You might also like

- 17Mb221 Industrial Relations and Labour LawsDocument2 pages17Mb221 Industrial Relations and Labour LawsshubhamNo ratings yet

- Internship Confidentiality AgreementDocument5 pagesInternship Confidentiality AgreementMonique AcostaNo ratings yet

- Ortigas vs Feati Bank zoning caseDocument2 pagesOrtigas vs Feati Bank zoning caseEstel Tabumfama100% (4)

- Last Holographic WillDocument2 pagesLast Holographic WillJenny Reyes60% (5)

- Provisional Remedy Under RA 9372Document10 pagesProvisional Remedy Under RA 9372Larry Fritz SignabonNo ratings yet

- Rules of Procedure For Environmental Cases - Salient FeaturesDocument9 pagesRules of Procedure For Environmental Cases - Salient FeaturesIleenMaeNo ratings yet

- ELMER MONTERO VS MonteroDocument1 pageELMER MONTERO VS MonteroJax Jax100% (2)

- City of Columbus Reaches Settlement Agreement With Plaintiffs in Alsaada v. ColumbusDocument2 pagesCity of Columbus Reaches Settlement Agreement With Plaintiffs in Alsaada v. ColumbusABC6/FOX28No ratings yet

- CAGAYAN STATE UNIVERSITY TECHNOLOGY LIVELIHOOD EDUCATION CLUB CONSTITUTIONDocument7 pagesCAGAYAN STATE UNIVERSITY TECHNOLOGY LIVELIHOOD EDUCATION CLUB CONSTITUTIONjohnlloyd delarosaNo ratings yet

- Case Digests - Credit TransactionsDocument3 pagesCase Digests - Credit TransactionsMichael Christianne CabugoyNo ratings yet

- Court limits insurer's liability in bank vs guarantor caseDocument2 pagesCourt limits insurer's liability in bank vs guarantor caseces ereseNo ratings yet

- A People Power Revolution Upholds Validity of Loan ContractsDocument19 pagesA People Power Revolution Upholds Validity of Loan ContractsAbby EvangelistaNo ratings yet

- 16 Manila Electric Co Vs LimDocument1 page16 Manila Electric Co Vs Limjed_sindaNo ratings yet

- Civil Procedure Jurisdiction and Venue: Leizl A. Villapando, Mba JURIS-DOCTOR, 20201841 MARCH 13, 2021Document46 pagesCivil Procedure Jurisdiction and Venue: Leizl A. Villapando, Mba JURIS-DOCTOR, 20201841 MARCH 13, 2021Leizl A. VillapandoNo ratings yet

- Citibank v. Corpuz: Forgetting pre-trial date not valid excuseDocument2 pagesCitibank v. Corpuz: Forgetting pre-trial date not valid excuseCharisse Ayra ClamosaNo ratings yet

- 111 - Licaros v. Licaros G.R. No. 150656Document3 pages111 - Licaros v. Licaros G.R. No. 150656Joan MangampoNo ratings yet

- People Vs MamaliasDocument2 pagesPeople Vs MamaliasPrudencio Ruiz AgacitaNo ratings yet

- Teodoro v. Metropolitan Bank and CoDocument18 pagesTeodoro v. Metropolitan Bank and CoJamaika Ina CruzNo ratings yet

- #08 Borja Vs AddisonDocument2 pages#08 Borja Vs AddisonSRB4No ratings yet

- Allied Banking Corp. vs. CA, 284 SCRA 357Document2 pagesAllied Banking Corp. vs. CA, 284 SCRA 357Gilda P. OstolNo ratings yet

- Lisondra v. MegacraftDocument3 pagesLisondra v. MegacraftDNAANo ratings yet

- Perfecto vs. EsideraDocument2 pagesPerfecto vs. EsideraRaymond DiazNo ratings yet

- Mindanao Bus Co. vs City Assessor Ruling on Immobilization of EquipmentDocument1 pageMindanao Bus Co. vs City Assessor Ruling on Immobilization of Equipment123abc456defNo ratings yet

- People Vs Tio Won ChuaDocument1 pagePeople Vs Tio Won ChuaAshley CandiceNo ratings yet

- Everson V Board of EducationDocument1 pageEverson V Board of Educationmich3300No ratings yet

- Re Conviction of Judge Adoracion G AngelesDocument3 pagesRe Conviction of Judge Adoracion G AngelesJoey MapaNo ratings yet

- Ursal v. CTADocument1 pageUrsal v. CTAd2015member100% (1)

- TIDCORP vs. Asia PacesDocument2 pagesTIDCORP vs. Asia PacesAdrian GorgonioNo ratings yet

- 3Document11 pages3Emman FernandezNo ratings yet

- People Vs TulaganDocument50 pagesPeople Vs Tulaganbai malyanah a salmanNo ratings yet

- PALACIOS V. PEOPLE Case SummaryDocument1 pagePALACIOS V. PEOPLE Case SummaryAbigail TolabingNo ratings yet

- Crim Compilation DigestDocument6 pagesCrim Compilation DigestRey Malvin SG PallominaNo ratings yet

- SLDC V. DSWD Southern Luzon Drug Corporation, Petitioner, vs. The Department of Social Welfare and Development, EtDocument2 pagesSLDC V. DSWD Southern Luzon Drug Corporation, Petitioner, vs. The Department of Social Welfare and Development, Etyetyet100% (1)

- BSP Vs COADocument3 pagesBSP Vs COAjohn ryan anatanNo ratings yet

- Bar Ops Pilipinas 2016: MercantileDocument15 pagesBar Ops Pilipinas 2016: Mercantiletwenty19 lawNo ratings yet

- BailDocument5 pagesBailnbragasNo ratings yet

- 24 - Asian Surety at Insurance Co., Inc. Vs HerreraDocument2 pages24 - Asian Surety at Insurance Co., Inc. Vs HerreraVince Llamazares LupangoNo ratings yet

- Villanueva V PeopleDocument1 pageVillanueva V PeopleAbigail TolabingNo ratings yet

- People V. Mentoy G. R. NO. 223140 SPETMBER 4, 2019 FactsDocument1 pagePeople V. Mentoy G. R. NO. 223140 SPETMBER 4, 2019 FactsVian O.100% (1)

- Validity of search warrant and arrest of club manager for gamblingDocument1 pageValidity of search warrant and arrest of club manager for gamblingLloyd David P. VicedoNo ratings yet

- Fill in The Blanks 101-150 Family CodeDocument15 pagesFill in The Blanks 101-150 Family CodeKatherine DizonNo ratings yet

- Escheat Written Report PDFDocument23 pagesEscheat Written Report PDFPatricia Nicole BalgoaNo ratings yet

- People Vs TudtudDocument2 pagesPeople Vs TudtudjayNo ratings yet

- Problem Areas in Legal EthicsDocument23 pagesProblem Areas in Legal Ethicsybun0% (1)

- Dragon vs. Manila Banking CorporationDocument2 pagesDragon vs. Manila Banking CorporationKISSINGER REYESNo ratings yet

- SEC Case Not Prejudicial to Falsification CaseDocument2 pagesSEC Case Not Prejudicial to Falsification CaseJohn Michael ValmoresNo ratings yet

- 4 Waterousdrugcorporation Vs NLRCDocument1 page4 Waterousdrugcorporation Vs NLRCKP DAVAO CITYNo ratings yet

- 9th Batch DigestsDocument26 pages9th Batch Digestspinkblush717No ratings yet

- Macapinlac vs. Gutierrez Repide Jose C. Macapinlac, vs. Francisco Gutierrez Repide, Et Al. G.R. No. 18574 September 20, 1922Document2 pagesMacapinlac vs. Gutierrez Repide Jose C. Macapinlac, vs. Francisco Gutierrez Repide, Et Al. G.R. No. 18574 September 20, 1922Joanna May G CNo ratings yet

- Estrada vs. Ombudsman, Sandiganbayan Et - Al.Document26 pagesEstrada vs. Ombudsman, Sandiganbayan Et - Al.Stef OcsalevNo ratings yet

- Zomer Devt Co V Special Twentieth DivisionDocument3 pagesZomer Devt Co V Special Twentieth DivisionViolet Parker71% (7)

- 6 - Drugstore Assoc V National Council On Disability AffairsDocument10 pages6 - Drugstore Assoc V National Council On Disability AffairsPat EspinozaNo ratings yet

- CALTEX (PHILIPPINES), INC., Petitioner, vs. The Intermediate Appellate Court and Asia PACIFIC AIRWAYS, INC., RespondentsDocument5 pagesCALTEX (PHILIPPINES), INC., Petitioner, vs. The Intermediate Appellate Court and Asia PACIFIC AIRWAYS, INC., RespondentspatrickNo ratings yet

- BPI vs. SPOUSES YUJUICO: Deficiency claim after foreclosure is personal actionDocument2 pagesBPI vs. SPOUSES YUJUICO: Deficiency claim after foreclosure is personal actionAnonymous vTBEE2No ratings yet

- Valerio vs. Refresca Case DigestDocument3 pagesValerio vs. Refresca Case DigestssNo ratings yet

- Digest For GR 87434Document2 pagesDigest For GR 87434Jec Luceriaga Biraquit67% (3)

- NPC Vs Co DigestDocument2 pagesNPC Vs Co DigestVanityHughNo ratings yet

- Ante V UP DigestDocument8 pagesAnte V UP DigestDonamir CatorNo ratings yet

- Hacienda Luisita, Inc. Vs PARC (Resolution) 670 SCRA 392Document11 pagesHacienda Luisita, Inc. Vs PARC (Resolution) 670 SCRA 392Jovelan V. EscañoNo ratings yet

- RULE 91 DigestDocument4 pagesRULE 91 DigestYvone BaduyenNo ratings yet

- Ombudsman Jurisdiction Over Murder Case Against GovernorDocument5 pagesOmbudsman Jurisdiction Over Murder Case Against GovernorjazrethNo ratings yet

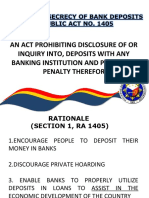

- The Law On Secrecy of Bank DepositsDocument17 pagesThe Law On Secrecy of Bank DepositsMakoy BixenmanNo ratings yet

- Sangguniang Panlungsod NG Baguio City v. Jadewell Parking Systems CorporationDocument2 pagesSangguniang Panlungsod NG Baguio City v. Jadewell Parking Systems CorporationRafaelNo ratings yet

- Drugstore Assoc of The PH Vs NCDADocument11 pagesDrugstore Assoc of The PH Vs NCDACistron ExonNo ratings yet

- Cases BankingDocument52 pagesCases BankingDane Pauline AdoraNo ratings yet

- PNB v. AlondayDocument8 pagesPNB v. AlondayMikkaEllaAnclaNo ratings yet

- PNB Vs AbelloDocument8 pagesPNB Vs AbelloERWINLAV2000No ratings yet

- VIVE EAGLE LAND Vs NHMFCDocument2 pagesVIVE EAGLE LAND Vs NHMFCJax JaxNo ratings yet

- Supreme Court issues resolution on impeachment recordsDocument31 pagesSupreme Court issues resolution on impeachment recordsJames Glendon PialagoNo ratings yet

- HEIRS OF FERNANDO Et Al VS HEIRS OF RAMOS Et AlDocument2 pagesHEIRS OF FERNANDO Et Al VS HEIRS OF RAMOS Et AlJax JaxNo ratings yet

- Court Petition for Protection from Military SurveillanceDocument1 pageCourt Petition for Protection from Military SurveillanceJax JaxNo ratings yet

- Does A Court Order For Support Prove A Child Is YoursDocument1 pageDoes A Court Order For Support Prove A Child Is YoursJax JaxNo ratings yet

- Termination Letter Template 10Document1 pageTermination Letter Template 10Jax JaxNo ratings yet

- 2016 Suggested Answers in Mercantile LawDocument13 pages2016 Suggested Answers in Mercantile LawGemays Chong100% (1)

- NoticeDocument1 pageNoticeJax JaxNo ratings yet

- Termination LetterDocument1 pageTermination LetterJax JaxNo ratings yet

- What Other Evidence Proves PaternityDocument1 pageWhat Other Evidence Proves PaternityJax JaxNo ratings yet

- SAAMPLE Letter of TerminationDocument1 pageSAAMPLE Letter of TerminationJax JaxNo ratings yet

- Termination Letter Template 10Document1 pageTermination Letter Template 10Jax JaxNo ratings yet

- SCHOLASTICISM Report To Be PrintedDocument5 pagesSCHOLASTICISM Report To Be PrintedJax JaxNo ratings yet

- Supreme Court issues resolution on impeachment recordsDocument31 pagesSupreme Court issues resolution on impeachment recordsJames Glendon PialagoNo ratings yet

- Fasap v. Pal, 2008-DigestDocument10 pagesFasap v. Pal, 2008-DigestMer CeeNo ratings yet

- Title IVDocument9 pagesTitle IVJax JaxNo ratings yet

- Fasap v. Pal, 2008-DigestDocument10 pagesFasap v. Pal, 2008-DigestMer CeeNo ratings yet

- 11 Gonzales Vs NarvazaDocument4 pages11 Gonzales Vs NarvazaJax JaxNo ratings yet

- CIR VsDocument1 pageCIR VsMario BagesbesNo ratings yet

- Agabon vs. National Labor Relations CommissionDocument140 pagesAgabon vs. National Labor Relations CommissionArya StarkNo ratings yet

- Chapter 2Document2 pagesChapter 2James Ibrahim AlihNo ratings yet

- Rodriguez Vs Arroyo DigestDocument2 pagesRodriguez Vs Arroyo DigestJohn Leo SolinapNo ratings yet

- BALAO Et Al vs. GMA G.R. No. 186050 December 13, 2011 FACTS: The Siblings of James Balao, and Longid (Petitioners), Filed With TheDocument4 pagesBALAO Et Al vs. GMA G.R. No. 186050 December 13, 2011 FACTS: The Siblings of James Balao, and Longid (Petitioners), Filed With ThenadineyagoNo ratings yet

- COMELEC airtime limits violate free expressionDocument2 pagesCOMELEC airtime limits violate free expressionArahbells100% (1)

- Criminal Law (Chapter1 10)Document38 pagesCriminal Law (Chapter1 10)Fos Naitsirk EyasNo ratings yet

- Chapter 2Document2 pagesChapter 2James Ibrahim AlihNo ratings yet

- CAM-Version -1.5_ Tr-CAM formatDocument19 pagesCAM-Version -1.5_ Tr-CAM formatNikhil MohaneNo ratings yet

- The Episteme Journal of Linguistics and Literature Vol 1 No 2 - 4-An Analysis of Presupposition On President Barack ObamaDocument33 pagesThe Episteme Journal of Linguistics and Literature Vol 1 No 2 - 4-An Analysis of Presupposition On President Barack ObamaFebyNo ratings yet

- Industrial Security ConceptDocument85 pagesIndustrial Security ConceptJonathanKelly Bitonga BargasoNo ratings yet

- 35 - Motion For More Definite StatementDocument18 pages35 - Motion For More Definite StatementRipoff Report100% (1)

- FR EssayDocument3 pagesFR EssayDavid YamNo ratings yet

- Bitcoin Wallet PDFDocument2 pagesBitcoin Wallet PDFLeo LopesNo ratings yet

- (RBI) OdtDocument2 pages(RBI) OdtSheethal HGNo ratings yet

- Wa0008.Document8 pagesWa0008.Md Mehedi hasan hasanNo ratings yet

- Term Paper On Police CorruptionDocument7 pagesTerm Paper On Police Corruptionafdtzvbex100% (1)

- Standard Joist Load TablesDocument122 pagesStandard Joist Load TablesNicolas Fuentes Von KieslingNo ratings yet

- Soc Sci PT 3Document6 pagesSoc Sci PT 3Nickleson LabayNo ratings yet

- Inventory Accounting and ValuationDocument13 pagesInventory Accounting and Valuationkiema katsutoNo ratings yet

- AAC Technologies LTD (Ticker 2018) : Why Are AAC's Reported Profit Margins Higher AND Smoother Than Apple's? Part I (Full Report)Document43 pagesAAC Technologies LTD (Ticker 2018) : Why Are AAC's Reported Profit Margins Higher AND Smoother Than Apple's? Part I (Full Report)gothamcityresearch72% (18)

- Class Program: Division of Agusan Del Norte Santigo National High SchoolDocument1 pageClass Program: Division of Agusan Del Norte Santigo National High SchoolIAN CLEO B.TIAPENo ratings yet

- Life in Madinah - Farewell Pilgrimage 10AH-11AHDocument3 pagesLife in Madinah - Farewell Pilgrimage 10AH-11AHkinza yasirNo ratings yet

- FNDWRRDocument2 pagesFNDWRRCameron WrightNo ratings yet

- Case StudyDocument6 pagesCase StudyGreen Tree0% (1)

- Plato's Concept of Justice ExploredDocument35 pagesPlato's Concept of Justice ExploredTanya ChaudharyNo ratings yet

- What Is Defined As A Type of Living in Which Survival Is Based Directly or Indirectly On The Maintenance of Domesticated AnimalsDocument26 pagesWhat Is Defined As A Type of Living in Which Survival Is Based Directly or Indirectly On The Maintenance of Domesticated AnimalsJen JenNo ratings yet

- Business Studies: One Paper 3 Hours 100 MarksDocument10 pagesBusiness Studies: One Paper 3 Hours 100 MarksHARDIK ANANDNo ratings yet

- Uy v. CADocument6 pagesUy v. CAnakedfringeNo ratings yet

- COC 2021 - ROY - Finance OfficerDocument2 pagesCOC 2021 - ROY - Finance OfficerJillian V. RoyNo ratings yet

- Business Law Midterm ExamDocument6 pagesBusiness Law Midterm ExammoepoeNo ratings yet

- Characteristics Literature of Restoration PeriodDocument4 pagesCharacteristics Literature of Restoration PeriodIksan AjaNo ratings yet

- Business Studies PamphletDocument28 pagesBusiness Studies PamphletSimushi SimushiNo ratings yet

- Case Study 1 StudDocument11 pagesCase Study 1 StudLucNo ratings yet