You might also like

- Sale DeedDocument5 pagesSale DeedNitin GoyalNo ratings yet

- Income Declaration Scheme Rules, 2016: Form 1Document9 pagesIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatNo ratings yet

- Banca SuranceDocument32 pagesBanca SuranceNikhil KasatNo ratings yet

- Hedging With Financial DerivativesDocument30 pagesHedging With Financial DerivativesNikhil KasatNo ratings yet

- Types of stamps and concepts of stamp dutyDocument5 pagesTypes of stamps and concepts of stamp dutyNikhil Kasat100% (2)

- Derivatives Markets in Interest Rate & Foreign Exchange RateDocument20 pagesDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfNo ratings yet

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Document21 pagesSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatNo ratings yet

- DTL Sec 10Document14 pagesDTL Sec 10Nikhil KasatNo ratings yet

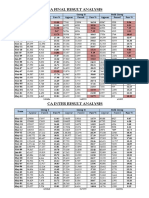

- CA Result AnalysisDocument1 pageCA Result AnalysisNikhil KasatNo ratings yet

- Black Money BillDocument30 pagesBlack Money BillNikhil KasatNo ratings yet

- BLack Money RulesDocument23 pagesBLack Money RulesLive LawNo ratings yet

- Directors Report As Per StatusDocument5 pagesDirectors Report As Per StatusNikhil KasatNo ratings yet

- Calculate Fees and Stamp Duty for Increase in Authorised Share CapitalDocument10 pagesCalculate Fees and Stamp Duty for Increase in Authorised Share CapitalNikhil KasatNo ratings yet

- Delhi Dvat Registration InformationDocument4 pagesDelhi Dvat Registration InformationNikhil KasatNo ratings yet

- Privileges To Small CompaniesDocument2 pagesPrivileges To Small CompaniesNikhil KasatNo ratings yet

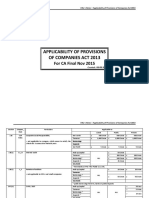

- ApplicabiliTY of ProvisionsDocument3 pagesApplicabiliTY of ProvisionsNikhil KasatNo ratings yet

- How to score 12-14 marks on Professional Ethics exam questionsDocument2 pagesHow to score 12-14 marks on Professional Ethics exam questionsNikhil KasatNo ratings yet

- Curriculum VitaeDocument13 pagesCurriculum VitaeNikhil KasatNo ratings yet

- List of Indian As Convergence With IfrsDocument1 pageList of Indian As Convergence With IfrsNikhil KasatNo ratings yet

- Web Base Timesheet ApplicationDocument4 pagesWeb Base Timesheet ApplicationNikhil KasatNo ratings yet

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDocument9 pagesAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatNo ratings yet

- Valuation of InventoriesDocument4 pagesValuation of InventoriesNikhil KasatNo ratings yet

- August Month CompliancesDocument1 pageAugust Month CompliancesNikhil KasatNo ratings yet

- Anf 4dDocument3 pagesAnf 4dNikhil KasatNo ratings yet

- Ind As 2015Document2 pagesInd As 2015Nikhil KasatNo ratings yet

- Tds On SalariesDocument55 pagesTds On SalariespunitNo ratings yet

- CUSTOMS VALUATION COMPUTATIONDocument8 pagesCUSTOMS VALUATION COMPUTATIONNikhil KasatNo ratings yet

- Importance of ArticleshipDocument6 pagesImportance of ArticleshipNikhil KasatNo ratings yet

- C01Document23 pagesC01Silvery DoeNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- PROBLEMS WITH CONSUMER CHOICEDocument9 pagesPROBLEMS WITH CONSUMER CHOICEPavan kumar GulimiNo ratings yet

- ASM404Document7 pagesASM404Alia najwaNo ratings yet

- StylecrackerDocument14 pagesStylecrackerNavya Sood0% (1)

- Questionnaire on Social Media MarketingDocument6 pagesQuestionnaire on Social Media MarketingAllwinNo ratings yet

- Jampason, Initao, Misamis Oriental 1st Semester, S.Y. 2020 - 2021Document1 pageJampason, Initao, Misamis Oriental 1st Semester, S.Y. 2020 - 2021Rina LopezNo ratings yet

- Lesson 9 Recognizing The Importance of Marketing Mix I Part 1 The Development of Marketing Strategies NOTESDocument6 pagesLesson 9 Recognizing The Importance of Marketing Mix I Part 1 The Development of Marketing Strategies NOTESShunuan Huang100% (2)

- Marketing Plan of Chik ShampooDocument5 pagesMarketing Plan of Chik ShampooSiddharth UdyawarNo ratings yet

- Cars24 New Cars Buying VerticalDocument41 pagesCars24 New Cars Buying VerticalPriyal Singhal100% (1)

- Types of Retailers: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedDocument52 pagesTypes of Retailers: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedSteven LohNo ratings yet

- Elective List - Term - V - ERP Portal - 2019-21Document380 pagesElective List - Term - V - ERP Portal - 2019-21Sakshi ShahNo ratings yet

- Red-Bull - Marketing Mix PDFDocument4 pagesRed-Bull - Marketing Mix PDFEdward WingNo ratings yet

- Cpa Traffic Guide PDFDocument89 pagesCpa Traffic Guide PDFAikut AbdykadyrovNo ratings yet

- Business: Accounting, Finance, Management & MarketingDocument137 pagesBusiness: Accounting, Finance, Management & MarketingKaiqueSilvaNo ratings yet

- Digital Transformation - A Guide For ManagerDocument129 pagesDigital Transformation - A Guide For ManagerJOSE DIAZNo ratings yet

- Why Business Uses The InternetDocument4 pagesWhy Business Uses The InternetJonathanNo ratings yet

- Hasbro's New Toy Requires Unique Marketing StrategyDocument11 pagesHasbro's New Toy Requires Unique Marketing StrategyAshutosh kumarNo ratings yet

- Mirror MazeDocument15 pagesMirror MazeSushovan AmatyaNo ratings yet

- Book of Papers M-Sphere 2015Document441 pagesBook of Papers M-Sphere 2015Tamás KozákNo ratings yet

- XLRI BrochureDocument8 pagesXLRI BrochureAbhishek KukrejaNo ratings yet

- SAP SD Frequently Asked Questions1Document2 pagesSAP SD Frequently Asked Questions1Kamal BatraNo ratings yet

- MarketSpeakYamunaNagar - RAJESH MASKARADocument1 pageMarketSpeakYamunaNagar - RAJESH MASKARAShubham KumarNo ratings yet

- English For Medical Science Syllabus (Example)Document6 pagesEnglish For Medical Science Syllabus (Example)Leng Villeza50% (2)

- By Gunnlaugur Arnar Elíasson, Sandra Ósk Kristbjarnardóttir and Clara Sofia Escobar LopezDocument15 pagesBy Gunnlaugur Arnar Elíasson, Sandra Ósk Kristbjarnardóttir and Clara Sofia Escobar Lopezbeatriz_ledesma_2No ratings yet

- Indian Post Office - Redefining DistributionDocument10 pagesIndian Post Office - Redefining DistributionBushalNo ratings yet

- Freecharge Company Background and BenefitsDocument11 pagesFreecharge Company Background and BenefitsneetugNo ratings yet

- Industrial SalesmenDocument9 pagesIndustrial Salesmenmaher76No ratings yet

- Strategic Management - The Shopee StoryDocument6 pagesStrategic Management - The Shopee StoryNoor Hairulnizam NasirNo ratings yet

- Passage No 34Document10 pagesPassage No 34SanchitNo ratings yet

- RiskDocument1 pageRiskJohn Dee Hortelano100% (1)

- Midas Advertising Marketing ProjectDocument14 pagesMidas Advertising Marketing ProjectNauman RashidNo ratings yet