You might also like

- Derivatives 120821000932 Phpapp02Document54 pagesDerivatives 120821000932 Phpapp02Choco ChocoNo ratings yet

- Financial DerivavtivesDocument22 pagesFinancial DerivavtivesAlfe PinongpongNo ratings yet

- OTC Market Meaning: What is Traded Over-the-CounterDocument6 pagesOTC Market Meaning: What is Traded Over-the-CounterAman NegiNo ratings yet

- Derivatives: Prof Mahesh Kumar Amity Business SchoolDocument56 pagesDerivatives: Prof Mahesh Kumar Amity Business SchoolasifanisNo ratings yet

- Chapter VI DerivativesDocument36 pagesChapter VI Derivativesmulutsega yacobNo ratings yet

- What Does Derivative Mean?Document23 pagesWhat Does Derivative Mean?shrikantyemulNo ratings yet

- International DerivativesDocument56 pagesInternational DerivativesPradyumna SwainNo ratings yet

- Derivatives Explained: Futures, Forwards, Options & SwapsDocument11 pagesDerivatives Explained: Futures, Forwards, Options & SwapsSanchit KaushalNo ratings yet

- Derivatives and Risk Management: Answers To Beginning-Of-Chapter QuestionsDocument13 pagesDerivatives and Risk Management: Answers To Beginning-Of-Chapter QuestionsRiri FahraniNo ratings yet

- Derivatives Note SeminarDocument7 pagesDerivatives Note SeminarCA Vikas NevatiaNo ratings yet

- DERIVATIVES AND RISK MANAGEMENTDocument4 pagesDERIVATIVES AND RISK MANAGEMENTbhumishahNo ratings yet

- CUHK RMSC2001 Chapter 6 NotesDocument17 pagesCUHK RMSC2001 Chapter 6 NotesanthetNo ratings yet

- AMA535: Mathematics of Derivative PricingDocument46 pagesAMA535: Mathematics of Derivative PricingYu XinNo ratings yet

- Accounting for DerivativesDocument9 pagesAccounting for DerivativesEricka AlimNo ratings yet

- Derivatives & OptionsDocument30 pagesDerivatives & OptionsakshastarNo ratings yet

- Financial Security: Best Online Brokers)Document7 pagesFinancial Security: Best Online Brokers)Khabele LenkoeNo ratings yet

- Types of Financial Risk and Derivatives ExplainedDocument4 pagesTypes of Financial Risk and Derivatives ExplainedChristine CaridoNo ratings yet

- Derivatives and Commodity ExchangesDocument53 pagesDerivatives and Commodity ExchangesMonika GoelNo ratings yet

- Foreign Exchange Exposures - IFMDocument7 pagesForeign Exchange Exposures - IFMDivya SindheyNo ratings yet

- RatiosDocument15 pagesRatiosAmirah AzmiNo ratings yet

- Accounting for Derivatives and Hedge Relationships under PFRS 9Document9 pagesAccounting for Derivatives and Hedge Relationships under PFRS 9Mary Yvonne AresNo ratings yet

- Risk management and derivativesDocument8 pagesRisk management and derivativesIm NayeonNo ratings yet

- Derivatives: You Need To Know About Derivatives TradingDocument35 pagesDerivatives: You Need To Know About Derivatives TradingPooja mahadikNo ratings yet

- Derivatives Instruments GuideDocument20 pagesDerivatives Instruments GuideKhyati MistryNo ratings yet

- WLH Finance CompilationDocument58 pagesWLH Finance CompilationSandhya S 17240No ratings yet

- Topic 8 Managing Risk New 1233829259255133 3Document17 pagesTopic 8 Managing Risk New 1233829259255133 3aasif383No ratings yet

- WORK SHEET - Financial Derivatives: Q1) Enumerate The Basic Differences Between Forward and Futures ContractsDocument5 pagesWORK SHEET - Financial Derivatives: Q1) Enumerate The Basic Differences Between Forward and Futures ContractsBhavesh RathiNo ratings yet

- Week 8 Financial Instruments - Hedging - Options and SwapsDocument20 pagesWeek 8 Financial Instruments - Hedging - Options and SwapsOv NomaanNo ratings yet

- Derivatives and Risk Management: What Does Forward Contract MeanDocument9 pagesDerivatives and Risk Management: What Does Forward Contract MeanMd Hafizul HaqueNo ratings yet

- Financial Derivative Instruments in Bangladesh: DefinitionDocument4 pagesFinancial Derivative Instruments in Bangladesh: DefinitionJahid AhnafNo ratings yet

- DERIVATIVESDocument30 pagesDERIVATIVESDeepak ParidaNo ratings yet

- What Are FuturesDocument4 pagesWhat Are FuturesGrace G. ServanoNo ratings yet

- Risk Management Cheat Sheet Risk Management Cheat SheetDocument4 pagesRisk Management Cheat Sheet Risk Management Cheat SheetEdithNo ratings yet

- Basis Risk, Options Risk, Structure Risk, and Repricing Risk.Document4 pagesBasis Risk, Options Risk, Structure Risk, and Repricing Risk.Puja DuaNo ratings yet

- FN - 04Document6 pagesFN - 04abhiNo ratings yet

- International Financial Management Techniques To Mitigate RiskDocument27 pagesInternational Financial Management Techniques To Mitigate RiskAsra HakakNo ratings yet

- What is a Futures ContractDocument4 pagesWhat is a Futures Contractareesakhtar100% (1)

- Basics of Investment Banking DomainDocument15 pagesBasics of Investment Banking DomainChakravarthi ChiluveruNo ratings yet

- Reviewed By: DerivativeDocument10 pagesReviewed By: DerivativefrancisNo ratings yet

- FD Bcom Module 1Document75 pagesFD Bcom Module 1Mandy RandiNo ratings yet

- Hedging Strategies ExplainedDocument28 pagesHedging Strategies ExplainedNadeem AhmadNo ratings yet

- DRM-Intro To DerivativesDocument6 pagesDRM-Intro To Derivativeschandu prakashNo ratings yet

- Foreign Currency Derivatives GuideDocument4 pagesForeign Currency Derivatives GuideÂn TrầnNo ratings yet

- Forward and Futures ContractsDocument29 pagesForward and Futures ContractsMaulik ShahNo ratings yet

- Introduction to Derivatives BasicsDocument29 pagesIntroduction to Derivatives BasicsRaheel SiddiquiNo ratings yet

- 02 Lecture21Document29 pages02 Lecture21Ashi GargNo ratings yet

- How Companies Use Derivatives For Hedging & Risk ManagementDocument17 pagesHow Companies Use Derivatives For Hedging & Risk ManagementBinitha B NairNo ratings yet

- Dividend Yield: RecapitalisationDocument6 pagesDividend Yield: RecapitalisationArun NadarNo ratings yet

- What Are DerivativesDocument11 pagesWhat Are DerivativesJayash KaushalNo ratings yet

- Chapter 6Document5 pagesChapter 6Muhammed YismawNo ratings yet

- Derivatives: Introduction To Derivatives: Meaning, Types, Uses and ClassificationDocument17 pagesDerivatives: Introduction To Derivatives: Meaning, Types, Uses and ClassificationAlok PandeyNo ratings yet

- Ca - Final - SFM TheoryDocument13 pagesCa - Final - SFM TheoryPravinn_MahajanNo ratings yet

- Chap001 RevisedDocument43 pagesChap001 Revisedp6yq4n9ykjNo ratings yet

- What Are Futures and ForwardsDocument22 pagesWhat Are Futures and ForwardsMuneeza AzharNo ratings yet

- Interest Rate Derivatives Credit Default Swaps Currency DerivativesDocument30 pagesInterest Rate Derivatives Credit Default Swaps Currency DerivativesAtul JainNo ratings yet

- Basics of DeivativesDocument9 pagesBasics of DeivativesGaurav ThigaleNo ratings yet

- Mortgage Markets and Derivatives - AnswerDocument3 pagesMortgage Markets and Derivatives - AnswerSarang SNo ratings yet

- Understanding Derivatives in 40 CharactersDocument10 pagesUnderstanding Derivatives in 40 CharactersSanjai SivañanthamNo ratings yet

- M M M MDocument46 pagesM M M MajithsubramanianNo ratings yet

- CreativeDocument1 pageCreativeMichael WardNo ratings yet

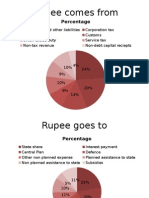

- Rupee Comes From: PercentageDocument2 pagesRupee Comes From: PercentageMichael WardNo ratings yet

- Organisational Ambidexterity Key to Long-Term SuccessDocument15 pagesOrganisational Ambidexterity Key to Long-Term SuccessMichael WardNo ratings yet

- Basel ComitteeDocument26 pagesBasel ComitteeMichael WardNo ratings yet

- AseanDocument15 pagesAseanMichael WardNo ratings yet

- Valuechainanalysis 130703070548 Phpapp01Document36 pagesValuechainanalysis 130703070548 Phpapp01Michael WardNo ratings yet

- Condom Social Marketing in India July232012Document16 pagesCondom Social Marketing in India July232012Michael WardNo ratings yet

- Factors Influencing Consumer Buying BehaviorDocument7 pagesFactors Influencing Consumer Buying BehaviorMichael WardNo ratings yet

- Hindalco CaseDocument33 pagesHindalco CaseMichael WardNo ratings yet

- Hindalco CaseDocument33 pagesHindalco CaseMichael WardNo ratings yet

- Monetary PolicyDocument135 pagesMonetary PolicyMayank ChawlaNo ratings yet

- Group Dynamics Presentation: Concepts, Types, Stages and PrinciplesDocument24 pagesGroup Dynamics Presentation: Concepts, Types, Stages and PrinciplesMichael WardNo ratings yet

- How To Trade For Consistent ReturnsDocument46 pagesHow To Trade For Consistent Returnsliang yuanNo ratings yet

- Vietnam Banks: The Sector To Own Significant Potential Upside in The Next 12 MonthsDocument56 pagesVietnam Banks: The Sector To Own Significant Potential Upside in The Next 12 MonthsViet HoangNo ratings yet

- Question Paper Financial Accounting (MB131) : January 2005Document32 pagesQuestion Paper Financial Accounting (MB131) : January 2005Ujwalsagar SagarNo ratings yet

- Indian Shipping Industry RoleDocument11 pagesIndian Shipping Industry RoleThejasvi AnchanNo ratings yet

- Balance Sheet of Shakti PumpsDocument2 pagesBalance Sheet of Shakti PumpsAnonymous 3OudFL5xNo ratings yet

- SEBI's Disclosures and Investor Protection Guidelines Explained! Do You FeelDocument2 pagesSEBI's Disclosures and Investor Protection Guidelines Explained! Do You Feelabhisheksh100% (2)

- Moneylife 26 October 2017Document68 pagesMoneylife 26 October 2017ADNo ratings yet

- Castillo Et - Al Vs BalinghasayDocument10 pagesCastillo Et - Al Vs BalinghasaySimeon SuanNo ratings yet

- APCRDA Engages Consultant to Support Capital City DevelopmentDocument1 pageAPCRDA Engages Consultant to Support Capital City DevelopmentSettyDinakarrambabaNo ratings yet

- PetronDocument61 pagesPetronTrinity Mae QuinaNo ratings yet

- Anmol Biscuits Limited: Rating Analyst ContactsDocument6 pagesAnmol Biscuits Limited: Rating Analyst ContactsSachin BidNo ratings yet

- WEF Alternative Investments 2020 FutureDocument59 pagesWEF Alternative Investments 2020 FutureR. Mega MahmudiaNo ratings yet

- Ratio Analysis Guide for Financial Statement EvaluationDocument66 pagesRatio Analysis Guide for Financial Statement Evaluationthella deva prasad100% (2)

- Chapter 21 - Introduction To Derivative MarketsDocument31 pagesChapter 21 - Introduction To Derivative MarketsSaad KhanNo ratings yet

- NOT To Sell in MayDocument23 pagesNOT To Sell in Maynom1237100% (1)

- Royal Dutch Shell PLC Investor's Handbook 2010-2014: Consolidated Balance Sheet (At December 31)Document1 pageRoyal Dutch Shell PLC Investor's Handbook 2010-2014: Consolidated Balance Sheet (At December 31)Shara ValleserNo ratings yet

- BBM 206 BCM 2209 Principles of Finance End Sem Exam Final Jan-Feb 2017Document3 pagesBBM 206 BCM 2209 Principles of Finance End Sem Exam Final Jan-Feb 2017Hillary Odunga100% (1)

- Impact of M&A on Tata Steel and Cours GroupDocument8 pagesImpact of M&A on Tata Steel and Cours Groupaashish0128No ratings yet

- (1st Exam) Taxation 1 - DigestsDocument36 pages(1st Exam) Taxation 1 - DigestsAnonymous kDxt5UNo ratings yet

- Day Trading - Systems & Methods C Le Beau & D W Lucas PDFDocument80 pagesDay Trading - Systems & Methods C Le Beau & D W Lucas PDFElizabeth Hammon100% (1)

- DAR Securities Wire Transfer Instructions February 2023Document2 pagesDAR Securities Wire Transfer Instructions February 2023michaelblaschke973No ratings yet

- Assignment On Payment Methods: Submitted byDocument6 pagesAssignment On Payment Methods: Submitted bySanam ChouhanNo ratings yet

- Intermediate Accounting, Volume 1: Donald E. Kieso PH.D., C.P.ADocument9 pagesIntermediate Accounting, Volume 1: Donald E. Kieso PH.D., C.P.AFitriani AllethaNo ratings yet

- Zuari Industries LimitedDocument32 pagesZuari Industries LimitedSachin AcharyaNo ratings yet

- Notes From Invest Malaysia 2014: KPJ HealthcareDocument7 pagesNotes From Invest Malaysia 2014: KPJ Healthcareaiman_077No ratings yet

- Negotiable Instruments ExplainedDocument50 pagesNegotiable Instruments ExplainedRolly AcunaNo ratings yet

- Study of Tstockmantra Investment - Offered Services, Risk & GainsDocument47 pagesStudy of Tstockmantra Investment - Offered Services, Risk & GainsBHUPENDRANo ratings yet

- RUNNING HEAD: Forex Risk Management ProductsDocument6 pagesRUNNING HEAD: Forex Risk Management ProductsFatima ShahidNo ratings yet

- 4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostDocument11 pages4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostElvie PepitoNo ratings yet

- PQ PQ PQ PQ B/229 B/229 B/229 B/229 Parliamentary Parliamentary Parliamentary Parliamentary Questions Questions Questions QuestionsDocument6 pagesPQ PQ PQ PQ B/229 B/229 B/229 B/229 Parliamentary Parliamentary Parliamentary Parliamentary Questions Questions Questions QuestionsL'express Maurice100% (1)