You might also like

- Reference For Advent, Simbang Gabi at PaskoDocument4 pagesReference For Advent, Simbang Gabi at PaskoVann Balingit100% (2)

- The United Nations Environment Programme and The 2030 Agenda PDFDocument8 pagesThe United Nations Environment Programme and The 2030 Agenda PDFVivianaNo ratings yet

- Buklod NG Pag-IbigDocument1 pageBuklod NG Pag-IbigTesa GD100% (1)

- America's Unknown Enemy - Beyond - American Institute For EconomicDocument155 pagesAmerica's Unknown Enemy - Beyond - American Institute For EconomicwestgenNo ratings yet

- Huwag Mangamba PDFDocument2 pagesHuwag Mangamba PDFTesa GD100% (1)

- Philippine Budget CycleDocument67 pagesPhilippine Budget CycleJessa Dela CruzNo ratings yet

- Ra 9710 Magna Carta For Women With Implementing Rules (Irr)Document133 pagesRa 9710 Magna Carta For Women With Implementing Rules (Irr)alm27ph57% (7)

- Appendix 76 - PTRDocument1 pageAppendix 76 - PTRTesa GD100% (2)

- 2017 9 Audit Observations and RecommendationsDocument79 pages2017 9 Audit Observations and RecommendationsKean Fernand BocaboNo ratings yet

- Secretary's Certificate TemplateDocument2 pagesSecretary's Certificate TemplateJanine Garcia100% (1)

- 139 Governmental Accounting HO PDFDocument6 pages139 Governmental Accounting HO PDFSankalp Singh100% (1)

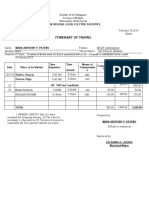

- Iterenary Travel FormDocument3 pagesIterenary Travel Formsplef lguNo ratings yet

- Withholding Taxes 2Document20 pagesWithholding Taxes 2hildaNo ratings yet

- Ang Tibay Vs CIRDocument2 pagesAng Tibay Vs CIRNyx PerezNo ratings yet

- SECTOR PERFORMANCE AND REVIEW (SPRDocument38 pagesSECTOR PERFORMANCE AND REVIEW (SPRRussel SarachoNo ratings yet

- Report On The Physical Count of Property, Plant and EquipmentDocument1 pageReport On The Physical Count of Property, Plant and EquipmentFeena Ritz Herly Baria0% (1)

- Govt & NFP Accounting - Ch2Document70 pagesGovt & NFP Accounting - Ch2Fãhâd Õró ÂhmédNo ratings yet

- Commission On Audit: of FQR L) IqilippiursDocument3 pagesCommission On Audit: of FQR L) IqilippiursDianeNo ratings yet

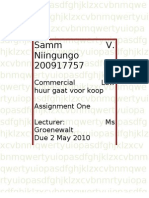

- Huur Gaat Voor Koop - FinalDocument17 pagesHuur Gaat Voor Koop - FinalSam_e_LeeJones_649380% (5)

- COA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsDocument6 pagesCOA Audit Finds Deficiencies in Collections of Bongabon Liga ng mga Barangay FundsJonson PalmaresNo ratings yet

- CIVIL SERVICE EXAM UPDATE 2023 With Answer Key 2,300 ItemsDocument302 pagesCIVIL SERVICE EXAM UPDATE 2023 With Answer Key 2,300 ItemsKuyaJemar GraphicNo ratings yet

- Guide To Filling Out The Personal Data SheetDocument7 pagesGuide To Filling Out The Personal Data SheetTesa GDNo ratings yet

- GNFP CH 3Document41 pagesGNFP CH 3Bilisummaa GeetahuunNo ratings yet

- CSC Memo Cir No. 2-2005Document35 pagesCSC Memo Cir No. 2-2005daniel besina jrNo ratings yet

- Accounting For Disbursements and Related TransactionsDocument12 pagesAccounting For Disbursements and Related TransactionsJustine GuilingNo ratings yet

- BUDGET AND FINANCIAL ACCOUNTABILITY REPORTS (BFARs)Document38 pagesBUDGET AND FINANCIAL ACCOUNTABILITY REPORTS (BFARs)tuffoman100% (1)

- The Local Government CodeDocument176 pagesThe Local Government CodeGracelyn Enriquez BellinganNo ratings yet

- Steps For EfpsDocument3 pagesSteps For EfpsMarites Domingo - PaquibulanNo ratings yet

- Scan App Review - CamScanner PDF ScannerDocument2 pagesScan App Review - CamScanner PDF ScannerTesa GD100% (5)

- Guidelines for Completing New IPCR FormDocument4 pagesGuidelines for Completing New IPCR FormCaryl FranceNo ratings yet

- RepertoireDocument2 pagesRepertoireTesa GDNo ratings yet

- JAIME GAPAYAO vs. JAIME FULODocument3 pagesJAIME GAPAYAO vs. JAIME FULOBert NazarioNo ratings yet

- TMAP - DOF-BLGF Policy UpdatesDocument35 pagesTMAP - DOF-BLGF Policy UpdatesPena Tn100% (1)

- NGAS: New Government Accounting SystemDocument56 pagesNGAS: New Government Accounting SystemVenianNo ratings yet

- Summary of Appropriations, Allotments, Obligations and Balances (SAAOBDocument2 pagesSummary of Appropriations, Allotments, Obligations and Balances (SAAOBthessa_starNo ratings yet

- 2018 AFR Local Govt Volume I PDFDocument453 pages2018 AFR Local Govt Volume I PDFRhuejane Gay Maquiling0% (1)

- UACS Manual for Financial ReportingDocument41 pagesUACS Manual for Financial ReportingHammurabi BugtaiNo ratings yet

- Appendix 30 - Instructions - RANCADocument1 pageAppendix 30 - Instructions - RANCApdmu regionixNo ratings yet

- Appraisal Report On Unserviceable IT EquipmentDocument2 pagesAppraisal Report On Unserviceable IT EquipmentAbraham JunioNo ratings yet

- Ngas Vol 1 To 6 Acctng PoliciesDocument184 pagesNgas Vol 1 To 6 Acctng PoliciesresurgumNo ratings yet

- 08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsDocument22 pages08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsGil DavinNo ratings yet

- Instructions On Reports of Disbursements FormDocument1 pageInstructions On Reports of Disbursements FormPayapa At Masaganang PamayananNo ratings yet

- Appendix 8 - Instructions - RAPALDocument1 pageAppendix 8 - Instructions - RAPALTesa GDNo ratings yet

- Budget AccountabilityDocument2 pagesBudget AccountabilityAi Ai Serna LawangonNo ratings yet

- Appendix 9B - Instructions - RAOD MOOEDocument1 pageAppendix 9B - Instructions - RAOD MOOETesa GDNo ratings yet

- Alpha ListDocument22 pagesAlpha ListArnold BaladjayNo ratings yet

- DDO Hand Book Part 2Document54 pagesDDO Hand Book Part 2Sajid AwanNo ratings yet

- BIR Revenue Memorandum Order 23 Full TextDocument9 pagesBIR Revenue Memorandum Order 23 Full TextImperator FuriosaNo ratings yet

- 62983rmo 5-2012Document14 pages62983rmo 5-2012Mark Dennis JovenNo ratings yet

- RCIDocument2 pagesRCIrussel1435100% (1)

- Uganda Public Finance Management Regulations, 2016Document24 pagesUganda Public Finance Management Regulations, 2016African Centre for Media Excellence100% (19)

- GPPB NPM 011-2010Document4 pagesGPPB NPM 011-2010Eric DykimchingNo ratings yet

- COA issues guidelines on cellular phone card allowanceDocument2 pagesCOA issues guidelines on cellular phone card allowancealiahNo ratings yet

- Annual Audit Report: Republic of The Philippines Commission On Audit Regional Office No. IX Zamboanga CityDocument8 pagesAnnual Audit Report: Republic of The Philippines Commission On Audit Regional Office No. IX Zamboanga CityJuan Luis LusongNo ratings yet

- DPWH Overtime PayDocument7 pagesDPWH Overtime PayTarhata KalimNo ratings yet

- 2K12 ARB-Lower DimalinaoDocument8 pages2K12 ARB-Lower DimalinaoJuan Luis LusongNo ratings yet

- Agency Action Plan to Address Audit ObservationsDocument9 pagesAgency Action Plan to Address Audit ObservationsRagnar LothbrokNo ratings yet

- 09-CalapanCity2019 Part2-Observations and RecommDocument55 pages09-CalapanCity2019 Part2-Observations and RecommkQy267BdTKNo ratings yet

- Enhanced Engas and Ebudget System Version 2.0 (Ppsas and Rca Compliant) For Local Government UnitDocument5 pagesEnhanced Engas and Ebudget System Version 2.0 (Ppsas and Rca Compliant) For Local Government UnitJayden CruzNo ratings yet

- Concept of Funds-Dr. Loida M. CancinoDocument81 pagesConcept of Funds-Dr. Loida M. CancinoAricirtap Abenoja JoyceNo ratings yet

- Pantar2014 Audit Report 3Document58 pagesPantar2014 Audit Report 3rain06021992No ratings yet

- 10 ACR InstructionsDocument69 pages10 ACR InstructionsMuhammadNo ratings yet

- Registry of Allotments and Notice of Transfer of Allocation: Appendix 31Document1 pageRegistry of Allotments and Notice of Transfer of Allocation: Appendix 31Tesa GDNo ratings yet

- Activity 4Document7 pagesActivity 4Genelyn LangoteNo ratings yet

- Withholding Tax RatesDocument35 pagesWithholding Tax RatesZonia Mae CuidnoNo ratings yet

- New Government Accounting System FeaturesDocument4 pagesNew Government Accounting System FeaturesabbiecdefgNo ratings yet

- Auditor OpinionDocument3 pagesAuditor OpinionAnkesh ShrivastavaNo ratings yet

- Local-Budget-Circular-No-132 2021Document18 pagesLocal-Budget-Circular-No-132 2021Lav Valdez Raza100% (1)

- Summary of Ifrs 6Document1 pageSummary of Ifrs 6Divine Epie Ngol'esueh100% (1)

- Saaodb 2014 1st QTRDocument2 pagesSaaodb 2014 1st QTRtesdaro12No ratings yet

- Report of Disbursement - 1st QuarterDocument2 pagesReport of Disbursement - 1st Quartertesdaro12No ratings yet

- Annex D Summary Report of Disbursements: ParticularsDocument2 pagesAnnex D Summary Report of Disbursements: ParticularsJeremiah TrinidadNo ratings yet

- Annex A: - Date: - DateDocument2 pagesAnnex A: - Date: - DateJeremiah TrinidadNo ratings yet

- Appendix 20 - Instructions - FAR No. 2Document2 pagesAppendix 20 - Instructions - FAR No. 2thessa_starNo ratings yet

- Appendix 21 - Instructions - FAR No. 2-ADocument2 pagesAppendix 21 - Instructions - FAR No. 2-Athessa_starNo ratings yet

- Huwag MangambaDocument2 pagesHuwag MangambaTesa GDNo ratings yet

- Living Rosary for Our Lady of AssumptionDocument1 pageLiving Rosary for Our Lady of AssumptionTesa GDNo ratings yet

- MemberChangeInformation V06Document2 pagesMemberChangeInformation V06joy barrameda50% (2)

- Additional Guidelines On The DepEd National Uniforms For Teaching and Non-Teaching PersonnelDocument12 pagesAdditional Guidelines On The DepEd National Uniforms For Teaching and Non-Teaching PersonnelDeped TambayanNo ratings yet

- Sapat Na Ang Diyos EPHDocument2 pagesSapat Na Ang Diyos EPHTesa GDNo ratings yet

- New Pagibig STLRF FormatDocument4 pagesNew Pagibig STLRF FormatTesa GDNo ratings yet

- Additional Guidelines On The DepEd National Uniforms For Teaching and Non-Teaching PersonnelDocument12 pagesAdditional Guidelines On The DepEd National Uniforms For Teaching and Non-Teaching PersonnelDeped TambayanNo ratings yet

- MemberChangeInformation V06Document2 pagesMemberChangeInformation V06joy barrameda50% (2)

- Pipe FitterDocument2 pagesPipe FitterTesa GDNo ratings yet

- NLEX lockdown alternate routes for conferenceDocument1 pageNLEX lockdown alternate routes for conferenceTesa GDNo ratings yet

- Corporate Budget Circular No 23Document7 pagesCorporate Budget Circular No 23Tesa GDNo ratings yet

- Teacher Transfer RequestsDocument40 pagesTeacher Transfer RequestsTesa GDNo ratings yet

- Registry of Allotments and Notice of Transfer of Allocation: Appendix 31Document1 pageRegistry of Allotments and Notice of Transfer of Allocation: Appendix 31Tesa GDNo ratings yet

- Marian SolemnitiesDocument4 pagesMarian SolemnitiesTesa GDNo ratings yet

- Appendix 36 - JEVDocument1 pageAppendix 36 - JEVTesa GDNo ratings yet

- Registry of Heritage Asset - SummaryDocument3 pagesRegistry of Heritage Asset - SummaryTesa GDNo ratings yet

- Pcne 4 PsalmDocument1 pagePcne 4 PsalmTesa GDNo ratings yet

- Meeting Planner ChecklistDocument3 pagesMeeting Planner ChecklistnombreclaudiaNo ratings yet

- Med Record Abstract FormDocument1 pageMed Record Abstract FormTesa GDNo ratings yet

- Appendix 7b - Rror-SagfDocument1 pageAppendix 7b - Rror-SagfEdwin Siruno LopezNo ratings yet

- Appendix 77 - CIPLCDocument1 pageAppendix 77 - CIPLCTesa GDNo ratings yet

- When Are Military Holidays in United States - Google SearchDocument1 pageWhen Are Military Holidays in United States - Google SearchNicholson SmithNo ratings yet

- 8th Circuit Oral Argument, Business Leaders in Christ v. University of IowaDocument50 pages8th Circuit Oral Argument, Business Leaders in Christ v. University of IowaThe College FixNo ratings yet

- Famous Trials of The Philippines The Gom 1Document7 pagesFamous Trials of The Philippines The Gom 1Josef Gelacio NuylesNo ratings yet

- Lagrosas V Brsitol Myers (GR 168637)Document2 pagesLagrosas V Brsitol Myers (GR 168637)Verlie FajardoNo ratings yet

- Addendum On The Bangsamoro Waters and Zones of Joint CooperationDocument1 pageAddendum On The Bangsamoro Waters and Zones of Joint CooperationOffice of the Presidential Adviser on the Peace ProcessNo ratings yet

- PADILLA JR Vs COMELECDocument1 pagePADILLA JR Vs COMELECVonNo ratings yet

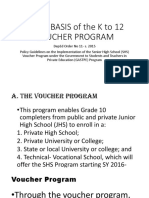

- K to 12 Voucher Program Legal BasisDocument9 pagesK to 12 Voucher Program Legal BasisLourdes Libo-onNo ratings yet

- Ch-8. Internal Economies of Scale and Trade (Krugman)Document12 pagesCh-8. Internal Economies of Scale and Trade (Krugman)দুর্বার নকিবNo ratings yet

- Retainer AgreementDocument1 pageRetainer AgreementAtty. Emmanuel SandichoNo ratings yet

- Board of Ed Agendas 2009 - 2010Document9 pagesBoard of Ed Agendas 2009 - 2010Hob151219!No ratings yet

- Saraswathy Rajamani || Woman Who Fooled British by Dressing as ManDocument11 pagesSaraswathy Rajamani || Woman Who Fooled British by Dressing as Manbasutk2055No ratings yet

- Annex A: MINUTES OF THE MEETING OF (Involved Committee, Technical Working GroupDocument2 pagesAnnex A: MINUTES OF THE MEETING OF (Involved Committee, Technical Working GroupJAYSON NECIDANo ratings yet

- SEIP Trainee Admission FormDocument2 pagesSEIP Trainee Admission FormRj IsratNo ratings yet

- Vaibhav Steel Corporation W.P.1735 of 2013 Dt.26.11.2013Document7 pagesVaibhav Steel Corporation W.P.1735 of 2013 Dt.26.11.2013sweetuhemuNo ratings yet

- Doug Ducey/Cold Stone Creamery Exploited Child Labor LawsDocument2 pagesDoug Ducey/Cold Stone Creamery Exploited Child Labor LawsBarbara EspinosaNo ratings yet

- Ffice of The Lerk: Elephone AcsimileDocument2 pagesFfice of The Lerk: Elephone AcsimileWBAYNo ratings yet

- The Doctrine of EclipseDocument12 pagesThe Doctrine of EclipseKanika Srivastava33% (3)

- PA Law Grants Promotions in Rank To Terrorist Prisoners From PA Security ServicesDocument4 pagesPA Law Grants Promotions in Rank To Terrorist Prisoners From PA Security ServicesKokoy JimenezNo ratings yet

- Precedents Concept and KindsDocument12 pagesPrecedents Concept and Kindsgagan deepNo ratings yet

- Application For Intimation and Transfer of Ownership of A Motor VehicleDocument3 pagesApplication For Intimation and Transfer of Ownership of A Motor VehicleAnanth KrishnaNo ratings yet

- BBC News - World War One 10 Interpretations of Who Started ww1Document4 pagesBBC News - World War One 10 Interpretations of Who Started ww1api-213324377No ratings yet

- Bangladesh Genocide of 1971Document33 pagesBangladesh Genocide of 1971Robert VeneziaNo ratings yet

- National Officers Academy: Mock Exams Special CSS & CSS-2024 August 2023 (Mock-5) International Relations, Paper-IiDocument1 pageNational Officers Academy: Mock Exams Special CSS & CSS-2024 August 2023 (Mock-5) International Relations, Paper-IiKiranNo ratings yet