You might also like

- ReitDocument2 pagesReitvivekNo ratings yet

- Karvy - Case - Detailed ExplanationDocument2 pagesKarvy - Case - Detailed ExplanationANSHUL SINGH PARIHARNo ratings yet

- Non Banking Financial CompaniesDocument20 pagesNon Banking Financial CompaniesLav Chaudhary0% (1)

- Investment BankingDocument17 pagesInvestment BankingDhananjay BiyalaNo ratings yet

- Ipo OrderDocument252 pagesIpo Orderapi-3701467No ratings yet

- DuPont analysis breakdown of ROEDocument3 pagesDuPont analysis breakdown of ROEChirag JainNo ratings yet

- Reits - Vinod KothariDocument52 pagesReits - Vinod KothariRuchita SenNo ratings yet

- Ipo ProcessDocument19 pagesIpo ProcessDeepa KawaraniNo ratings yet

- Credit Rating Services, Types, Advantages, Agencies & MethodologyDocument28 pagesCredit Rating Services, Types, Advantages, Agencies & Methodologyak5775No ratings yet

- Ratios - Session3 ReadingDocument4 pagesRatios - Session3 Readingshashwatnirma50% (2)

- NBFC CrisisDocument12 pagesNBFC CrisisvikuNo ratings yet

- Case Study Barclays FinalDocument13 pagesCase Study Barclays FinalShalini Senglo RajaNo ratings yet

- Sbi Capital Market Investment BankDocument13 pagesSbi Capital Market Investment BankdineshNo ratings yet

- IL&FS Default AnalysisDocument28 pagesIL&FS Default Analysisanuj rakhejaNo ratings yet

- Karvy Scam 1801106Document2 pagesKarvy Scam 1801106Manjeet Sagar100% (1)

- Anand RathiDocument27 pagesAnand RathiRicha56No ratings yet

- Made By: Akshay VirkarDocument19 pagesMade By: Akshay Virkarakshay virkarNo ratings yet

- Aim IndiaDocument10 pagesAim Indiaapoorva100% (1)

- Types of Mutual FundDocument3 pagesTypes of Mutual FundKhunt DadhichiNo ratings yet

- HMC Case Study on Inflation Linked BondsDocument29 pagesHMC Case Study on Inflation Linked BondsFast TalkerNo ratings yet

- The Structure and Functions of The Federal Reserve System: Policy, Banking Supervision, Financial ServicesDocument18 pagesThe Structure and Functions of The Federal Reserve System: Policy, Banking Supervision, Financial ServicesJapish MehtaNo ratings yet

- A Study On Wealth Creation (1993-98)Document20 pagesA Study On Wealth Creation (1993-98)vinod kumar maddineniNo ratings yet

- REITs and InvITsDocument17 pagesREITs and InvITsSai YvstNo ratings yet

- Corporate finance group work analysis and WACC calculationsDocument15 pagesCorporate finance group work analysis and WACC calculationscaglar ozyesilNo ratings yet

- BCG Classics Revisited The Growth Share Matrix Jun 2014 Tcm80-162923Document9 pagesBCG Classics Revisited The Growth Share Matrix Jun 2014 Tcm80-162923NITINNo ratings yet

- Regulatory Framework of M&ADocument5 pagesRegulatory Framework of M&ARaghuramNo ratings yet

- Times Mirror - Group-2 Section ADocument4 pagesTimes Mirror - Group-2 Section AManu Shivanand0% (1)

- Investment in Equities Versus Investment in Mutual FundDocument37 pagesInvestment in Equities Versus Investment in Mutual FundBob PanjabiNo ratings yet

- Corporate Valuation 9-9-12Document50 pagesCorporate Valuation 9-9-12pradeepbandiNo ratings yet

- Overview of Corporate Banking and Wholesale Lending ModelsDocument75 pagesOverview of Corporate Banking and Wholesale Lending ModelsNarinder BhasinNo ratings yet

- Comparative Analysis of Mutual Funds - Kotak SecuritiesDocument6 pagesComparative Analysis of Mutual Funds - Kotak SecuritiesVasavi DaramNo ratings yet

- SEBI Guidelines On IPODocument17 pagesSEBI Guidelines On IPOSachin SinghNo ratings yet

- A Study On Mergers and Acquisitions of Indian Banking SectorDocument9 pagesA Study On Mergers and Acquisitions of Indian Banking SectorEditor IJTSRDNo ratings yet

- Stock ExchangeDocument8 pagesStock ExchangeNayan kakiNo ratings yet

- Mutual Funds Vs Gold Saving FundsDocument19 pagesMutual Funds Vs Gold Saving Fundschaluvadiin100% (1)

- Swap RatioDocument11 pagesSwap RatioVaibhav Singla100% (1)

- Api Holdings Limited: (Pharmeasy)Document21 pagesApi Holdings Limited: (Pharmeasy)Rohan RautelaNo ratings yet

- HEDGE FUND TITLEDocument71 pagesHEDGE FUND TITLEfgersgtesrtgeNo ratings yet

- Minibond Series 35Document58 pagesMinibond Series 35Ben JoneNo ratings yet

- Case 1 - Term Sheet Negotiations For Trendsetter Inc. Group 3Document10 pagesCase 1 - Term Sheet Negotiations For Trendsetter Inc. Group 3Avanish Nagar 23No ratings yet

- IIFL Special Opportunities Fund Series 2 PresentationDocument21 pagesIIFL Special Opportunities Fund Series 2 PresentationKrishna ShambhuNo ratings yet

- Merchant BankingDocument19 pagesMerchant BankingMiral PatelNo ratings yet

- Alternative Investment FundsDocument10 pagesAlternative Investment Fundskrishna sharmaNo ratings yet

- Direct Equity Investing and Mutual Fund InvestingDocument116 pagesDirect Equity Investing and Mutual Fund Investingmoula nawazNo ratings yet

- Research PaperDocument13 pagesResearch PaperShuvajit BhattacharyyaNo ratings yet

- Working Capital & Dividend PolicyDocument9 pagesWorking Capital & Dividend PolicyLipi Singal0% (1)

- The IPO Process in IndiaDocument13 pagesThe IPO Process in IndiaManish IngaleNo ratings yet

- Avenue Supermart AnalysisDocument394 pagesAvenue Supermart Analysisashish.forgetmenotNo ratings yet

- IFDocument12 pagesIFVikas ShegalNo ratings yet

- Thomas Weisel Partners Case StudyDocument1 pageThomas Weisel Partners Case StudyHEM BANSALNo ratings yet

- HDFC - Company Analysis - SAMNIDHY INSTAGRAM - 4 PDFDocument10 pagesHDFC - Company Analysis - SAMNIDHY INSTAGRAM - 4 PDFAsanga KumarNo ratings yet

- 1-Equity Research - Introduction PDFDocument3 pages1-Equity Research - Introduction PDFAindrila SilNo ratings yet

- Radnet, Inc.: Financing An Acquisition: Rev. May 20, 2014Document22 pagesRadnet, Inc.: Financing An Acquisition: Rev. May 20, 2014Luisa FernandaNo ratings yet

- Tata Consultancy Services IPO AnalysisDocument13 pagesTata Consultancy Services IPO AnalysisAmartya Dey0% (1)

- IMPACT OF FOREIGN INSTITUTIONAL INVESTORS (FIIs) AND MACRO ECONOMIC FACTORS ON INDIAN STOCK MARKETSDocument27 pagesIMPACT OF FOREIGN INSTITUTIONAL INVESTORS (FIIs) AND MACRO ECONOMIC FACTORS ON INDIAN STOCK MARKETSece_shreyas100% (2)

- Alternative Investment Strategies A Complete Guide - 2020 EditionFrom EverandAlternative Investment Strategies A Complete Guide - 2020 EditionNo ratings yet

- FARDocument1 pageFARmssidhu88No ratings yet

- FARDocument1 pageFARmssidhu88No ratings yet

- TDEEDocument38 pagesTDEEmssidhu88No ratings yet

- As DebtModification TLDocument48 pagesAs DebtModification TLmssidhu88No ratings yet

- Greenlight Capital 2014 Q4 Investor Letter by Insider MonkeyDocument7 pagesGreenlight Capital 2014 Q4 Investor Letter by Insider Monkeymssidhu88No ratings yet

- Ifrs and Us Gaap Similarities and Differences 2014Document224 pagesIfrs and Us Gaap Similarities and Differences 2014Naveed Mughal AcmaNo ratings yet

- Marking To Market: How Far Is Far Enough?: Fair Value in Financial ReportingDocument8 pagesMarking To Market: How Far Is Far Enough?: Fair Value in Financial ReportingAndrie WijayaNo ratings yet

- Financialreportingdevelopments Bb2438 Debtandequity 5june2014Document480 pagesFinancialreportingdevelopments Bb2438 Debtandequity 5june2014mssidhu88No ratings yet

- EY Global Private Equity Watch 2014Document28 pagesEY Global Private Equity Watch 2014mssidhu88No ratings yet

- Proposed Amended ComplaintDocument56 pagesProposed Amended ComplaintNallur SethuramanNo ratings yet

- EY-Private Equity Roundup China Q4 2013Document16 pagesEY-Private Equity Roundup China Q4 2013mssidhu88No ratings yet

- Cowboys Full James McManusDocument0 pagesCowboys Full James McManuscata_alex_muntNo ratings yet

- Ed Marlo - FingerTip Control PDFDocument11 pagesEd Marlo - FingerTip Control PDFOmar Sayoumit100% (1)

- DfadfDocument1 pageDfadfmssidhu88No ratings yet

- Unlocking Value Hidden Real Estate HoldingsDocument16 pagesUnlocking Value Hidden Real Estate Holdingsmssidhu88No ratings yet

- IntroductionDocument3 pagesIntroductionkenya11No ratings yet

- Sto 16.69 150 2,503.50 Tot 48.73 50 2,436.50 Sto 18.58 150 2,787.00 Tot 49.02 50 2,451.00 Sto 17.64 300 5,290.50 Tot 48.88 100 4,887.50Document2 pagesSto 16.69 150 2,503.50 Tot 48.73 50 2,436.50 Sto 18.58 150 2,787.00 Tot 49.02 50 2,451.00 Sto 17.64 300 5,290.50 Tot 48.88 100 4,887.50mssidhu88No ratings yet

- Cowboys Full James McManusDocument0 pagesCowboys Full James McManuscata_alex_muntNo ratings yet

- Prompt 2Document1 pagePrompt 2mssidhu88No ratings yet

- DfadfDocument1 pageDfadfmssidhu88No ratings yet

- WoolworthsDocument55 pagesWoolworthsjohnsmithlovestodo69No ratings yet

- Alphabet 2014 Financial ReportDocument6 pagesAlphabet 2014 Financial ReportsharatjuturNo ratings yet

- M1 M5 Forex Scalping Trading Strategy PDFDocument9 pagesM1 M5 Forex Scalping Trading Strategy PDFzooor100% (1)

- Bhel Ratio AnalysisDocument5 pagesBhel Ratio AnalysisPuja AryaNo ratings yet

- 7EelrUukRlC290knhHNO - NOAH18 Berlin Investor Book PDFDocument106 pages7EelrUukRlC290knhHNO - NOAH18 Berlin Investor Book PDFSaravanan RajaramNo ratings yet

- A Project Report On "Investment Environment For Shares in Belgaum"conducted For Geerak MarketingDocument67 pagesA Project Report On "Investment Environment For Shares in Belgaum"conducted For Geerak MarketingBabasab Patil (Karrisatte)No ratings yet

- Indian Capital MarketsDocument122 pagesIndian Capital MarketsVivek100% (4)

- CH 5Document10 pagesCH 5Miftahudin MiftahudinNo ratings yet

- Business CombinationsDocument43 pagesBusiness CombinationsCici AyuoctaviaNo ratings yet

- Modern Trader Media KitDocument14 pagesModern Trader Media KitBrianNo ratings yet

- Balance Sheet AuditDocument10 pagesBalance Sheet AuditFathiah HamidNo ratings yet

- SGX ASX MergerDocument12 pagesSGX ASX Merger靳雪娇No ratings yet

- Financial Institutions, Financial Instruments & Financial MarketDocument23 pagesFinancial Institutions, Financial Instruments & Financial MarketjudithNo ratings yet

- CH 2 ProbsDocument4 pagesCH 2 ProbsEnas FandosNo ratings yet

- Analysis of Foreign Financial Statements: Mcgraw-Hill/Irwin Rights ReservedDocument30 pagesAnalysis of Foreign Financial Statements: Mcgraw-Hill/Irwin Rights ReservedChuckNo ratings yet

- Corporate Valuation Model - Activision Blizzard IncDocument24 pagesCorporate Valuation Model - Activision Blizzard IncMichael Andres Gamarra TorresNo ratings yet

- Delisting Checklist PDFDocument4 pagesDelisting Checklist PDFsnjv2621No ratings yet

- MACD Histogram StrategyDocument12 pagesMACD Histogram StrategyElizabeth John RajNo ratings yet

- HUAWEIDocument18 pagesHUAWEIAswini Kumar BhuyanNo ratings yet

- Calculating WACC and Project NPV with Changing Floatation CostsDocument18 pagesCalculating WACC and Project NPV with Changing Floatation CostsYoga Pratama Rizki FNo ratings yet

- BKDP - Annual Report - 2018Document24 pagesBKDP - Annual Report - 2018galuh tri.pNo ratings yet

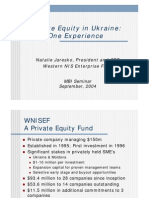

- WNISEF Experience in UkraineDocument21 pagesWNISEF Experience in UkraineVitaliy HamuhaNo ratings yet

- 22-Oct-2018 HDFC Mutual Fund Seeramsyamali 14232346/34: Scheme DetailsDocument1 page22-Oct-2018 HDFC Mutual Fund Seeramsyamali 14232346/34: Scheme DetailsSyamali SeeramNo ratings yet

- Limiting Factor AnalysisDocument5 pagesLimiting Factor AnalysisFaizan MotiwalaNo ratings yet

- Interim Order in The Matter of Togo Retail Marketing LimitedDocument16 pagesInterim Order in The Matter of Togo Retail Marketing LimitedShyam SunderNo ratings yet

- DerivaGem 2Document10 pagesDerivaGem 2Vicky RajoraNo ratings yet

- Lecture 6 1567834793996Document52 pagesLecture 6 1567834793996Jay ShuklaNo ratings yet

- p2Document8 pagesp2elizaNo ratings yet

- Cadbury Ratio AnalysisDocument11 pagesCadbury Ratio AnalysisShanza Maryam100% (1)

- Mock Test (Final Exam) KeyDocument4 pagesMock Test (Final Exam) KeyKhoa TrầnNo ratings yet