You might also like

- ICAB Fees Schedule 2016Document17 pagesICAB Fees Schedule 2016dff_jx100% (2)

- ICAP revises minimum audit fees and hourly ratesDocument5 pagesICAP revises minimum audit fees and hourly ratesMuhammad KhanNo ratings yet

- Atr 14 (2008)Document4 pagesAtr 14 (2008)Awais AhmadNo ratings yet

- ICAP ATR 14 Minimum Fee Revised 2008Document4 pagesICAP ATR 14 Minimum Fee Revised 2008Zeeshan Shahid100% (3)

- CARO 2020 Question BankDocument12 pagesCARO 2020 Question BankVINUS DHANKHARNo ratings yet

- Advance Audit and Professional Ethics Amendment NotesDocument38 pagesAdvance Audit and Professional Ethics Amendment NotesSnehaNo ratings yet

- Auditing Trs by IcapDocument53 pagesAuditing Trs by IcapArif AliNo ratings yet

- Rtpfinalnew Nov20 p3Document30 pagesRtpfinalnew Nov20 p3cdNo ratings yet

- The National Small Industries Corporation Limited: Registration Fee For Enlistment Under SprsDocument1 pageThe National Small Industries Corporation Limited: Registration Fee For Enlistment Under SprsRenuka KNNo ratings yet

- Accounting Standard LLP - 05.11.2023Document10 pagesAccounting Standard LLP - 05.11.2023Mustafa MisriNo ratings yet

- 60829bos49465 PDFDocument11 pages60829bos49465 PDFHari KiranNo ratings yet

- Ensuring Audit Quality Through Optimal Audit FeesDocument3 pagesEnsuring Audit Quality Through Optimal Audit FeesAsjad MobeenNo ratings yet

- Asifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-10 PDFDocument21 pagesAsifamin - 3179 - 18893 - 6 - Taxation Pakistan - Session-10 PDFaemanNo ratings yet

- RTP Nov 2020Document30 pagesRTP Nov 2020Syamala GadupudiNo ratings yet

- Amendments: May 2011 ExamsDocument13 pagesAmendments: May 2011 ExamsKanth RaaveeNo ratings yet

- Chapter Zakat Acc For Ibis-1 - 42051Document20 pagesChapter Zakat Acc For Ibis-1 - 42051Aisyah AnuarNo ratings yet

- All Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestDocument13 pagesAll Mcqs Are Compulsory Question No. 1 Is Compulsory. Attempt Any Four Questions From The RestGJ ELASHREEVALLINo ratings yet

- Audit MTP Nov'22Document22 pagesAudit MTP Nov'22Kushagra SoniNo ratings yet

- What Is This Section Is All AboutDocument11 pagesWhat Is This Section Is All AboutjasminerathodNo ratings yet

- Frequently Asked Question Single Point Registration Scheme: Page 1 of 4Document4 pagesFrequently Asked Question Single Point Registration Scheme: Page 1 of 4Bubbly GalNo ratings yet

- Cost Audit Programme SpeechDocument4 pagesCost Audit Programme SpeechJaymin ShahNo ratings yet

- Indian Cost Accountants Service Notes - Cap BudgetingDocument19 pagesIndian Cost Accountants Service Notes - Cap Budgetingbefox87318No ratings yet

- Important Instruction & Fees StructureDocument3 pagesImportant Instruction & Fees StructurePeppers ChannelNo ratings yet

- Test 8Document3 pagesTest 8lalshahbaz57No ratings yet

- Budget 2018 Highlights Direct Tax ChangesDocument5 pagesBudget 2018 Highlights Direct Tax ChangesSrushti BhattNo ratings yet

- Wbhidco Kolkata TenderDocument24 pagesWbhidco Kolkata Tendershafaquesameen2001No ratings yet

- Indirect Tax Laws Detail Test 1 May 2024 Solution 1702459521Document13 pagesIndirect Tax Laws Detail Test 1 May 2024 Solution 1702459521SAKSHI SINGHNo ratings yet

- Odisha Hydro Power Corporation EOIDocument12 pagesOdisha Hydro Power Corporation EOISoumyaranjan SinghNo ratings yet

- Dec 2021 Law New Syllabus MCQ Topic Coverage (Hints) Sebi LodrDocument18 pagesDec 2021 Law New Syllabus MCQ Topic Coverage (Hints) Sebi LodrKhader MohammedNo ratings yet

- CA-Inter-Accounts-RTP-Nov23-castudynotes-comDocument33 pagesCA-Inter-Accounts-RTP-Nov23-castudynotes-comAbhishant KapahiNo ratings yet

- Scale of Professional Fees NewDocument9 pagesScale of Professional Fees NewOwolabi Olusola RajiNo ratings yet

- New Book ChangesDocument26 pagesNew Book Changessairad1999No ratings yet

- FILING GUIDELINES FOR INVESTMENT REGISTRATIONDocument4 pagesFILING GUIDELINES FOR INVESTMENT REGISTRATIONGabe RuaroNo ratings yet

- SEBI Board Meeting: I. Reduction of Fees Payable by Brokers by 25% and Calibration of Other FeesDocument4 pagesSEBI Board Meeting: I. Reduction of Fees Payable by Brokers by 25% and Calibration of Other FeesNewsBharatiNo ratings yet

- Capital Budgeting: Prepared By:-Priyanka GohilDocument44 pagesCapital Budgeting: Prepared By:-Priyanka GohilSunil PillaiNo ratings yet

- Sebi Corporate GovernanceDocument8 pagesSebi Corporate GovernanceNARU MANOJ KUMARNo ratings yet

- Ca Audit PDFDocument154 pagesCa Audit PDFsandesh1506No ratings yet

- Auditing Set 2Document7 pagesAuditing Set 2cleophacerevivalNo ratings yet

- CDA guidelines for cooperative external auditor accreditationDocument11 pagesCDA guidelines for cooperative external auditor accreditationAndres Lorenzo III50% (2)

- PWC Frcn-Rules On Reporting PDFDocument7 pagesPWC Frcn-Rules On Reporting PDFamandaNo ratings yet

- Qau Memo 2021-14. AnnexesDocument16 pagesQau Memo 2021-14. AnnexesMariene PagsibiganNo ratings yet

- Guidelines On Applying For BOI RegistrationDocument12 pagesGuidelines On Applying For BOI RegistrationCarol DonsolNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument9 pages© The Institute of Chartered Accountants of IndiaGJ ELASHREEVALLINo ratings yet

- Requirements For Setting Up Micro Finance BankDocument9 pagesRequirements For Setting Up Micro Finance BankadamuNo ratings yet

- Income Taxation and MCIT RulesDocument4 pagesIncome Taxation and MCIT RulesMJNo ratings yet

- SME-CS PS RaoDocument29 pagesSME-CS PS Raonilesh nayeeNo ratings yet

- Guidelines For ListingDocument9 pagesGuidelines For ListingTarun LoharNo ratings yet

- FM Fast Track Volume 1 - 2024-02-19 17-12-41Document184 pagesFM Fast Track Volume 1 - 2024-02-19 17-12-41vrushankpatel377No ratings yet

- Frequently Asked Question Single Point Registration Scheme: Page 1 of 5Document5 pagesFrequently Asked Question Single Point Registration Scheme: Page 1 of 5HstgasuNo ratings yet

- UCO BANK Audit and InspectionDocument16 pagesUCO BANK Audit and Inspectionganpati megabuilderNo ratings yet

- REGISTRATION REQUIREMENTS FOR MERCHANT BANKERSDocument28 pagesREGISTRATION REQUIREMENTS FOR MERCHANT BANKERSrthi04No ratings yet

- Test 7Document4 pagesTest 7lalshahbaz57No ratings yet

- Chartered Institute of Taxation of NigeriaDocument8 pagesChartered Institute of Taxation of NigeriaAfolabi OladunniNo ratings yet

- Budget 2023 CKDocument16 pagesBudget 2023 CKVenkateswar raoNo ratings yet

- Prakas On Accreditation of Professional Accounting Firm Providing... EnglishDocument12 pagesPrakas On Accreditation of Professional Accounting Firm Providing... EnglishChou ChantraNo ratings yet

- Auditing AnalysisDocument13 pagesAuditing AnalysisAmmarah Rajput ParhiarNo ratings yet

- CAF 6 Exam SuppDocument12 pagesCAF 6 Exam Suppg8888No ratings yet

- Indian Cost Accountants Service - Notes: By: Tarun MahajanDocument38 pagesIndian Cost Accountants Service - Notes: By: Tarun MahajanAKSHAYA RAVINo ratings yet

- Test 10Document4 pagesTest 10ls786580302No ratings yet

- Executive's Guide to COSO Internal Controls: Understanding and Implementing the New FrameworkFrom EverandExecutive's Guide to COSO Internal Controls: Understanding and Implementing the New FrameworkNo ratings yet

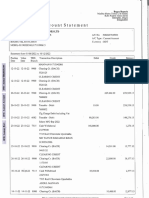

- Oific: Account StatementDocument1 pageOific: Account StatementFøèzÅhåmmédNo ratings yet

- NN SirDocument1 pageNN SirFøèzÅhåmmédNo ratings yet

- Ifii:: Account StatementDocument1 pageIfii:: Account StatementFøèzÅhåmmédNo ratings yet

- Oific: Account StatementDocument1 pageOific: Account StatementFøèzÅhåmmédNo ratings yet

- Financial System in BangladeshDocument30 pagesFinancial System in BangladeshS.E Chowdhury90% (31)

- NN SirDocument1 pageNN SirFøèzÅhåmmédNo ratings yet

- NN SirDocument1 pageNN SirFøèzÅhåmmédNo ratings yet

- NN SirDocument1 pageNN SirFøèzÅhåmmédNo ratings yet

- NN SirDocument1 pageNN SirFøèzÅhåmmédNo ratings yet

- NN SirDocument1 pageNN SirFøèzÅhåmmédNo ratings yet

- NN SirDocument1 pageNN SirFøèzÅhåmmédNo ratings yet

- View PDFDocument1 pageView PDFFøèzÅhåmmédNo ratings yet

- Financial System in BangladeshDocument30 pagesFinancial System in BangladeshS.E Chowdhury90% (31)

- 2 Accounting 19Document2 pages2 Accounting 19FøèzÅhåmmédNo ratings yet

- Annual Report 2016Document17 pagesAnnual Report 2016FøèzÅhåmmédNo ratings yet

- Annual Report 2016 PDFDocument231 pagesAnnual Report 2016 PDFFøèzÅhåmmédNo ratings yet

- PricingDocument12 pagesPricingFøèzÅhåmmédNo ratings yet

- Annual ReportDocument2 pagesAnnual ReportFøèzÅhåmmédNo ratings yet

- Small BusinessDocument4 pagesSmall BusinessFøèzÅhåmmédNo ratings yet

- CHAPTER 2 Group No.1Document227 pagesCHAPTER 2 Group No.1Pavan KumarNo ratings yet

- Citibank Performance EvaluationDocument9 pagesCitibank Performance EvaluationMohit Sharma67% (6)

- Making Internal Audit More Credible and RelevantDocument11 pagesMaking Internal Audit More Credible and RelevantCarlos BermudezNo ratings yet

- Code of Conduct Living Our ValuesDocument35 pagesCode of Conduct Living Our ValuesKim Na NaNo ratings yet

- Relationship Between Financial Management Skills and Job Satisfaction Amon The Teachers of Bagumbayan National High School - Group1 - ABM - Chapter1Document12 pagesRelationship Between Financial Management Skills and Job Satisfaction Amon The Teachers of Bagumbayan National High School - Group1 - ABM - Chapter1Wenzil CastillonNo ratings yet

- Electrical Contracting Book V2Document199 pagesElectrical Contracting Book V2HandoyoGozali100% (1)

- Robotic Process Automation: Bachelor of TechnologyDocument9 pagesRobotic Process Automation: Bachelor of TechnologyShivam Juneja0% (1)

- Advising - Payslip - 20309012 - Shamim Ara Jahan SharnaDocument2 pagesAdvising - Payslip - 20309012 - Shamim Ara Jahan SharnaFardin Ibn ZamanNo ratings yet

- Philips Lighting Annual ReportDocument158 pagesPhilips Lighting Annual ReportOctavian Andrei NanciuNo ratings yet

- Interview Base - Knowledge & PracticalDocument39 pagesInterview Base - Knowledge & Practicalsonu malikNo ratings yet

- Harmonising SME accounting standardsDocument144 pagesHarmonising SME accounting standardsJahde GoncalvesNo ratings yet

- Banks Customer Satisfaction in Kuwait PDFDocument77 pagesBanks Customer Satisfaction in Kuwait PDFpavlov2No ratings yet

- Reading - Unit 6. Vocabulary Questions & Part 6Document16 pagesReading - Unit 6. Vocabulary Questions & Part 6baomuahe94No ratings yet

- TCS Annual Report 2019-20Document44 pagesTCS Annual Report 2019-20Savi MahajanNo ratings yet

- Mpa AssignmentDocument8 pagesMpa AssignmentSanah SahniNo ratings yet

- Employee Engagement: The Key To Realizing Competitive AdvantageDocument33 pagesEmployee Engagement: The Key To Realizing Competitive Advantageshivi_kashtiNo ratings yet

- Iso 9000 - Quality HandbookDocument331 pagesIso 9000 - Quality HandbookJavier Pozo Santana92% (13)

- Companies Act 2013 HighlightsDocument9 pagesCompanies Act 2013 Highlightsashishbajaj007100% (2)

- Nature of AdvertisingDocument13 pagesNature of AdvertisingMitzi Gia CuentaNo ratings yet

- Internal Audit Report - 2022Document2 pagesInternal Audit Report - 2022Camila AlmeidaNo ratings yet

- 5s PrincipleDocument22 pages5s PrincipleamaliaNo ratings yet

- Dolat Capital Market - Vinati Organics - Q2FY20 Result Update - 1Document6 pagesDolat Capital Market - Vinati Organics - Q2FY20 Result Update - 1Bhaveek OstwalNo ratings yet

- Layer Business PlanDocument15 pagesLayer Business PlanHumphrey67% (3)

- Customer SatisfactionDocument17 pagesCustomer Satisfactionrcindia1No ratings yet

- Subway Application FormDocument2 pagesSubway Application Formsaidul67% (3)

- Offer Letter - Deepak ChaudharyDocument4 pagesOffer Letter - Deepak ChaudharyHR SSIFNo ratings yet

- KPIs Customs 2021Document193 pagesKPIs Customs 2021Syed Hadi Hussain ShahNo ratings yet

- Final Marketing Strategies of PatanjaliDocument53 pagesFinal Marketing Strategies of PatanjaliYash Rawat100% (1)

- Flash Reports DefinitionDocument8 pagesFlash Reports Definitionca_rudraNo ratings yet

- Production Process Analysis ExerciseDocument10 pagesProduction Process Analysis ExerciseBishnu PoudelNo ratings yet