You might also like

- BIR Ruling No. 291-12 Dated 04.25.2012 PDFDocument5 pagesBIR Ruling No. 291-12 Dated 04.25.2012 PDFJerwin DaveNo ratings yet

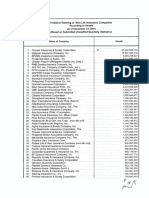

- Ranking NL Assets2015Document2 pagesRanking NL Assets2015Jerwin DaveNo ratings yet

- Life - According To Assets - Year 2014Document1 pageLife - According To Assets - Year 2014Jerwin DaveNo ratings yet

- Ias12 StandardDocument40 pagesIas12 StandardKay BookNo ratings yet

- BIR Ruling (DA-031-07)Document2 pagesBIR Ruling (DA-031-07)Jerwin Dave100% (4)

- Notes TtraDocument2 pagesNotes TtraJerwin DaveNo ratings yet

- Notes TtraDocument2 pagesNotes TtraJerwin DaveNo ratings yet

- RR No. 13-94Document13 pagesRR No. 13-94Jerwin DaveNo ratings yet

- DA-087-08 - No CAR For Any Personal PropertiesDocument2 pagesDA-087-08 - No CAR For Any Personal PropertiesJerwin DaveNo ratings yet

- BIR Ruling 302-08 - Funeral AssistanceDocument13 pagesBIR Ruling 302-08 - Funeral AssistanceJerwin DaveNo ratings yet

- BIR Ruling 173-99 - Sale or Transfer of Motor VehiclesDocument2 pagesBIR Ruling 173-99 - Sale or Transfer of Motor VehiclesJerwin Dave100% (1)

- 2010 - 2017 Executive OrdersDocument457 pages2010 - 2017 Executive OrdersJerwin DaveNo ratings yet

- Comparison Between Operating Lease and Finance LeaseDocument1 pageComparison Between Operating Lease and Finance LeaseJerwin DaveNo ratings yet

- 2003 ITAD RulingsDocument511 pages2003 ITAD RulingsJerwin DaveNo ratings yet

- 2004 ITAD RulingsDocument464 pages2004 ITAD RulingsJerwin DaveNo ratings yet

- DA (C337) 818-09 - Liquidating DivDocument6 pagesDA (C337) 818-09 - Liquidating DivJerwin DaveNo ratings yet

- ITAD BIR Ruling 375-15 - Guarantee LoansDocument17 pagesITAD BIR Ruling 375-15 - Guarantee LoansJerwin DaveNo ratings yet

- 2000 ITAD RulingsDocument409 pages2000 ITAD RulingsJerwin DaveNo ratings yet

- 2007 ITAD Rulings - Delegated AuthorityDocument413 pages2007 ITAD Rulings - Delegated AuthorityJerwin DaveNo ratings yet

- DA ITAD BIR Ruling 017-09 - Interest Income Tax Sparing Rule SingaporeDocument9 pagesDA ITAD BIR Ruling 017-09 - Interest Income Tax Sparing Rule SingaporeJerwin DaveNo ratings yet

- 2001 ITAD RulingsDocument306 pages2001 ITAD RulingsJerwin DaveNo ratings yet

- 2006 ITAD Rulings - Delegated AuthorityDocument537 pages2006 ITAD Rulings - Delegated AuthorityJerwin DaveNo ratings yet

- 2005 ITAD RulingsDocument461 pages2005 ITAD RulingsJerwin DaveNo ratings yet

- 2002 ITAD RulingsDocument587 pages2002 ITAD RulingsJerwin DaveNo ratings yet

- BIR Rulings (2017 - 2018)Document2,631 pagesBIR Rulings (2017 - 2018)Jerwin DaveNo ratings yet

- BIR Ruling 302-08 - Funeral AssistanceDocument13 pagesBIR Ruling 302-08 - Funeral AssistanceJerwin DaveNo ratings yet

- BIR Ruling 383-15 - Dividends Received by Luxembourg Entity (Participation Exemption)Document5 pagesBIR Ruling 383-15 - Dividends Received by Luxembourg Entity (Participation Exemption)Jerwin DaveNo ratings yet

- 1999 ITAD RulingsDocument97 pages1999 ITAD RulingsJerwin DaveNo ratings yet

- DA-402-07 - Restricted Stock Award Under A Stock Incentive PlanDocument4 pagesDA-402-07 - Restricted Stock Award Under A Stock Incentive PlanJerwin DaveNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Empirical Analysis of Agricultural Exports and Economic Growth in NigeriaDocument10 pagesThe Empirical Analysis of Agricultural Exports and Economic Growth in NigeriaYusif AxundovNo ratings yet

- Taxation and Development: Mick MoooreDocument39 pagesTaxation and Development: Mick MoooreKimberly Joy LungayNo ratings yet

- The Rentier State in The Middle EastDocument34 pagesThe Rentier State in The Middle EastbengersonNo ratings yet

- Rentier StatesDocument9 pagesRentier Statesapi-281122860No ratings yet

- Analysis of "Why The Modest Harvest?"Document3 pagesAnalysis of "Why The Modest Harvest?"Dylan Schaffer100% (1)

- Politics and The Natural Resource Curse Evidence From Selected African StatesDocument18 pagesPolitics and The Natural Resource Curse Evidence From Selected African StatesWendmagegn Assefa RasNo ratings yet

- The Role of Tribal and Kinship Ties in The Politics of The United Arab EmiratesDocument24 pagesThe Role of Tribal and Kinship Ties in The Politics of The United Arab Emiratesamin ChenNo ratings yet

- Does Oil Hinder Democracy?Document38 pagesDoes Oil Hinder Democracy?darkzielNo ratings yet

- After The Sheikhs - The Coming Collapse of The Gulf Monarchies (PDFDrive)Document1,275 pagesAfter The Sheikhs - The Coming Collapse of The Gulf Monarchies (PDFDrive)Amine KronNo ratings yet

- Book Reviews On Hallaq's Impossible StateDocument18 pagesBook Reviews On Hallaq's Impossible StateNazmus Sakib NirjhorNo ratings yet

- O Ocidente Diz Adeus Ao Capitalismo IndustrialDocument31 pagesO Ocidente Diz Adeus Ao Capitalismo IndustrialMarcelo AraújoNo ratings yet

- Corruption in Nigeria's Oil and Gas Industry Extent and Macroeconomic Impact, 1981-2014Document156 pagesCorruption in Nigeria's Oil and Gas Industry Extent and Macroeconomic Impact, 1981-2014nnubiaNo ratings yet

- 11 S Implication-InterferenceDocument50 pages11 S Implication-InterferenceLe Minh ThanhNo ratings yet

- Spaces of PostdevelopmentDocument18 pagesSpaces of PostdevelopmentfjtoroNo ratings yet

- Oil-Led Development: Social, Political, and Economic ConsequencesDocument12 pagesOil-Led Development: Social, Political, and Economic ConsequencesVíctor SalmerónNo ratings yet

- M.Phil Modern Middle Eastern Studies Political Economy PaperDocument16 pagesM.Phil Modern Middle Eastern Studies Political Economy PaperalexandramihaiNo ratings yet

- Energy Security and The Resource Curse in Nigeria - Docx 2Document47 pagesEnergy Security and The Resource Curse in Nigeria - Docx 2Oreoluwa Asanmo100% (1)

- Globalization and Social Change' in The GCC SocietiesDocument17 pagesGlobalization and Social Change' in The GCC SocietiesKundan Kumar100% (3)

- Ross 2001 - Does Oil Hinder DemocracyDocument38 pagesRoss 2001 - Does Oil Hinder DemocracyÖ. Faruk ErtürkNo ratings yet

- 7 - Sidaway - 2007 - Spaces of PostdevelopmentDocument17 pages7 - Sidaway - 2007 - Spaces of PostdevelopmentPaiguliNo ratings yet

- The World Bank, Multinational Companies and The Resource Curse in Africa.Document67 pagesThe World Bank, Multinational Companies and The Resource Curse in Africa.Oreoluwa AsanmoNo ratings yet

- Qatar Chapt 02Document31 pagesQatar Chapt 02Drzavne_TajneNo ratings yet

- The Rentier State in The Middle EastDocument34 pagesThe Rentier State in The Middle EastynsozNo ratings yet

- Haifaa A. Jawad (Eds.) - The Middle East in The New World Order (1997, Palgrave Macmillan UK) PDFDocument229 pagesHaifaa A. Jawad (Eds.) - The Middle East in The New World Order (1997, Palgrave Macmillan UK) PDFarianiNo ratings yet

- López Maya - Venezuela - The Political Crisis of Post-ChavismoDocument21 pagesLópez Maya - Venezuela - The Political Crisis of Post-ChavismoEnrique Sotomayor TrellesNo ratings yet

- Middle East Review Sheet Part 1 and 2Document4 pagesMiddle East Review Sheet Part 1 and 2Elad KaffashNo ratings yet

- Resource Booms and Institutional Pathways The Case of The Extractive Industry in Peru PDFDocument214 pagesResource Booms and Institutional Pathways The Case of The Extractive Industry in Peru PDFJOSÉ MANUEL MEJÍA VILLENANo ratings yet

- After The Sheikhs The Coming Collapse of The Gulf Monarchies PDFDocument324 pagesAfter The Sheikhs The Coming Collapse of The Gulf Monarchies PDFmiaser 1986No ratings yet

- Iraq - The Human Cost of HistoryDocument281 pagesIraq - The Human Cost of Historykameswari2uNo ratings yet