You might also like

- Risk Management Fundamentals: An introduction to risk management in the financial services industry in the 21st centuryFrom EverandRisk Management Fundamentals: An introduction to risk management in the financial services industry in the 21st centuryRating: 5 out of 5 stars5/5 (1)

- Dissertation Project Report On Risk Management in BanksDocument38 pagesDissertation Project Report On Risk Management in BanksKelly HamiltonNo ratings yet

- Credit Risk Assessment: The New Lending System for Borrowers, Lenders, and InvestorsFrom EverandCredit Risk Assessment: The New Lending System for Borrowers, Lenders, and InvestorsNo ratings yet

- Credit Risk Management Policy of BanksDocument35 pagesCredit Risk Management Policy of BanksNeha SharmaNo ratings yet

- Credit Risk Management In and Out of the Financial Crisis: New Approaches to Value at Risk and Other ParadigmsFrom EverandCredit Risk Management In and Out of the Financial Crisis: New Approaches to Value at Risk and Other ParadigmsRating: 1 out of 5 stars1/5 (1)

- Tools Used by Banking Industry For Risk Measure MenDocument9 pagesTools Used by Banking Industry For Risk Measure Meninformatic1988No ratings yet

- Background: Types of RisksDocument7 pagesBackground: Types of Risksnandish30No ratings yet

- Risk Management in Commercial BanksDocument37 pagesRisk Management in Commercial BanksRavi DepaniNo ratings yet

- Credit Risk Grading-Apex TanneryDocument21 pagesCredit Risk Grading-Apex TanneryAbdullahAlNomunNo ratings yet

- Credit Risk ManagementDocument13 pagesCredit Risk ManagementVallabh UtpatNo ratings yet

- CB Case Study 1Document7 pagesCB Case Study 1raviraj969355No ratings yet

- Bank's Balance Sheet QuestionsDocument8 pagesBank's Balance Sheet QuestionsRaja J SahuNo ratings yet

- Risk Management in Banks: BackgroundDocument17 pagesRisk Management in Banks: Backgroundvaishu_4ever724942No ratings yet

- Credit Risk Management Dissertation PDFDocument7 pagesCredit Risk Management Dissertation PDFPaperWritingServicesCanada100% (1)

- New Approaches To SME Finance Using Bank Account Information (Big Data)Document19 pagesNew Approaches To SME Finance Using Bank Account Information (Big Data)ADBI EventsNo ratings yet

- Credit Recovery ManagementDocument75 pagesCredit Recovery ManagementSudeep Chinnabathini75% (4)

- Unit 12 Risk Management: An Overview: ObjectivesDocument33 pagesUnit 12 Risk Management: An Overview: ObjectivesSiva Venkata RamanaNo ratings yet

- Thesis On Credit Risk ManagementDocument4 pagesThesis On Credit Risk Managementbk184deh100% (2)

- Npa 119610079679343 5Document46 pagesNpa 119610079679343 5Teju AshuNo ratings yet

- Term PaperDocument21 pagesTerm PaperPooja JainNo ratings yet

- Credit Risk Management LectureDocument80 pagesCredit Risk Management LectureNoaman Ahmed100% (2)

- Credit Recovery ManagementDocument79 pagesCredit Recovery ManagementSudeep ChinnabathiniNo ratings yet

- Credit Risk Management With Reference of State Bank of IndiaDocument85 pagesCredit Risk Management With Reference of State Bank of IndiakkvNo ratings yet

- Volcker's Rule: UNION BUDGET 2015 - Banking SectorDocument6 pagesVolcker's Rule: UNION BUDGET 2015 - Banking SectorManu RameshNo ratings yet

- Risk Management in BanksDocument27 pagesRisk Management in BanksMAHENDERNo ratings yet

- Unit 5Document28 pagesUnit 5Mohammad ShahvanNo ratings yet

- Credit Risk Management at SBIDocument19 pagesCredit Risk Management at SBIkkvNo ratings yet

- Basics of Credit Risk ModellingDocument13 pagesBasics of Credit Risk ModellingAnonymous 85ygV3JR100% (1)

- Thesis On Credit Risk Management in BanksDocument7 pagesThesis On Credit Risk Management in BanksKim Daniels100% (2)

- Managing Credit Risk in BanksDocument9 pagesManaging Credit Risk in BanksUsaama AbdilaahiNo ratings yet

- Credit Risk Mgmt. at ICICIDocument60 pagesCredit Risk Mgmt. at ICICIRikesh Daliya100% (1)

- The Measurement and Management of Risks in BanksDocument21 pagesThe Measurement and Management of Risks in BanksGaurav GehlotNo ratings yet

- 1nh21ba076 230712 112345Document64 pages1nh21ba076 230712 112345akshaya kasi rajanNo ratings yet

- Sample Thesis On Credit Risk ManagementDocument6 pagesSample Thesis On Credit Risk ManagementINeedSomeoneToWriteMyPaperUK100% (2)

- MFM 842: Financial Risk ManagementDocument74 pagesMFM 842: Financial Risk Management121923602032 PUTTURU JAGADEESHNo ratings yet

- Credit RiskDocument57 pagesCredit RiskmefulltimepassNo ratings yet

- Risk Management Sample AnalysisDocument45 pagesRisk Management Sample AnalysisAlex NavarroNo ratings yet

- To Study The Credit Risk Analysis of Banking Industry With Reference To Sbi BankDocument56 pagesTo Study The Credit Risk Analysis of Banking Industry With Reference To Sbi BankHussain SyedNo ratings yet

- Basel Norms and Credit Risk AssessmentDocument28 pagesBasel Norms and Credit Risk AssessmentAnubhav SrivastavaNo ratings yet

- Credit Risk Management and Best PracticesDocument23 pagesCredit Risk Management and Best Practicessagar7No ratings yet

- CRM - ZuariDocument9 pagesCRM - ZuariKhaisarKhaisarNo ratings yet

- Credit Risk Management LectureDocument80 pagesCredit Risk Management LectureAbhishek KarekarNo ratings yet

- Risk Management in Indian BanksDocument20 pagesRisk Management in Indian BanksDinesh Godhani100% (1)

- Credit Risk ManagementDocument24 pagesCredit Risk ManagementAl-Imran Bin Khodadad100% (2)

- Credit Risk ManagementDocument78 pagesCredit Risk ManagementSanjida100% (1)

- Deeoika 1Document93 pagesDeeoika 1Tanmoy ChakrabortyNo ratings yet

- Oriental Bank of Commerce,: Head Office, DelhiDocument32 pagesOriental Bank of Commerce,: Head Office, DelhiAkshat SinghalNo ratings yet

- Credit Risk ManagementDocument93 pagesCredit Risk Managementepost.sb83% (6)

- Credit RiskDocument30 pagesCredit RiskVineeta HNo ratings yet

- Credit Risk Management in Uk Banks DissertationDocument7 pagesCredit Risk Management in Uk Banks DissertationPayToWriteAPaperUK100% (1)

- Banking Presentation Final - 4Document34 pagesBanking Presentation Final - 4Ganesh Nair100% (1)

- Credit ManagementDocument24 pagesCredit ManagementrajnishdubeNo ratings yet

- FMTD - RIsk Management in BanksDocument6 pagesFMTD - RIsk Management in Banksajay_chitreNo ratings yet

- Risk Management in Banking A Study With Reference-Risk Management in Banking A Study With ReferenceDocument12 pagesRisk Management in Banking A Study With Reference-Risk Management in Banking A Study With ReferencePavithra GowthamNo ratings yet

- Module III: Credit Management: Chapter 6: Credit Risk and RatingDocument25 pagesModule III: Credit Management: Chapter 6: Credit Risk and Ratingsagar7No ratings yet

- Dissertation Main - Risk Management in BanksDocument87 pagesDissertation Main - Risk Management in Banksjesenku100% (1)

- Research Paper On Credit Risk Management in BanksDocument7 pagesResearch Paper On Credit Risk Management in BanksafnhinzugpbcgwNo ratings yet

- Assets and Liabilities Management in Vijaya BankDocument19 pagesAssets and Liabilities Management in Vijaya BankSwarnaa Prakash babuNo ratings yet

- Dissertation On Credit Risk Management in BanksDocument4 pagesDissertation On Credit Risk Management in BanksWriteMyPaperOneDayCanada100% (1)

- Research Papers On Credit Risk Management in BanksDocument6 pagesResearch Papers On Credit Risk Management in Banksgz7gh8h0No ratings yet

- Assignment 3 Chapter 1Document12 pagesAssignment 3 Chapter 1Hatem HassanNo ratings yet

- Hatem Hassan Zakaria - Juhayna Co. Credit AnalysisDocument49 pagesHatem Hassan Zakaria - Juhayna Co. Credit AnalysisHatem Hassan100% (3)

- Assignment 2 Chapter 8Document18 pagesAssignment 2 Chapter 8Hatem Hassan100% (1)

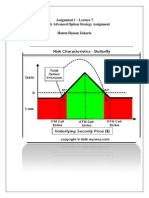

- Butterfly Advanced Option Strategy AssignmentDocument3 pagesButterfly Advanced Option Strategy AssignmentHatem HassanNo ratings yet

- Assignment 1 - Lecture 4 Protective Call & Covered Call Probelm Hatem Hassan ZakariaDocument8 pagesAssignment 1 - Lecture 4 Protective Call & Covered Call Probelm Hatem Hassan ZakariaHatem HassanNo ratings yet

- Butterfly Advanced Option Strategy AssignmentDocument3 pagesButterfly Advanced Option Strategy AssignmentHatem HassanNo ratings yet

- Assignment 1 Chapter 8Document4 pagesAssignment 1 Chapter 8Hatem HassanNo ratings yet

- Assignment 1 - Chapter 6 Call Option Lecture ProblemDocument4 pagesAssignment 1 - Chapter 6 Call Option Lecture ProblemHatem HassanNo ratings yet

- Assignment 3 Chapter 1Document12 pagesAssignment 3 Chapter 1Hatem HassanNo ratings yet

- Assignment 2 Chapter 1Document9 pagesAssignment 2 Chapter 1Hatem HassanNo ratings yet

- Assignment 1 Chapter 1Document9 pagesAssignment 1 Chapter 1Hatem HassanNo ratings yet

- Assignment 2 Chapter 8Document18 pagesAssignment 2 Chapter 8Hatem Hassan100% (1)

- Al Andalous PharmaceuticalsDocument17 pagesAl Andalous PharmaceuticalsHatem HassanNo ratings yet

- EASIER TECHNIQUES FOR BALANCE OF PAYMENTS ANALYSISDocument13 pagesEASIER TECHNIQUES FOR BALANCE OF PAYMENTS ANALYSISHatem HassanNo ratings yet

- Table: 19: Country:Eg Yp T B Al Ance of PaymentsDocument2 pagesTable: 19: Country:Eg Yp T B Al Ance of PaymentsHatem HassanNo ratings yet

- Thirlwall's Law ExplainedDocument1 pageThirlwall's Law ExplainedHatem HassanNo ratings yet

- Exelon Economics AnalysisDocument14 pagesExelon Economics AnalysisHatem HassanNo ratings yet

- Loans Problem in Commercail BanksDocument30 pagesLoans Problem in Commercail BanksHatem HassanNo ratings yet

- Government Banking and BRICs in The Recent Financial CrisisDocument57 pagesGovernment Banking and BRICs in The Recent Financial CrisisHatem HassanNo ratings yet

- Incentive-Based Regulations and Bank Restructuring in EgyptDocument23 pagesIncentive-Based Regulations and Bank Restructuring in EgyptHatem HassanNo ratings yet

- Islamic Banking ResearchDocument19 pagesIslamic Banking ResearchHatem HassanNo ratings yet

- The Contexts of International BusinessDocument8 pagesThe Contexts of International BusinessHatem HassanNo ratings yet

- Situational Leadership MANAGEMENTDocument2 pagesSituational Leadership MANAGEMENTHatem Hassan88% (8)

- Chapter 18 Mass CommunicationDocument25 pagesChapter 18 Mass CommunicationHatem HassanNo ratings yet

- Assignment 2: Lesson Plan Analysis, Revision and Justification - Kaitlin Rose TrojkoDocument9 pagesAssignment 2: Lesson Plan Analysis, Revision and Justification - Kaitlin Rose Trojkoapi-408336810No ratings yet

- Fi 7160Document2 pagesFi 7160maxis2022No ratings yet

- Operating Instructions: Blu-Ray Disc™ / DVD Player BDP-S470Document39 pagesOperating Instructions: Blu-Ray Disc™ / DVD Player BDP-S470JhamNo ratings yet

- Complex Numbers GuideDocument17 pagesComplex Numbers GuideGus EdiNo ratings yet

- Pic Attack1Document13 pagesPic Attack1celiaescaNo ratings yet

- Mutaz Abdelrahim - Doa - MT-103Document17 pagesMutaz Abdelrahim - Doa - MT-103Minh KentNo ratings yet

- Corporate GovernanceDocument35 pagesCorporate GovernanceshrikirajNo ratings yet

- BILL of Entry (O&A) PDFDocument3 pagesBILL of Entry (O&A) PDFHiJackNo ratings yet

- Operation Manual TempoLink 551986 enDocument12 pagesOperation Manual TempoLink 551986 enBryan AndradeNo ratings yet

- p2 - Guerrero Ch13Document40 pagesp2 - Guerrero Ch13JerichoPedragosa88% (17)

- Digestive System Song by MR ParrDocument2 pagesDigestive System Song by MR ParrRanulfo MayolNo ratings yet

- Product Data: T T 13 SEER Single - Packaged Heat Pump R (R - 410A) RefrigerantDocument36 pagesProduct Data: T T 13 SEER Single - Packaged Heat Pump R (R - 410A) RefrigerantJesus CantuNo ratings yet

- Expose Anglais TelephoneDocument6 pagesExpose Anglais TelephoneAlexis SoméNo ratings yet

- Veolia Moray Outfalls Repair WorksDocument8 pagesVeolia Moray Outfalls Repair WorksGalih PutraNo ratings yet

- Machine Tools Cutting FluidsDocument133 pagesMachine Tools Cutting FluidsDamodara MadhukarNo ratings yet

- Amma dedicates 'Green Year' to environmental protection effortsDocument22 pagesAmma dedicates 'Green Year' to environmental protection effortsOlivia WilliamsNo ratings yet

- Course Handbook MSC Marketing Sept2022Document58 pagesCourse Handbook MSC Marketing Sept2022Tauseef JamalNo ratings yet

- Module 2 What It Means To Be AI FirstDocument85 pagesModule 2 What It Means To Be AI FirstSantiago Ariel Bustos YagueNo ratings yet

- An Improved Ant Colony Algorithm and Its ApplicatiDocument10 pagesAn Improved Ant Colony Algorithm and Its ApplicatiI n T e R e Y eNo ratings yet

- C++ Programmierung (Benjamin Buch, Wikibooks - Org)Document257 pagesC++ Programmierung (Benjamin Buch, Wikibooks - Org)stefano rossiNo ratings yet

- 2.5L ENGINE Chevy Tracker 1999Document580 pages2.5L ENGINE Chevy Tracker 1999andres german romeroNo ratings yet

- 114 ArDocument254 pages114 ArJothishNo ratings yet

- Past Paper Booklet - QPDocument506 pagesPast Paper Booklet - QPMukeshNo ratings yet

- Pharma Pathway SopDocument350 pagesPharma Pathway SopDinesh Senathipathi100% (1)

- Geometric Dilution of Precision ComputationDocument25 pagesGeometric Dilution of Precision ComputationAntonius NiusNo ratings yet

- Putri KartikaDocument17 pagesPutri KartikaRamotSilabanNo ratings yet

- Rivalry and Central PlanningDocument109 pagesRivalry and Central PlanningElias GarciaNo ratings yet

- Destroyed Inventory Deduction ProceduresDocument7 pagesDestroyed Inventory Deduction ProceduresCliff DaquioagNo ratings yet

- Excel Bill of Materials Bom TemplateDocument8 pagesExcel Bill of Materials Bom TemplateRavi ChhawdiNo ratings yet

- Wei Et Al 2016Document7 pagesWei Et Al 2016Aline HunoNo ratings yet