You might also like

- Venus Petrochemicals BrochureDocument4 pagesVenus Petrochemicals BrochureorangeponyNo ratings yet

- Merchant Banking InsightsDocument78 pagesMerchant Banking InsightsorangeponyNo ratings yet

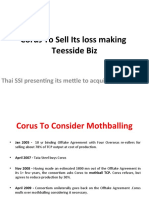

- Corus To Sell Its Loss Making Teesside Biz: Thai SSI Presenting Its Mettle To Acquire For $500 MNDocument7 pagesCorus To Sell Its Loss Making Teesside Biz: Thai SSI Presenting Its Mettle To Acquire For $500 MNorangeponyNo ratings yet

- Corus To Sell Its Loss Making Teesside Biz: Thai SSI Presenting Its Mettle To Acquire For $500 MNDocument7 pagesCorus To Sell Its Loss Making Teesside Biz: Thai SSI Presenting Its Mettle To Acquire For $500 MNorangeponyNo ratings yet

- A Study On Working Capital of Nagarjuna Fertilizers and Chemicals LTDDocument31 pagesA Study On Working Capital of Nagarjuna Fertilizers and Chemicals LTDorangeponyNo ratings yet

- CRISIL Ratings India Top 50 MfisDocument68 pagesCRISIL Ratings India Top 50 MfisDavid Raju GollapudiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Journal Entries: ACC111 Froilan LabausaDocument3 pagesJournal Entries: ACC111 Froilan LabausaDenise Ortiz ManolongNo ratings yet

- Sem6 RatioAnalysisLecture 6 JuhiJaiswal 19apr2020Document8 pagesSem6 RatioAnalysisLecture 6 JuhiJaiswal 19apr2020Hanabusa Kawaii IdouNo ratings yet

- AHTM 2007 - OpenDoors - PKDocument9 pagesAHTM 2007 - OpenDoors - PKWaleed KhalidNo ratings yet

- Chapter 23: Accounts Receivable and Inventory Management: I. True or False (Definitions and Concepts)Document20 pagesChapter 23: Accounts Receivable and Inventory Management: I. True or False (Definitions and Concepts)deiyan ballonNo ratings yet

- NFJPIA - Mockboard 2011 - AP PDFDocument6 pagesNFJPIA - Mockboard 2011 - AP PDFSteven Mark MananguNo ratings yet

- Irrecoverable Debts and Allowances For ReceivablesDocument20 pagesIrrecoverable Debts and Allowances For ReceivablesShayan KhanNo ratings yet

- 293-Article Text-1711-1-10-20230611Document14 pages293-Article Text-1711-1-10-20230611aera.aeoNo ratings yet

- Accounting Cycle HacksDocument14 pagesAccounting Cycle HacksAnonymous mnAAXLkYQCNo ratings yet

- Arias, Kyla Kim B. - Midterm Project Sept 30Document9 pagesArias, Kyla Kim B. - Midterm Project Sept 30Kyla Kim AriasNo ratings yet

- Ratio Analysis Theory and ProblemsDocument13 pagesRatio Analysis Theory and ProblemsPunit Kuleria100% (1)

- Explaining the 3 Main Financing Options of an Export OrderDocument8 pagesExplaining the 3 Main Financing Options of an Export OrderDiana SumailiNo ratings yet

- DemonstraDocument25 pagesDemonstraJBS RINo ratings yet

- ACCCOB2-Chapter 3 - RECEIVABLESDocument43 pagesACCCOB2-Chapter 3 - RECEIVABLESVan TisbeNo ratings yet

- Perpetual Periodic InventoryDocument4 pagesPerpetual Periodic InventoryJuvanni B. SabellaNo ratings yet

- AssignmentDocument3 pagesAssignmentFrancis Abuyuan100% (1)

- Afar.3202 Corporate LiquidationDocument6 pagesAfar.3202 Corporate Liquidationruel c armillaNo ratings yet

- Bank ReconciliationDocument6 pagesBank Reconciliationclarisse jaramillaNo ratings yet

- Chapter 2Document11 pagesChapter 2Tofik SalmanNo ratings yet

- 0452 s07 QP 3 PDFDocument20 pages0452 s07 QP 3 PDFAbirHudaNo ratings yet

- Recording Transactions: Using The Method of Journal EntriesDocument50 pagesRecording Transactions: Using The Method of Journal EntriesHasanAbdullah100% (1)

- Ex 3 Journal Entries Guide PDFDocument19 pagesEx 3 Journal Entries Guide PDFShashank MallepulaNo ratings yet

- Cash Flow Kunci BaruDocument1 pageCash Flow Kunci BaruDyah WinengkuNo ratings yet

- Cash and Accrual BasisDocument24 pagesCash and Accrual BasisAlexa LeeNo ratings yet

- AFAR Notes by Dr. Ferrer PDFDocument21 pagesAFAR Notes by Dr. Ferrer PDFjexNo ratings yet

- Working Cap MGMT Questions SolutionDocument13 pagesWorking Cap MGMT Questions SolutionElin SaldañaNo ratings yet

- Chapter 7 Business Transactions and Their AnalysisDocument14 pagesChapter 7 Business Transactions and Their Analysisrmm0415No ratings yet

- Yogesh Naik (Project)Document68 pagesYogesh Naik (Project)yogeshnaik06100% (1)

- Accounting Principles CH 03 + 04 ExamDocument7 pagesAccounting Principles CH 03 + 04 ExamJames MorganNo ratings yet

- 9 Liquid Asset ManagementDocument26 pages9 Liquid Asset Managementadib nassarNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument21 pagesAccounting Cycle of A Merchandising Businesszedrick edenNo ratings yet