You might also like

- Revolving Line of Credit AgreementDocument9 pagesRevolving Line of Credit AgreementRobert ArkinNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Section 80DD, Section 80DDB, Section 80U - Tax Deduction For Disabled PersonsDocument19 pagesSection 80DD, Section 80DDB, Section 80U - Tax Deduction For Disabled Personsvvijayaraghava100% (1)

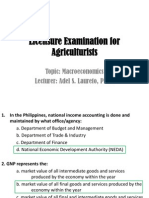

- RB CAGMAT REVIEW Macroeconomics Reviewer - Yet Sample QuestionsDocument35 pagesRB CAGMAT REVIEW Macroeconomics Reviewer - Yet Sample QuestionsSylveth Novah Badal Denzo100% (1)

- US Internal Revenue Service: f706 - 2005Document40 pagesUS Internal Revenue Service: f706 - 2005IRSNo ratings yet

- Form 8854 Expatriate Information StatementDocument5 pagesForm 8854 Expatriate Information StatementSami HartsfieldNo ratings yet

- US Internal Revenue Service: F3520a - 1999Document4 pagesUS Internal Revenue Service: F3520a - 1999IRSNo ratings yet

- Annual Return for Foreign Trust TransactionsDocument6 pagesAnnual Return for Foreign Trust TransactionsFAQMD2No ratings yet

- Form 706-NA Estate Tax Return for Nonresident AlienDocument2 pagesForm 706-NA Estate Tax Return for Nonresident Aliendouglas jonesNo ratings yet

- Certificate of Payment of Foreign Death TaxDocument3 pagesCertificate of Payment of Foreign Death Taxdouglas jonesNo ratings yet

- 6399 Supplemental Statement 20200730 7Document13 pages6399 Supplemental Statement 20200730 7Newsbomb AlbaniaNo ratings yet

- Annual Return To Report Transactions With Foreign TrustsDocument6 pagesAnnual Return To Report Transactions With Foreign TrustsCarmita Keepitmovin FosterNo ratings yet

- United States Additional Estate Tax Return: General InformationDocument4 pagesUnited States Additional Estate Tax Return: General InformationIRSNo ratings yet

- Initial and Annual Expatriation StatementDocument5 pagesInitial and Annual Expatriation StatementMarishiNo ratings yet

- United States Estate (And Generation-Skipping Transfer) Tax ReturnDocument31 pagesUnited States Estate (And Generation-Skipping Transfer) Tax ReturnHazem El SayedNo ratings yet

- United States Estate (And Generation-Skipping Transfer) Tax ReturnDocument29 pagesUnited States Estate (And Generation-Skipping Transfer) Tax Returndouglas jonesNo ratings yet

- IRS Publication Form 706Document4 pagesIRS Publication Form 706Francis Wolfgang UrbanNo ratings yet

- Foreign Earned Income: 34 For Use by U.S. Citizens and Resident Aliens OnlyDocument3 pagesForeign Earned Income: 34 For Use by U.S. Citizens and Resident Aliens OnlyTanasha FlandersNo ratings yet

- OMB FARA FormDocument7 pagesOMB FARA FormTitle IV-D Man with a planNo ratings yet

- Pink FilingDocument3,185 pagesPink FilingMichael James0% (1)

- Beaulieu Bankruptcy FilingDocument170 pagesBeaulieu Bankruptcy FilingDan LehrNo ratings yet

- Voluntary Petition For Non-Individuals Filing For BankruptcyDocument30 pagesVoluntary Petition For Non-Individuals Filing For BankruptcyAnonymous lTRXIIVnyNo ratings yet

- Discovery Tours Files Chapter 7 BankruptcyDocument4 pagesDiscovery Tours Files Chapter 7 BankruptcyWKYC.comNo ratings yet

- Discovery Tours Files For Chapter 7 BankruptcyDocument1,944 pagesDiscovery Tours Files For Chapter 7 BankruptcyWKYC.comNo ratings yet

- Trident Lakes Property Holdings LLC BankruptcyDocument5 pagesTrident Lakes Property Holdings LLC BankruptcyCBS 11 NewsNo ratings yet

- US Internal Revenue Service: f2555 - 1991Document3 pagesUS Internal Revenue Service: f2555 - 1991IRSNo ratings yet

- Buffalo Diocese Bankruptcy FilingDocument38 pagesBuffalo Diocese Bankruptcy Filingamber healyNo ratings yet

- Voluntary Petition For Non-Individuals Filing For BankruptcyDocument42 pagesVoluntary Petition For Non-Individuals Filing For BankruptcyAnonymous lTRXIIVnyNo ratings yet

- US Internal Revenue Service: f1116 - 1997Document2 pagesUS Internal Revenue Service: f1116 - 1997IRSNo ratings yet

- Jims Place CHP 7 BankruptcyDocument50 pagesJims Place CHP 7 BankruptcycinemapprenticeNo ratings yet

- StemGenex Files For BankruptcyDocument53 pagesStemGenex Files For BankruptcyLeighTurnerNo ratings yet

- Boyce Hydro Bankruptcy Filing - U.S. Bankruptcy Court - EASTERN DISTRICT OF MICHIGANDocument51 pagesBoyce Hydro Bankruptcy Filing - U.S. Bankruptcy Court - EASTERN DISTRICT OF MICHIGANCaleb HollowayNo ratings yet

- Subway Bankrupcy 1Document34 pagesSubway Bankrupcy 1Kate TaylorNo ratings yet

- Sample Form 56Document2 pagesSample Form 56greatist70No ratings yet

- FORM 20-F: United States Securities and Exchange CommissionDocument427 pagesFORM 20-F: United States Securities and Exchange Commissionميرنا ميرناNo ratings yet

- Voluntary Petition For Non-Individuals Filing For BankruptcyDocument15 pagesVoluntary Petition For Non-Individuals Filing For Bankruptcytriguy_2010No ratings yet

- US Internal Revenue Service: f1120f - 2002Document6 pagesUS Internal Revenue Service: f1120f - 2002IRSNo ratings yet

- Document 1 Chapter 11 Filing Show - Temp PDFDocument16 pagesDocument 1 Chapter 11 Filing Show - Temp PDFeforman85No ratings yet

- Coon Ol: Second DivisionDocument19 pagesCoon Ol: Second DivisionRaymond RogacionNo ratings yet

- Earth Fare Files For Chapter 11 BankruptcyDocument19 pagesEarth Fare Files For Chapter 11 BankruptcyJeff WilliamsonNo ratings yet

- US Internal Revenue Service: f1120f - 1991Document6 pagesUS Internal Revenue Service: f1120f - 1991IRSNo ratings yet

- 8281 2010 PIMCO ExDocument1 page8281 2010 PIMCO ExBunny Fontaine100% (1)

- US Internal Revenue Service: f5472 AccessibleDocument4 pagesUS Internal Revenue Service: f5472 AccessibleIRSNo ratings yet

- Voluntary Petition For Non-Individuals Filing For BankruptcyDocument128 pagesVoluntary Petition For Non-Individuals Filing For BankruptcyMichaelPatrickMcSweeneyNo ratings yet

- Johnson Publishing BankruptcyDocument35 pagesJohnson Publishing BankruptcySteve WarmbirNo ratings yet

- Cover Sheet: Month Day Month DayDocument56 pagesCover Sheet: Month Day Month DayOnyeta HICUwnaNo ratings yet

- f1096 Internal Revenue Tax Form For - Coldwell Banker Real Estate Limited Liability CompanyDocument2 pagesf1096 Internal Revenue Tax Form For - Coldwell Banker Real Estate Limited Liability Companyakil kemnebi easley elNo ratings yet

- Foreign Tax Credit CalculationDocument2 pagesForeign Tax Credit CalculationTanasha FlandersNo ratings yet

- Fara KeeneDocument12 pagesFara KeeneAli AmarNo ratings yet

- Form7 2007 08Document12 pagesForm7 2007 08api-3850174No ratings yet

- XPeng Inc - Form 20-F (Apr-16-2021)Document271 pagesXPeng Inc - Form 20-F (Apr-16-2021)Peng WuNo ratings yet

- U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnDocument4 pagesU.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnIRSNo ratings yet

- Nria Chapt. 11Document23 pagesNria Chapt. 11RSNo ratings yet

- United States Estate (And Generation-Skipping Transfer) Tax ReturnDocument28 pagesUnited States Estate (And Generation-Skipping Transfer) Tax ReturnsirpiekNo ratings yet

- Alfred Angelo CH 7 FilingDocument1,044 pagesAlfred Angelo CH 7 FilingkmccoynycNo ratings yet

- International Applications of U.S. Income Tax Law: Inbound and Outbound TransactionsFrom EverandInternational Applications of U.S. Income Tax Law: Inbound and Outbound TransactionsNo ratings yet

- The Wall Street Waltz: 90 Visual Perspectives, Illustrated Lessons From Financial Cycles and TrendsFrom EverandThe Wall Street Waltz: 90 Visual Perspectives, Illustrated Lessons From Financial Cycles and TrendsNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- The Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeFrom EverandThe Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeNo ratings yet

- Getting Started in A Financially Secure RetirementFrom EverandGetting Started in A Financially Secure RetirementRating: 4.5 out of 5 stars4.5/5 (2)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Assignment Law Q 26, 48, 78Document13 pagesAssignment Law Q 26, 48, 78Syahirah AliNo ratings yet

- An Act To Define Condominium, Establish Requirements For Its Creation, and Govern Its Incidents.Document9 pagesAn Act To Define Condominium, Establish Requirements For Its Creation, and Govern Its Incidents.erikha_aranetaNo ratings yet

- F 703Document6 pagesF 703Pritam WarudkarNo ratings yet

- Hayman July 07Document5 pagesHayman July 07grumpyfeckerNo ratings yet

- For Bidding DecDocument20 pagesFor Bidding DecramszlaiNo ratings yet

- Softcell Mail BodyDocument3 pagesSoftcell Mail BodyAmit SinghNo ratings yet

- BTF3601 ExamDocument8 pagesBTF3601 ExamOverflagNo ratings yet

- Essential elements of an oral contract of saleDocument1 pageEssential elements of an oral contract of saleCareyssa MaeNo ratings yet

- Lim Tong Lim v. Philippine Fishing Gear Industries, Inc., G.R. No. 136448Document14 pagesLim Tong Lim v. Philippine Fishing Gear Industries, Inc., G.R. No. 136448Krister VallenteNo ratings yet

- Product & Services of KSFCDocument109 pagesProduct & Services of KSFCशैलेश चन्द0% (1)

- 1up Mercantile Law Reviewer 2017 PDFDocument368 pages1up Mercantile Law Reviewer 2017 PDFManny Aragones100% (1)

- Advance Financial Management - Financial Tools - Written ReportDocument36 pagesAdvance Financial Management - Financial Tools - Written Reportgilbertson tinioNo ratings yet

- Substantive rights under due process: Acts that cannot be criminalized such as debtsDocument2 pagesSubstantive rights under due process: Acts that cannot be criminalized such as debtsJebellePuracanNo ratings yet

- Vidit TOPA First DraftDocument11 pagesVidit TOPA First DraftVidit HarsulkarNo ratings yet

- Modelo Proof of Claim MaestroDocument8 pagesModelo Proof of Claim MaestroMetro Puerto RicoNo ratings yet

- Cashflow 101 ManualDocument16 pagesCashflow 101 Manualwladwolf100% (2)

- Focus On Personal Finance 5Th Edition Kapoor Test Bank Full Chapter PDFDocument67 pagesFocus On Personal Finance 5Th Edition Kapoor Test Bank Full Chapter PDFmiguelstone5tt0f100% (12)

- Citimotors, Inc. Makati Application FormDocument1 pageCitimotors, Inc. Makati Application FormAnonymous XmpmkShNo ratings yet

- Genova vs. de CastroDocument2 pagesGenova vs. de CastropiptipaybNo ratings yet

- CIA2001 Tutorial Accounting For Leases Part 2Document7 pagesCIA2001 Tutorial Accounting For Leases Part 2Putri Nurin Hasnida HassanNo ratings yet

- ProblemDocument2 pagesProblemAnonymous JiiHPiQmiNo ratings yet

- Bus Org Case Digest Compile IncompleteDocument19 pagesBus Org Case Digest Compile IncompleteWuwu WuswewuNo ratings yet

- EjectmentPacket As APPLIED in USDocument23 pagesEjectmentPacket As APPLIED in USdsay88No ratings yet

- Dispute over mortgage loan violations and notice of intent to rescindDocument3 pagesDispute over mortgage loan violations and notice of intent to rescindj_west30No ratings yet

- Financial Hardship Letter SampleDocument2 pagesFinancial Hardship Letter SampleWilliam BluntNo ratings yet

- Bir60 EguideDocument15 pagesBir60 Eguidekumar.arasu8717No ratings yet

- Chapter 13: Schedule VI: Rohit AgarwalDocument3 pagesChapter 13: Schedule VI: Rohit Agarwalbcom0% (1)