You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Startup Companies - PowerPointDocument16 pagesStartup Companies - PowerPointFranklin Rege100% (1)

- Exhibits To Full Deposition of Patricia Arango of Marshall C WatsonDocument25 pagesExhibits To Full Deposition of Patricia Arango of Marshall C WatsonForeclosure FraudNo ratings yet

- Chapter 14Document43 pagesChapter 14Dominic RomeroNo ratings yet

- Approval SheetDocument5 pagesApproval SheetJoseph AlogNo ratings yet

- Chapter 08 Auditor's Legal LiabilityDocument20 pagesChapter 08 Auditor's Legal LiabilityRichard de LeonNo ratings yet

- Accounting For Decision Making or Management AU Question Paper'sDocument41 pagesAccounting For Decision Making or Management AU Question Paper'sAdhithiya dhanasekarNo ratings yet

- Research ProposalDocument11 pagesResearch ProposalQaiser Khalil100% (1)

- 02 Entrepreneurship Skills Complete NotesDocument17 pages02 Entrepreneurship Skills Complete Notesopolla nianorNo ratings yet

- Understanding Financial Leverage RatiosDocument17 pagesUnderstanding Financial Leverage RatiosChristian Jasper M. LigsonNo ratings yet

- Notes and Solutions of The Math of Financial Derivatives Wilmott PDFDocument224 pagesNotes and Solutions of The Math of Financial Derivatives Wilmott PDFKiers100% (1)

- Importance of TaxDocument6 pagesImportance of Taxmahabalu123456789No ratings yet

- Mergers, Acquisitions and RestructuringDocument34 pagesMergers, Acquisitions and RestructuringMunna JiNo ratings yet

- Role of ICT in Agricultural Marketing and Extension-Satyaveer Singh, DR Krishna GuptaDocument11 pagesRole of ICT in Agricultural Marketing and Extension-Satyaveer Singh, DR Krishna Guptaeletsonline100% (1)

- F 4506Document2 pagesF 4506kittie_86No ratings yet

- Taxation Short Questions AnswersDocument4 pagesTaxation Short Questions AnswersSheetal IyerNo ratings yet

- Katwa 803Document5 pagesKatwa 803Movies ActionNo ratings yet

- NFLX Initiating Coverage JSDocument12 pagesNFLX Initiating Coverage JSBrian BolanNo ratings yet

- Arkwright - Water Frame RulesDocument36 pagesArkwright - Water Frame RulestobymaoNo ratings yet

- Final Draft Ifp 2018 PDFDocument443 pagesFinal Draft Ifp 2018 PDFhusnasyahidahNo ratings yet

- Assignment (Graded) # 3: InstructionsDocument4 pagesAssignment (Graded) # 3: Instructionsatifatanvir1758No ratings yet

- General Power of AttorneyDocument1 pageGeneral Power of AttorneyAriel Hartung100% (1)

- Role of SMEs in Indian EconomyDocument25 pagesRole of SMEs in Indian Economyyatheesh07No ratings yet

- J.M. Hurst - The Profit Magic of Stock Transaction TimingDocument3 pagesJ.M. Hurst - The Profit Magic of Stock Transaction TimingKristin WalkerNo ratings yet

- Alluvial Capital Management Q2 2021 Letter To PartnersDocument8 pagesAlluvial Capital Management Q2 2021 Letter To Partnersl chanNo ratings yet

- Updated - Ooredoo at A Glance 2019Document11 pagesUpdated - Ooredoo at A Glance 2019AMR ERFANNo ratings yet

- Rep 0108122609Document104 pagesRep 0108122609Dr Luis e Valdez ricoNo ratings yet

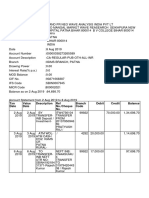

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNo ratings yet

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- CASFLOWDocument133 pagesCASFLOWalenNo ratings yet

- Executive Summary - Honolulu Rail Transit Financial Plan AssessmentDocument21 pagesExecutive Summary - Honolulu Rail Transit Financial Plan AssessmentCraig GimaNo ratings yet