: (2018 To 2020 All SSC Previous Year Questions)Document17 pagesCompound Interest: (2018 To 2020 All SSC Previous Year Questions)HakjsNo ratings yet

- LiborDocument28 pagesLiborRupesh ShahNo ratings yet

- Yes First Eclectic Debit Card SocDocument2 pagesYes First Eclectic Debit Card Socraghav mehraNo ratings yet

- Mortgage Paper For Math 1030 Final DraftDocument6 pagesMortgage Paper For Math 1030 Final Draftapi-192510247No ratings yet

- Nurul Jannah Binti Rossli Stament Bank 2Document7 pagesNurul Jannah Binti Rossli Stament Bank 2nurul jannah rossliNo ratings yet

- Chapter 2 - Nominal and Effective Interest RatesDocument16 pagesChapter 2 - Nominal and Effective Interest RatesTanveer Ahmed HakroNo ratings yet

- Bank charges schedule breakdownDocument26 pagesBank charges schedule breakdownMaria FayyazNo ratings yet

- POS Class Diagram PDFDocument1 pagePOS Class Diagram PDFSaad HassanNo ratings yet

- Kunal Jain 29589438528759262180371182184Document1 pageKunal Jain 29589438528759262180371182184trav baeNo ratings yet

- Checking Summary: David Johnson 8233 Tomlinson CT SEVERN MD 21144Document3 pagesChecking Summary: David Johnson 8233 Tomlinson CT SEVERN MD 21144jeffery lamarNo ratings yet

- CAMEL Ratios ExplainedDocument2 pagesCAMEL Ratios Explainedsrinath121No ratings yet

- Account Type / Jenis Akaun: Borang Permohonan Membuka Akaun - Komersial / KorporatDocument5 pagesAccount Type / Jenis Akaun: Borang Permohonan Membuka Akaun - Komersial / KorporatCik NurNo ratings yet

- Crest Slb&Repo SettlementsDocument41 pagesCrest Slb&Repo SettlementsGroucho32No ratings yet

- Detailed Statement: SearchDocument12 pagesDetailed Statement: SearchsikkaNo ratings yet

- MARQUEE-JKT-MF102 VO Registration Form - 6 December 2022 (Rev 4)Document1 pageMARQUEE-JKT-MF102 VO Registration Form - 6 December 2022 (Rev 4)Muhammad ChoiruddinNo ratings yet

- Screenshot 2023-06-23 at 11.12.58 AMDocument13 pagesScreenshot 2023-06-23 at 11.12.58 AMR P CNo ratings yet

- NIC Asia (Repaired)Document55 pagesNIC Asia (Repaired)Dikshita Shrestha67% (3)

- Account Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 1 Mar 2023 To 31 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSuresh VatipalliNo ratings yet

- Cigi Membership Form 2022Document1 pageCigi Membership Form 2022Uday MongaNo ratings yet

- Ayala Coop loan guidelinesDocument2 pagesAyala Coop loan guidelinesLiza SebastianNo ratings yet

- Kami Export - Depository Institutions Note Taking Guide 2 2 1 l1 PDFDocument2 pagesKami Export - Depository Institutions Note Taking Guide 2 2 1 l1 PDFapi-296019366No ratings yet