You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Impact Assessment of Agriculture Interventions in Tribal Areas in Madhya Pradesh PDFDocument133 pagesImpact Assessment of Agriculture Interventions in Tribal Areas in Madhya Pradesh PDFsuneelmanage09No ratings yet

- NCML BrochureDocument16 pagesNCML Brochuresuneelmanage09No ratings yet

- CP05 - IER - Web Theory of Chnage - Impact AssessmentDocument40 pagesCP05 - IER - Web Theory of Chnage - Impact Assessmentsuneelmanage09No ratings yet

- THDCIL Impact Assessment Report 2015Document117 pagesTHDCIL Impact Assessment Report 2015suneelmanage09No ratings yet

- Import Export Detailed ReportDocument468 pagesImport Export Detailed Reportsharath_medishetty100% (1)

- E´Ekõj·T Kõ+Πø‹Ø£ J·÷»E÷Q´ Dü+Düú: (Atma)Document8 pagesE´Ekõj·T Kõ+Πø‹Ø£ J·÷»E÷Q´ Dü+Düú: (Atma)suneelmanage09No ratings yet

- District-Wise Forest Cover - Andhra PradeshDocument3 pagesDistrict-Wise Forest Cover - Andhra Pradeshsuneelmanage09No ratings yet

- Monthwise Annual Priceand Arrival ReportDocument8 pagesMonthwise Annual Priceand Arrival Reportsuneelmanage09No ratings yet

- Aug - 17 Vessels DetailsDocument2 pagesAug - 17 Vessels Detailssuneelmanage09No ratings yet

- Baleno-Accessories Brochure PDFDocument8 pagesBaleno-Accessories Brochure PDFnapinnvoNo ratings yet

- NFSM - Telangana State (18!11!2014)Document27 pagesNFSM - Telangana State (18!11!2014)suneelmanage09No ratings yet

- Baleno-Accessories Brochure PDFDocument8 pagesBaleno-Accessories Brochure PDFnapinnvoNo ratings yet

- Report 4Document103 pagesReport 4suneelmanage09No ratings yet

- Operational Guidelines For NAMDocument28 pagesOperational Guidelines For NAMmbNo ratings yet

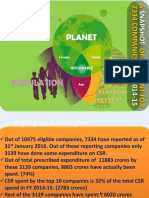

- On CSR Expenditure of 7334 Companies For F.Y 2014 15Document14 pagesOn CSR Expenditure of 7334 Companies For F.Y 2014 15suneelmanage09No ratings yet

- Associations Federations Councils Etc ContactsDocument20 pagesAssociations Federations Councils Etc Contactssuneelmanage09No ratings yet

- Value Chain of Wheat N Rice in U.P PDFDocument33 pagesValue Chain of Wheat N Rice in U.P PDFshamanth143kNo ratings yet

- Manual CottonDocument34 pagesManual Cottonvicky305No ratings yet

- Food Supply Chains and Their Influence On Resurgence in Institutions of CommonsDocument18 pagesFood Supply Chains and Their Influence On Resurgence in Institutions of Commonssuneelmanage09No ratings yet

- List of FPOs in The State of Andhra PradeshDocument1 pageList of FPOs in The State of Andhra Pradeshsuneelmanage09No ratings yet

- 6 KazakhstanDocument17 pages6 Kazakhstansuneelmanage09No ratings yet

- RATED GINNING FACTORIESDocument58 pagesRATED GINNING FACTORIESsuneelmanage09No ratings yet

- Hortstat GlanceDocument463 pagesHortstat GlancebhagatvarunNo ratings yet

- Kenya Leather Industry Diagnosis Strategy and Action PlanDocument126 pagesKenya Leather Industry Diagnosis Strategy and Action Plansuneelmanage09No ratings yet

- India Africa Partnership in Agriculture Current and Future ProspectsDocument52 pagesIndia Africa Partnership in Agriculture Current and Future Prospectssuneelmanage09100% (2)

- Using Mobile Phone-Based Market InformatDocument19 pagesUsing Mobile Phone-Based Market Informatsuneelmanage09No ratings yet

- FAO IGG TEA - Working Group On Organic Tea May 2014Document17 pagesFAO IGG TEA - Working Group On Organic Tea May 2014suneelmanage09No ratings yet

- Hope BrewingDocument29 pagesHope Brewingsuneelmanage09No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Study online at quizlet.com/_23q1qiDocument2 pagesStudy online at quizlet.com/_23q1qiAPRATIM BHUIYANNo ratings yet

- 2015 SALN FormDocument2 pages2015 SALN FormCHERRYMIE DIONSONNo ratings yet

- 4 2 Technical Analysis Fibonacci PDFDocument11 pages4 2 Technical Analysis Fibonacci PDFDis JovscNo ratings yet

- RRLDocument2 pagesRRLJOHN AXIL ALEJONo ratings yet

- VCMQ1Document11 pagesVCMQ1Daniella Dhanice CanoNo ratings yet

- Cheque Introduction: A Cheque Is A Document of Very Great Importance in TheDocument13 pagesCheque Introduction: A Cheque Is A Document of Very Great Importance in The777priyankaNo ratings yet

- Daimler Q3 2011 Interim ReportDocument38 pagesDaimler Q3 2011 Interim ReportSaiful_Azri_1450No ratings yet

- Tax Invoice: Mcconnell DowellDocument1 pageTax Invoice: Mcconnell DowellAndy HeaterNo ratings yet

- Horizon Kinetics: Q4-2021-Quarterly-Review - FINALDocument32 pagesHorizon Kinetics: Q4-2021-Quarterly-Review - FINALTBoone0No ratings yet

- Practice Problems - Audit of InvestmentsDocument10 pagesPractice Problems - Audit of InvestmentsAnthoni BacaniNo ratings yet

- CLO PrimerDocument31 pagesCLO PrimerdgnyNo ratings yet

- Seth Klarman Letter 1999 PDFDocument32 pagesSeth Klarman Letter 1999 PDFBean LiiNo ratings yet

- PF Withdrawal Application (Sample Copy)Document5 pagesPF Withdrawal Application (Sample Copy)Ashok Mahanta100% (1)

- Gerrymdayanan : Prk3Crossingsalimbalan Baungon 8707bukidnonDocument6 pagesGerrymdayanan : Prk3Crossingsalimbalan Baungon 8707bukidnonGerry DayananNo ratings yet

- Income Tax Declaration Form FY 22023 24 AY2024 25Document1 pageIncome Tax Declaration Form FY 22023 24 AY2024 25mrleftyftwNo ratings yet

- Nikhil Equitas StatementDocument2 pagesNikhil Equitas Statementprem yadav100% (1)

- Charges: Wee Wei Weng KennethDocument2 pagesCharges: Wee Wei Weng KennethGeminiCrescentNo ratings yet

- Corporate DerivativesDocument13 pagesCorporate Derivativesmbilalkhan88No ratings yet

- Summer Internship Project Report On Analysis of Credit Appraisal at Bank of IndiaDocument142 pagesSummer Internship Project Report On Analysis of Credit Appraisal at Bank of IndiaSamuel Mckenzie100% (10)

- Final Webinar TWKJ July2020 PDFDocument58 pagesFinal Webinar TWKJ July2020 PDFRohit PurandareNo ratings yet

- Card Monthly Summary 10072022023013Document5 pagesCard Monthly Summary 10072022023013Marsha BaconNo ratings yet

- Documents Required for Housing Loan TakeoverDocument1 pageDocuments Required for Housing Loan TakeoverRathinder RathiNo ratings yet

- FM Question BookletDocument66 pagesFM Question Bookletdeepu deepuNo ratings yet

- 2022 Thorwallet Pitch Deck V4Document19 pages2022 Thorwallet Pitch Deck V4Guillaume VingtcentNo ratings yet

- Mt103 Qonto Bank 100 e EuroDocument2 pagesMt103 Qonto Bank 100 e Eurohaleighcrissy49387No ratings yet

- Petronesa 5.99%Document6 pagesPetronesa 5.99%akaiNo ratings yet

- Solution - Problems and Solutions Chap 10Document6 pagesSolution - Problems and Solutions Chap 10سارة الهاشميNo ratings yet

- Drill AccountingDocument17 pagesDrill AccountingRobert CastilloNo ratings yet

- Simple Interest Formula and ProblemsDocument4 pagesSimple Interest Formula and ProblemsTAภaу ЎALLaмᎥlliNo ratings yet