You might also like

- Arens Aas17 PPT 07Document48 pagesArens Aas17 PPT 07Liz NegronNo ratings yet

- Treasury Manipulation ComplaintDocument61 pagesTreasury Manipulation ComplaintZerohedgeNo ratings yet

- Commercial Banks: Sustainability Accounting StandardDocument24 pagesCommercial Banks: Sustainability Accounting StandardSAGAR VAZIRANINo ratings yet

- Acceptance SamplingDocument50 pagesAcceptance SamplingSin TungNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument29 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionCharlotte ChanNo ratings yet

- Chapter 10 PPT 4th EditionDocument20 pagesChapter 10 PPT 4th EditionLinh Le Thi ThuyNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument37 pagesAuditing and Assurance Services: Seventeenth Edition, Global Edition賴宥禎100% (1)

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument34 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionChoki Coklat AsliNo ratings yet

- Auditing (Arens) 14e Chapter 2 PowerPoint SlidesDocument21 pagesAuditing (Arens) 14e Chapter 2 PowerPoint SlidesMohsin AliNo ratings yet

- Solution Manual Arens Chapter 1Document45 pagesSolution Manual Arens Chapter 1Rizal Pandu NugrohoNo ratings yet

- Audit Responsibilities and ObjectivesDocument52 pagesAudit Responsibilities and ObjectivesStudio AlphaNo ratings yet

- Advanced Accounting: Partnership LiquidationDocument33 pagesAdvanced Accounting: Partnership LiquidationVeesNo ratings yet

- Differentiate Assurance From Non-Assurance EngagementsDocument3 pagesDifferentiate Assurance From Non-Assurance EngagementsSomething ChicNo ratings yet

- Solution Manual Auditing and Assurance Services 13e by Arens Chapter 18Document35 pagesSolution Manual Auditing and Assurance Services 13e by Arens Chapter 18Thị Hải Yến TrầnNo ratings yet

- Arens Aas17 PPT 02 PDFDocument41 pagesArens Aas17 PPT 02 PDFSin TungNo ratings yet

- Arens Aud16 Inppt26Document20 pagesArens Aud16 Inppt26putri retnoNo ratings yet

- Arens Aud16 Inppt03Document40 pagesArens Aud16 Inppt03Tyasa PutriNo ratings yet

- Document PDFDocument3 pagesDocument PDFMJA50% (2)

- Chapter 6 The Search For Evidence ExplainedDocument27 pagesChapter 6 The Search For Evidence ExplainedNathali TjahjadiNo ratings yet

- Completing The Audit: Principles of Auditing: An Introduction To International Standards On AuditingDocument39 pagesCompleting The Audit: Principles of Auditing: An Introduction To International Standards On AuditingBitsca BasyaraNo ratings yet

- INVESTMENT AVENUES BLACK BOOK UpgradedDocument71 pagesINVESTMENT AVENUES BLACK BOOK UpgradedJack DawsonNo ratings yet

- Arens Auditing16e SM 15Document27 pagesArens Auditing16e SM 15김현중No ratings yet

- Horngren Ca16 PPT 16 - StudentDocument30 pagesHorngren Ca16 PPT 16 - StudentVon Andrei MedinaNo ratings yet

- Arens Aas17 PPT 01 PDFDocument38 pagesArens Aas17 PPT 01 PDFSin TungNo ratings yet

- Chapter 14 SlidesDocument26 pagesChapter 14 SlidesJc AdanNo ratings yet

- Client Acceptance: Principles of Auditing: An Introduction To International Standards On AuditingDocument23 pagesClient Acceptance: Principles of Auditing: An Introduction To International Standards On AuditingpradanawijayaNo ratings yet

- The Risk-Based Approach To Audit: Audit JudgementDocument18 pagesThe Risk-Based Approach To Audit: Audit JudgementWiratama SusetiyoNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument55 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionCharlotte Chan100% (1)

- Arens Aas17 PPT 04 PDFDocument30 pagesArens Aas17 PPT 04 PDFSin TungNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument45 pagesAuditing and Assurance Services: Seventeenth Edition, Global EditionSin TungNo ratings yet

- Auditing (Arens) 14e Chapter 4 PowerPoint SlidesDocument36 pagesAuditing (Arens) 14e Chapter 4 PowerPoint SlidesMohsin AliNo ratings yet

- Arens - Aas17 - PPT - 13-Audit of The Sales and Collection cycle-TOC+STOTDocument39 pagesArens - Aas17 - PPT - 13-Audit of The Sales and Collection cycle-TOC+STOTRayhan AlfansaNo ratings yet

- Audit Evidence: Concept Checks P. 167Document32 pagesAudit Evidence: Concept Checks P. 167hsingting yuNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument26 pagesAuditing and Assurance Services: Seventeenth Edition, Global Edition賴宥禎No ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument33 pagesAuditing and Assurance Services: Seventeenth Edition, Global Edition賴宥禎No ratings yet

- Chapter 1 PowerpointDocument50 pagesChapter 1 PowerpointRajNo ratings yet

- Auditing: Integral To The EconomyDocument47 pagesAuditing: Integral To The EconomyPei WangNo ratings yet

- Arens Aud16 Inppt07Document40 pagesArens Aud16 Inppt07euncieNo ratings yet

- 11 PPT The Audit Process Ed 6 GrayDocument23 pages11 PPT The Audit Process Ed 6 Grayina oktavianiNo ratings yet

- Auditing (Arens) 14e Chapter 3 PowerPoint SlidesDocument38 pagesAuditing (Arens) 14e Chapter 3 PowerPoint SlidesMohsin AliNo ratings yet

- Tutorial Chapter 13 - 14 Cost Management System - ABC - Pricing DecisionsDocument42 pagesTutorial Chapter 13 - 14 Cost Management System - ABC - Pricing DecisionsNaKib NahriNo ratings yet

- Anderson and Zinder, P.C., CpasDocument3 pagesAnderson and Zinder, P.C., CpasJack BurtonNo ratings yet

- Audit Sampling For Tests of Details of BalancesDocument43 pagesAudit Sampling For Tests of Details of BalancesEndah Hamidah AiniNo ratings yet

- The Demand For Audit and Other Assurance ServicesDocument41 pagesThe Demand For Audit and Other Assurance ServicesMamatz Fth-winter100% (1)

- Romney Ais13 PPT 13Document11 pagesRomney Ais13 PPT 13Aj PotXzs ÜNo ratings yet

- Chapter 12 - Audit Reports and Communication: Rick Hayes, Hans Gortemaker and Philip WallageDocument42 pagesChapter 12 - Audit Reports and Communication: Rick Hayes, Hans Gortemaker and Philip WallageMichael AnthonyNo ratings yet

- Chapter 14 Segment and Interim Financial ReportingDocument38 pagesChapter 14 Segment and Interim Financial ReportingFauzi Achmad100% (1)

- Fundamentals of Cost Management: True / False QuestionsDocument238 pagesFundamentals of Cost Management: True / False QuestionsElaine GimarinoNo ratings yet

- Auditing and Assurance ServicesDocument49 pagesAuditing and Assurance Servicesgilli1tr100% (1)

- Chapter 6Document17 pagesChapter 6MM M83% (6)

- Arens14e ch07 PPTDocument43 pagesArens14e ch07 PPTNindya Harum SolichaNo ratings yet

- MCS University Paper Solutions May 2001 to May 2011Document207 pagesMCS University Paper Solutions May 2001 to May 2011Suhana SharmaNo ratings yet

- Name: Safira Yafiq Khairani NIM: 1802112130 Review Question Chapter 16Document9 pagesName: Safira Yafiq Khairani NIM: 1802112130 Review Question Chapter 16Safira KhairaniNo ratings yet

- Cost Management ch1Document34 pagesCost Management ch1Ahmed DapoorNo ratings yet

- Formation of a Partnership AccountsDocument27 pagesFormation of a Partnership Accountssamuel debebeNo ratings yet

- CH 1 Overview AuditingDocument40 pagesCH 1 Overview AuditingMHWCORPS PRODUCTION100% (2)

- Controls For Information SecurityDocument14 pagesControls For Information Securitymuhammad f laitupaNo ratings yet

- Test ch7 Audit Test BankDocument45 pagesTest ch7 Audit Test BankFlorenz Nicole PalisocNo ratings yet

- Accounting Principles II Chapter 1: Cash and ReceivablesDocument101 pagesAccounting Principles II Chapter 1: Cash and ReceivablesAnimaw YayehNo ratings yet

- Chapter 2 (Tan&Lee)Document47 pagesChapter 2 (Tan&Lee)desy nataNo ratings yet

- Completing The Tests in The Acquisition and Payment Cycle: Verification of Selected AccountsDocument32 pagesCompleting The Tests in The Acquisition and Payment Cycle: Verification of Selected AccountsNhung KiềuNo ratings yet

- Cost Accounting: Sixteenth Edition, Global EditionDocument35 pagesCost Accounting: Sixteenth Edition, Global EditionvalerieNo ratings yet

- Acct4131 CH1Document38 pagesAcct4131 CH1tinkeyhui.tt.2003No ratings yet

- Chapter 6 Financial Auditing SlidesDocument19 pagesChapter 6 Financial Auditing SlidesLuong Thao LinhNo ratings yet

- Module 2 - Introduction To FS AuditDocument5 pagesModule 2 - Introduction To FS AuditLysss EpssssNo ratings yet

- Topic 4 QuestionsDocument14 pagesTopic 4 QuestionsSin TungNo ratings yet

- Topic 4 Materials (Part 2)Document18 pagesTopic 4 Materials (Part 2)Sin TungNo ratings yet

- Topic 3 QuestionsDocument11 pagesTopic 3 QuestionsSin TungNo ratings yet

- Shareholders and company meetings explainedDocument13 pagesShareholders and company meetings explainedSin TungNo ratings yet

- Week 6 Part IDocument24 pagesWeek 6 Part ISin TungNo ratings yet

- 2.1 Multiple Choice Questions (Circle The Correct Answer, 2 Points Each)Document3 pages2.1 Multiple Choice Questions (Circle The Correct Answer, 2 Points Each)Kyle Lee UyNo ratings yet

- Week 5 Part IDocument29 pagesWeek 5 Part ISin TungNo ratings yet

- Week 5 Part IIDocument17 pagesWeek 5 Part IISin TungNo ratings yet

- Business Combinations: Answers To Questions 1Document12 pagesBusiness Combinations: Answers To Questions 1Sin TungNo ratings yet

- Topic 3 Materials (Part 2)Document26 pagesTopic 3 Materials (Part 2)Sin TungNo ratings yet

- Week 4 - Cont. Week 3 Slides - UpdatedDocument43 pagesWeek 4 - Cont. Week 3 Slides - UpdatedSin TungNo ratings yet

- Week 4 - Product Mix DecisionsDocument17 pagesWeek 4 - Product Mix DecisionsSin TungNo ratings yet

- Advanced Accounting: Business CombinationsDocument43 pagesAdvanced Accounting: Business CombinationsSin TungNo ratings yet

- Week 4 Learning CurveDocument3 pagesWeek 4 Learning CurveSin TungNo ratings yet

- Ch1 Handout QuestionsDocument2 pagesCh1 Handout QuestionsSin TungNo ratings yet

- Week by Week Analysis of Customer Service Department Costs and PerformanceDocument11 pagesWeek by Week Analysis of Customer Service Department Costs and PerformanceSin TungNo ratings yet

- Basic Seven ToolsDocument33 pagesBasic Seven ToolsSin TungNo ratings yet

- Ch1 Handout QuestionsDocument2 pagesCh1 Handout QuestionsSin TungNo ratings yet

- Swim Lane Flow ChartDocument1 pageSwim Lane Flow ChartSin TungNo ratings yet

- Total Cost 30,050,000 28,950,000 26,750,000Document2 pagesTotal Cost 30,050,000 28,950,000 26,750,000Sin TungNo ratings yet

- Week 4 LP Excel Solver SolutionDocument3 pagesWeek 4 LP Excel Solver SolutionSin TungNo ratings yet

- Samsung quality complaints analysisDocument1 pageSamsung quality complaints analysisSin Tung0% (1)

- 3730 Inclass Flowchart 1Document2 pages3730 Inclass Flowchart 1Sin TungNo ratings yet

- Spring 2020 ISOM3730 Quiz Solution: Depth Analysis To Score Full CreditDocument5 pagesSpring 2020 ISOM3730 Quiz Solution: Depth Analysis To Score Full CreditSin TungNo ratings yet

- Quality Wireless (A) and (B) : Process CapabilityDocument3 pagesQuality Wireless (A) and (B) : Process CapabilitySin TungNo ratings yet

- And In-Depth Analysis To Score Full Credit.: Spring 2020 ISOM3730 Final Exam SolutionDocument5 pagesAnd In-Depth Analysis To Score Full Credit.: Spring 2020 ISOM3730 Final Exam SolutionSin TungNo ratings yet

- 3730 Uber Present ScriptDocument2 pages3730 Uber Present ScriptSin TungNo ratings yet

- SUST 1000 (L4) Introduction To Sustainability: Group 1 - MongoliaDocument3 pagesSUST 1000 (L4) Introduction To Sustainability: Group 1 - MongoliaSin TungNo ratings yet

- Financial Services: Mutual Fund and Hedge Fund Companies: True / False QuestionsDocument32 pagesFinancial Services: Mutual Fund and Hedge Fund Companies: True / False Questionslatifa hnNo ratings yet

- Assignment 1Document21 pagesAssignment 1siddhant jainNo ratings yet

- APP ScenariosDocument18 pagesAPP Scenariosanand chawanNo ratings yet

- Specialised Accouning Ques BankDocument31 pagesSpecialised Accouning Ques BankMayra AzharNo ratings yet

- CV Fifa Jaya Sport - Memorial JournalDocument6 pagesCV Fifa Jaya Sport - Memorial JournalMiskaNo ratings yet

- Board of Directors StructureDocument3 pagesBoard of Directors StructureMoamar Dalawis IsmulaNo ratings yet

- Directorate of Treasuries and Accounts, Department of Finance, Punjab Manual (XVII)Document76 pagesDirectorate of Treasuries and Accounts, Department of Finance, Punjab Manual (XVII)Pankaj kumarNo ratings yet

- Wealth-Lab Developer 6.9 Performance: Strategy: Channel Breakout VT Dataset/Symbol: AALDocument1 pageWealth-Lab Developer 6.9 Performance: Strategy: Channel Breakout VT Dataset/Symbol: AALHamahid pourNo ratings yet

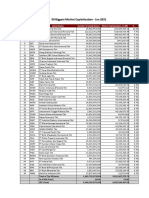

- 50 Biggest Market Capitalization - Jan 2021Document1 page50 Biggest Market Capitalization - Jan 2021Aditya WidiyadiNo ratings yet

- Form 1040A or 1040Document2 pagesForm 1040A or 1040Vita Volunteers WebmasterNo ratings yet

- Fortune Oil Annual Report 2014 - 5th - Clean - 0724Document37 pagesFortune Oil Annual Report 2014 - 5th - Clean - 0724Meng KeNo ratings yet

- Acc Clerk Chapter 4b-Preparing Trial BalanceDocument15 pagesAcc Clerk Chapter 4b-Preparing Trial BalanceEphraim PryceNo ratings yet

- MAhmed 37 18989 6 Questions Stock ValuationDocument2 pagesMAhmed 37 18989 6 Questions Stock ValuationAR LEGENDS0% (1)

- Purchases Day BookDocument8 pagesPurchases Day Bookdrishti.singh0609No ratings yet

- Saral Jeevan Bima Brochure-BRDocument10 pagesSaral Jeevan Bima Brochure-BRprabuNo ratings yet

- Explain Origin of Commercial BankingDocument6 pagesExplain Origin of Commercial Bankingዳግማዊ ጌታነህ ግዛው ባይህNo ratings yet

- Resume - CA Anuja RedkarDocument2 pagesResume - CA Anuja RedkarPACreatives ShortFilmsNo ratings yet

- Chap-17-Lending Policies and ProceduresDocument30 pagesChap-17-Lending Policies and ProceduresNazmul H. PalashNo ratings yet

- Lesson 29 - General AnnuitiesDocument67 pagesLesson 29 - General AnnuitiesAlfredo LabadorNo ratings yet

- Investment Declaration Form 2012-13 PDFDocument1 pageInvestment Declaration Form 2012-13 PDFnovalhemantNo ratings yet

- Covering Letter To Bank or Building SocietyDocument3 pagesCovering Letter To Bank or Building SocietyNick SiddallNo ratings yet

- HDFCDocument36 pagesHDFCdarshan.babu.mclarenNo ratings yet

- PFM Training Program Syllabus v1Document5 pagesPFM Training Program Syllabus v1Lukas FagoloNo ratings yet

- Maintaining Financial Records (FA2) : Syllabus and Study GuideDocument14 pagesMaintaining Financial Records (FA2) : Syllabus and Study GuideAhmar KhalilNo ratings yet

- Government Accounting Quizzes and ExamsDocument118 pagesGovernment Accounting Quizzes and ExamsBrian Torres100% (1)

- (224888313) Financial-Plan AnupamDocument23 pages(224888313) Financial-Plan AnupamShresth KotishNo ratings yet